Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Retirement planning for non-resident Indians includes various savings and investment plans designed to help build wealth that... Read more ensures lifelong financial independence. The structured and straightforward methods ensure you're financially ready when you are in your retirement phase. Additionally, appropriate NRI retirement solutions provide advantages, including tax relief, convenient fund transfer options, and assured income streams. Read less

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Your details could not be saved.

Please try again.

If you are currently employed abroad but planning to return India after retirement, an NRI retirement plan is your most powerful tool to build a secure corpus back home. A retirement plan in India not only helps you understand various pension plans for NRIs that include savings and investment benefits but also allows you to explore suitable retirement investment options in India and access your funds globally.

Retirement planning work in two key stages, and each serves a different financial purpose over time:

As an NRI, ensuring a financially secure and comfortable retirement can be a complex challenge, especially when living far from home. Although most countries have retirement schemes, their benefits might not be suited to meet the specific requirements of NRIs who must plan for a future involving multiple locations.

You need a financial plan that's flexible and considers inflation estimates, risk tolerance, current cost of living, ongoing healthcare needs, emergencies, and family dependencies.

Let’s understand why NRIs need dedicated retirement solutions.

Tata AIA

Non-Participating, Unit Linked, Individual Life Insurance Pension Plan (UIN:110L182V09)

Tata AIA

A Non-Linked Non-Participating Individual Life Insurance Plan (UIN:110N161V13) | 4T&C apply

There are various NRI pension plans available in India. You can choose one based on your financial goal, risk tolerance and age.

Investing in India offers significant advantages over foreign countries, primarily due to higher interest rates and the country’s fast-growing economy. Here are some of the reasons why NRIs should invest in India.

The following table highlights the features of retirement plan in India for NRIs:

Plan category |

Risk level |

Return structure |

Tax advantages |

Suited for |

ULIPs |

Moderate to High |

Market-dependent, potentially substantial |

Tax4 deduction under applicable sections up to ₹1.5 lakh and maturity proceeds may be exempt under prescribed conditions with death benefits being completely tax-free |

NRIs pursuing growth + flexibility |

Annuity Plans |

Low |

Fixed and guaranteed3 income, offering steady payouts throughout retirement |

Under Section 123, Schedule XV (Erstwhile Section 80C): Contributions to certain annuity plans (like pension plans) are eligible for a tax deduction of up to ₹1.5 lakh in a financial year. Section 11, Schedule II (Erstwhile Section 10(10D): The maturity proceeds of certain annuity plans, including the death benefits, are tax-free |

NRIs seeking a steady, low-risk income stream in retirement |

NPS |

Moderate |

Market-dependent with debt and equity combination |

Tax4 deduction under applicable sections with overall ceiling of ₹1.5 lakh + additional ₹50,000 under specific provisions |

NRIs seeking disciplined, long-term wealth building |

Key features of Retirement plans for NRIs include

NRIs have flexibility in choosing between regular or single premium payments. They also have complete freedom in selecting policy durations. This facilitates their requirements to align with their overseas earnings pattern.

Annuity plans provide a steady income post-retirement, offering financial stability. They provide fixed income which can be critical for managing daily expenses, healthcare costs, and other financial needs. Some annuity plans include survivor benefits, where the annuity continues to be paid to the policyholder’s spouse or beneficiary after their death which provides extra layer of security to policyholder’s family.

Returns would vary depending upon the selected retirement plan. For example, if you choose ULIPs, the life insurance solutions with market-linked5 investment characteristics, the returns will depend on the performance of your investment in the market. Similarly, an annuity scheme guarantees income, as it is a non-linked financial product.

How you take your retirement distributions depends on your type of pension and your goals for the future. The appropriate retirement plans provide options to choose from several payout alternatives. For instance, if you opt for a monthly payout from a deferred annuity, you receive a steady and fixed monthly income for a specified period. Alternatively, if you select a lump sum payout, you obtain a substantial portion of your pension fund at once and utilise it based on your preferences.

International accessibility is one of the key features of NRI retirement programmes. You may be living in any country, but you can access your retirement fund and modify your investment portfolio with ease. Be it contribution or redemption, the process remains easy. Here, the element of transparency comes into play, and you need to choose your retirement plan provider carefully.

Easy portability refers to the ability to maintain and handle an NRI retirement account. Retirement plans, such as NPS, allow for continued transferability across borders, provided the transfer is initiated through an NRO or an NRE account. This is one factor that many other financial products lack.

Following are the important factors to consider when investing in an NRI retirement plan in India:

The investment value for an NRI retirement plan depends not just on the respective instrument's performance but also on currency value changes. If the resident country's currency value weakens against Indian currency, the returns decrease during repatriation.

Being well-informed about both Indian, your residence country's tax systems and Double Taxation Avoidance Agreements (DTAA) under applicable sections of the Income Tax Act helps you avoid double taxation. Generally, NRIs fall under the Indian taxation law, where liability is determined under applicable sections for residential status determination and scope of income, which applies Tax Deducted at Source (TDS) under relevant sections on investment income. Understanding NRI taxation is essential for effective financial planning.

Repatriation can be quite complicated in some investment plans. It is therefore necessary to determine whether your chosen retirement plan offers easy repatriation. For instance, according to the Foreign Exchange Management Act (FEMA) regulation, NRIs can repatriate up to USD 1 million on the principal amount to their NRO account. The interest amount gets repatriated separately.

You can maintain a disciplined savings habit and help ensure uninterrupted fund growth by choosing the right lock-in period. Make sure the lock-in period of an NRI retirement plan matches your regular income before making an investment.

Evaluating your risk tolerance helps in selecting the right retirement plan. As an NRI, you may prefer a balance between secure income and high growth potential. To identify a suitable plan, you need to conduct thorough research and compare various plans before investing.

It's essential that NRIs comply with FEMA, IRDAI, SEBI, and RBI regulations. Proper documentation, with updated KYC, bank statements, address and identity verification, is mandatory. These ensure smooth withdrawals and investments.

NRI retirement programs offer many benefits, some of which are as follows:

The eligibility requirements for investing in an NRI retirement plan are:

Before purchasing the retirement plan, it is important to understand the NRI investment process. You must be aware of all the steps involved in the application process. Here’s how to apply for NRI retirement plans.

The tax4 benefits for NRIs that they can enjoy with retirement plans in India as per the following provision of the Income Tax Act are as follows.

Follow the steps mentioned below to buy NRI retirement plans in India.

Once you complete the due payment, you will receive the purchase details and the policy document. Monitor your retirement plan regularly and reach out to the insurers whenever you want to modify the policy to suit your evolving needs.

Tata AIA NRI retirement plans are designed to help individuals build a retirement corpus systematically while maintaining financial ties with India. Along with retirement savings, these plans also support long-term protection needs, which many times becomes equally important when planning for family security and future income stability.

Here are some of the key reasons NRIs consider retirement plans from Tata AIA.

Retirement plans available in India offer enough potential to generate substantial wealth for securing one’s future. NRIs can invest in them to ensure their family’s financial security.

Individuals between 18 and 60 years, residing outside India for at least 182 days in the previous year or 365 or more in the last four years preceding the previous year, can buy an NRI retirement plan. A valid PAN or declaration of non-tax residency is also required.

You need to submit PAN card or a declaration in company format as proof of a non-tax resident of India and address proof, along with a passport-size photograph, to purchase NRI retirement plans in India.

To select the best NRI retirement plan, consider your financial needs, retirement goals, and current financial situation. Decide based on whether you require a lump sum upon your death or income support for some time or throughout your life.

Section 123 of the Income Tax Act 2025 provides tax4 deductions of up to Rs. 150000 and tax exemption under Schedule II, Clause 2 (Erstwhile 10(10D) on payouts received upon policy maturity.

Yes, NRIs meeting the due eligibility criteria can invest in Indian retirement or pension plans in accordance with the guidelines prescribed in the Foreign Exchange Management Act, 1999.

Yes. OCI may get pension in India by enrolling in the National Pension System governed regulated by the Pension Fund Regulatory and Development Authority (PFRDA). However, individuals must meet the eligibility criteria of the PFRDA Act.

Disclaimer

Unit Linked Life Insurance products are different from the traditional insurance products and are subject to the risk factors. Please know the associated risks and the applicable charges, from your Insurance Agent or Intermediary or Policy Document issued by the Insurance Company.

The fund is managed by Tata AIA Life Insurance Company Ltd. For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. The precise terms and condition of this plan are specified in the Policy Contract.

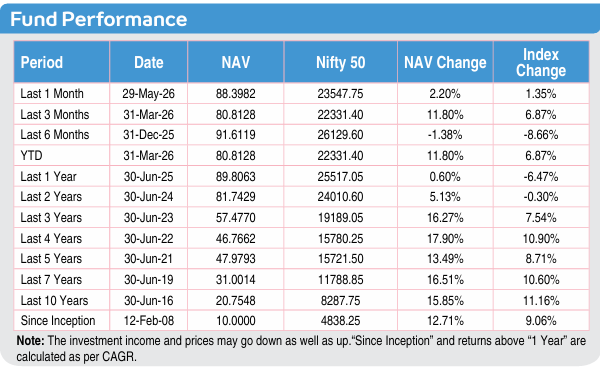

Past performance is not indicative of future performance. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any).

Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. Premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions

Investments are subject to market risks. The Company does not guarantee any assured returns. The investment income and price may go down as well as up depending on several factors influencing the market. Please make your own independent decision after consulting your financial or other professional advisor.

The fund is managed by Tata AIA Life Insurance Company Ltd. (hereinafter the “Company”). Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & Tata AIA Smart Pension Secure is only the name of the Unit Linked Life Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns

The performance of the managed portfolios and funds is not guaranteed, and the value may increase or decrease in accordance with the future experience of the managed portfolios and funds.

The investment income and price may go down as well as up depending on several factors influencing the market. Please know the associated risks and the applicable charges, from your Insurance Agent or the Intermediary or Policy Document issued by the Insurance Company. Please make your own independent decision after consulting your financial or other professional advisor. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any). All investments made by the Company are subject to market risks. The Company does not guarantee any assured return

Life insurance cover is available under the solution. For details on products, associated risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale

Last updated on 10 Aug 2026

Step 1: Obtain your PAN card

Step 1: Obtain your PAN card Step 2: Open an NRO or NRE bank account

Step 2: Open an NRO or NRE bank account Step 3: Complete KYC and other documentation

Step 3: Complete KYC and other documentation Step 4: Select the insurer and plan

Step 4: Select the insurer and plan Step 5: Fill the proposal form and complete the purchase

Step 5: Fill the proposal form and complete the purchase