Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

NRI investment in India continues to rise as Non-Resident Indians (NRI) seek stable, growth-oriented avenues to build long-term... Read more wealth. India’s strong economic performance, competitive returns, and emotional and financial ties make it a preferred destination for global investors. As of May 2025, the country recorded $7.2 billion in gross FDI, with NRIs contributing significantly to this inflow5. Remittances also hit a record $135.46 billion in FY 2025–256, reflecting sustained confidence in India’s financial ecosystem. Read less

Your premium calculation is in progress

Premier SIP Calculator

Here’s your customised plan

Get Maturity Benefit

As per assumed rate of return

₹34.57 Lakh

As per actual past performance

₹70.50 Lakh

Total premium: ₹11.99 Lakh

Additional Benefits

Life Cover (including Terminal Illness Cover)

Accidental Death Cover

Accidental Total & Permanent Disability

Discount

Applicable if the policy is purchased digitally.

This discount is auto-applied and can't be removed

A certified Tata AIA expert will call you from a 1600‑series number to help customise your plan.

Buy Now

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP - Non-participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V01) and

Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually. Product option: Future Secure.

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Your details could not be saved.

Please try again.

NRI investment plans are financial solutions designed specifically for Non-Resident Indians to invest and build wealth while living abroad. They help manage savings across countries, support long-term goals, and offer options for insurance protection, retirement planning, and tax-efficient wealth creation.

Returns as of Apr'26. Fund ratings by Morningstar as of Apr'26.

Choosing the right investment plan may help you build long-term wealth through well-diversified equity, debt, and hybrid funds. Tata AIA offers NRI investment solutions such as Tata AIA Premier SIP and Tata AIA Param Raksha Life Pro +, each following a disciplined strategy to help you align your goals with market-linked7 opportunities. Before selecting a plan, compare factors such as fund performance, asset allocation, and long-term suitability. There are also guaranteed8 returns options like Tata AIA Fortune Guarantee Supreme for steady returns. With goal-based investing, you can create a roadmap for future milestones such as education or retirement. Tata AIA investment plans help you balance growth with financial security while securing your family with a life cover.

NRI investment plans in India are financial products that help Non-Resident Indians grow wealth, maintain financial ties with India, and plan future goals more systematically. In practice, most NRIs are not just looking for returns alone. Many times, the focus also includes stability, family protection, retirement income, and easier financial management across countries.

Here’s a closer look at some of the commonly preferred NRI investment options in India:

NRIs and OCI (Overseas Citizenship of India) holders can invest in the shares of the listed companies in India directly in the stock market. It is generally recommended for investors who want to experience greater long-term growth and who can deal with more active management of market movements.

Mutual funds help NRIs invest across diversified portfolios managed by professional fund managers. Many times, they work well for investors who want market exposure without tracking individual stocks regularly.

ULIP plans combine life insurance coverage with market-linked7 investment opportunities under a single product structure. In practice, they are often considered for long-term wealth creation along with financial protection for dependants.

Real estate continues to attract NRI investors looking for property ownership, rental income, or long-term asset appreciation. Worth noting, many property investments are also linked to future relocation or retirement plans in India.

Retirement plans are designed to help NRIs build a structured retirement corpus over time. Basically, they support long-term financial independence by creating a steady income base for post-retirement years.

The National Pension Scheme is a government-sponsored investment vehicle to motivate disciplined long-term saving. It blends growth and retirement planning objectives.

Pre-IPO investments give NRIs access to companies before they become publicly listed on stock exchanges. While the return potential can be attractive, the investment risk is usually much higher compared to listed equities.

Guaranteed return savings insurance plans offer fixed maturity benefits along with life insurance protection. They are commonly preferred by NRIs who prioritise stability and predictable financial outcomes.

Fixed deposits provide stable returns over a fixed tenure with relatively lower investment risk. In simple terms, they are often used for capital preservation and short-to-medium-term financial planning.

Child plans help NRIs create a dedicated financial corpus for future milestones such as higher education or marriage expenses. At the same time, they also include insurance protection benefits.

Corporate FDs and NCDs are fixed-income investment instruments of companies. They can have a higher return than a regular bank account, but with a greater risk of credit.

PPF is a long term savings scheme with a steady rate of return and tax efficient. If you already have an NRI account, you can continue investing till the maturity date.

Money market instruments are short-term debt instruments like treasury bills and commercial papers. Such investments are primarily for liquidity management and capital allocation for lower risk.

Perpetual bond is a bond that has a fixed interest rate but has no fixed maturity date. These tend to be looked at by investors who want to receive consistent interest over a long period of time.

PSU bonds are issued by government-owned enterprises that are debt instruments. In practice they are seen as more or less stable debt income generating investments.

Bharat Bond ETF invests in debt securities issued by public sector companies through an exchange-traded structure. It provides diversified debt exposure with comparatively lower credit-related risk.

Portfolio Management Services provide personalised investment management with the assistance of experienced portfolio managers. Many of the high net worth NRIs would opt for PMS solutions many times when they are seeking personalised investment strategies.

Startup investments allow NRIs to participate in early-stage business opportunities with long-term growth potential. However, these investments usually involve higher uncertainty and longer investment horizons.

Alternative Investment Funds invest across specialised assets such as venture capital, private equity, and infrastructure projects. They are generally more suitable for experienced investors with higher risk tolerance.

Fractional ownership of commercial real estate allows NRIs to invest in commercial properties without purchasing an entire asset independently. Basically, it lowers entry costs while still offering rental income opportunities.

Infrastructure Investment Trusts (INVITs) are an opportunity for NRIs to invest in operational infrastructure projects like highways, power transmission and energy projects and generate regular income.

Looking to invest in USD? Check out our dollar investment plan. Click here

While there are several investment opportunities, it is important to know why it is considered one of the best options for NRIs and OCIs to invest in India.

The process for investing in the NRI and OCI investment plans varies based on the specific financial instrument. Here are the few essential steps that can help NRIs and OCIs to invest in India:

NRIs and OCIs should open an NRO or NRE bank account with an Indian bank to invest in India. It is important to remember that an NRE account should be used for investments using foreign earnings that can be repatriated. The NRO account should be used for investments based on earnings in India that cannot be repatriated.

NRIs and OCIs should have a PAN card to invest in India. It is important for various processes such as opening a bank account, investing, filing Income Tax Returns, and claiming tax2 deductions and exemptions, etc.

NRIs and OCIs have different investment options, such as direct equity, mutual funds, savings schemes, etc. They need to compare and evaluate the benefits to choose some of the best options.

Prepare the documents for the investment plans and complete the KYC (Know Your Customer) norms specific to the investment options in India for NRI or OCI. Submit the required identity and address proofs to complete the process.

NRI and OCI investors need to understand the tax2 implications, rules, and regulations concerning India and the country of residence to avoid unnecessary discrepancies in the future. It is always recommended to take the advice of tax consultants or financial advisors regarding OCI and Income tax provisions2 relating to NRI to make the best investment decisions.

Factor

Details

Key Features of Term Insurance Plan

Age

Must be between 18–65 years (varies by insurer)

Documents

Required documents include valid passport with latest immigration stamps, visa copy or work/study permit, and proof of residence (Indian and foreign). Identity proof, age proof, income proof, FATCA annexure, and a completed NRI questionnaire are also needed.

Medical Requirements

Medical tests are mandatory for higher coverage amounts, usually conducted remotely or at approved centers. Disclosure of medical history is required. Video medicals may be accepted by some insurers. Additional tests may be requested based on the underwriting policy.

In India, NRI investment options generally require the following documents:

Self-attested copy of passport.

As per Indian government regulations, you must have documents proving your non-resident Indian status (NRI) like visa, work permit or residence permit.

You must have a Permanent Account Number (PAN). An NRI declaration in place of a PAN may be used if you do not have a PAN. To ease taxation and ensure compliance, this is necessary.

To invest in India, you need a Non-Resident Ordinary (NRO) or a Non-Resident External (NRE) bank account.

Overseas or Indian residence proof through utility bills, bank statement or approved proofs.

Recent passport size photographs.

Fresh KYC is required, specifically listing foreign address.

Necessary for buying stocks directly via Portfolio Investment Scheme (PIS).

A Foreign Account Tax Compliance Act (FATCA) declaration is mandatory for determining tax residency.

In addition to these standard documents, you may also need to submit a few others, depending on how you plan to invest in India as an NRI. Consult with your financial advisor or a consulting institution to determine the specific requirements for each plan.

Here are the tax2 benefits applicable for investment for NRIs:

As an NRI, you should comply with the following FEMA guidelines before investing in India:

NRIs often make these investment planning mistakes. Avoid them to benefit from the best investment options for NRIs in India:

16T&C apply

1.

The Reserve Bank of India (RBI) and the Securities and Exchange Board of India (SEBI) govern OCI and NRI investments in India. The investments are regulated based on the Foreign Exchange Management Act of 1999.

2.

A person investing in India is considered a Non-Resident Indian (NRI) and liable to pay tax2 if they have Indian citizenship and, however, reside in a foreign destination. The purpose of the shift can be for reasons such as employment, business, or any other specific intention.

They are called an NRI if they do not meet the following criteria:

●Resided in India for more than 182 days in a financial year ●Resided in India for 60 days or more in the previous year and 365 days or more during the 4 years preceding the previous year

Furthermore, the eligibility criteria can differ for the individual investment plan option. Some of the primary conditions required are:

●Age between 18 and 60 years ●Having a PAN Card ●Having an NRE or NRO Account for the transfer of funds

3.

India is one of the fastest-growing economies, having better key economic indicators. It offers wide-ranging investment opportunities and contributes to higher returns.

In addition, clear regulations and streamlined processes provide easy access to investments. Furthermore, NRI and OCI investors can benefit from tax2 deductions and exemptions for the income earned in India based on the type of investment.

4.

The best investment plan for an NRI or OCI in India will depend on the individual financial requirements, risk appetite, investment period, and affordability. Aggressive investors can invest in direct equity, equity-oriented mutual funds, ULIPs, etc., while conservative investors can choose fixed deposits, Public Provident Fund investments, Bonds, etc.

5.

An NRE account holds foreign earnings in India, is tax-free2, and allows full repatriation. Whereas, an NRO account holds Indian income, is taxable, and has limited repatriation limits upto $1 Million per financial year.

6.

Yes, NRIs and OCIs can start investing in mutual funds through Systematic Investment Plans in India.

7.

The documents required for the NRIs and OCIs to invest in India will differ for the different types of investments. Some of the common documents required are:

●PAN Card ●Copy of Passport ●Recent passport-size photograph ●Proof of residence outside India ●Bank statement of the NRE or the NRO Account ●Power of attorney

8.

NRIs and OCIs cannot open a Public Provident Fund (PPF) in India. However, if they had opened it earlier when they were resident Indians, they can continue to contribute to their PPF Account.

9.

Yes, NRI and OCI investors can avail of tax2 deductions and exemption benefits for their investments and the income earned in India.

10.

Yes, NRIs and OCIs can invest in the Indian stock market. However, NRI and OCI investors need to open a Portfolio Investment Scheme (PIS) Account with a bank to invest in the stock market.

In addition, they should also ensure to have the following:

●NRE Account ●NRO Account ●Demat Account ●Trading Account with a registered stockbroker.

11.

PIS refers to the Portfolio Investment Scheme (PIS). It is not mandatory for all types of investments. NRI and OCI investors need to open a PIS Account with a bank to invest in the Indian stock market.

12.

Yes, NRIs and OCIs can have multiple Demat accounts. It is important to note that NRIs and OCIs should have separate Demat accounts for the non-repatriable (NRO) and repatriable (NRE) investments.

13.

●Wide-ranging investment opportunities ●Various options cater to different categories of investors, such as based on the risk profile. ●Clear regulations and streamlined processes for easy access to investments ●Higher returns on the investments ●Easy and convenient repatriation of funds ●Tax2 deductions and exemptions for specific investment plans.

14.

The different types of NRI and OCI investment plans available in India are:

●High Return Options for NRI and OCI Investment in India ●Direct Equity ●Mutual Funds ●Unit Linked Insurance Plans (ULIP Plans) ●Real Estate ●National Pension Scheme ●Pre-IPO Market ●Low-Risk Options for NRI and OCI Investment in India ●Savings Insurance Plans ●Fixed Deposit ●Corporate Fixed Deposits (FDs) or Non-Convertible Debentures (NCDs) ●Public Provident Fund (PPF) ●Money market instruments ●Perpetual Bonds ●PSU Bonds ●Sovereign Gold Bonds ●Bharat Bond ETF ●NRI and OCI Investment Options for HNI in India ●Portfolio Management Services (PMS) ●Startups ●Alternative Investment Funds ●Fractional Ownership of CRE ●INVITs (Infrastructure Investment Trust).

15.

Yes, NRI and OCI investment plans are subject to taxation in India based on the type of investment, such as equity, mutual funds, real estate, NPS, etc.

16.

NRIs and OCIs can purchase residential and commercial real estate properties in India. However, OCI’s cannot choose to purchase farms, plantations, and agricultural land.

18.

NRIs and OCIs can manage their investment plans in India by:

●Keeping track of the market trends and being informed of the key performance indicators ●Staying updated through online news platforms and taking the necessary actions ●Regularly reviewing the investment platform based on the changing risk appetite and investment needs ●Choosing the Portfolio Management Services ●Keeping track of any changes in the regulatory and taxation policies ●Seeking help from professional financial advisors

19.

NRIs and OCIs cannot directly invest in Post Office Schemes in India. They should have a joint account with a relative who is a resident Indian to invest in them.

20.

Yes, a PAN card is mandatory for NRIs and OCIs investing and having taxable income in India.

21.

The investor can continue to invest in the SIP after becoming an NRI or OCI, but the following changes are required:

●Changing the residential status ●Converting the bank account to NRE or NRO ●Complying with additional Foreign Account Tax Compliance Act (FACTA) requirements for people moving to US or Canada.

22.

NRIs or OCIs can repatriate their investments from India using their NRE (Non-Resident External) Account.

23.

NRIs can invest in certain Indian government bonds alongside some PSUs and RBI bonds. Reserve Bank of India (RBI) offers the Fully Accessible Route (FAR) to invest in Government Securities (G-secs) and State Development Loans (SDLs).

24.

NRI investments in Indian companies are limited to 10% of the company's paid-up capital, with a single investor having a 5% limit. If the company passes a special resolution in its general body meeting, this limit can be increased to 24%.

25.

Yes. The Foreign Exchange Management Act (FEMA), 1999 allows NRIs to invest in startups in India. Startups must adhere to government regulations to ensure foreign funds are legally channeled.

26.

Investing in mutual funds or opening a bank account in India requires Non-Resident Indians (NRIs) to update their KYC (Know Your Customer) information. To ensure compliance with Indian financial regulations, this is a mandatory requirement.

27.

Non-Resident Indians (NRIs) can invest jointly with Indian residents in certain circumstances. NRIs are permitted to open joint accounts with residents (as defined in the Companies Act) on a "former or survivor" basis.

28.

Yes. The exchange rate affects NRI investments in India. When repatriated to the investor's home currency, these rates have a significant impact on investment value and returns.

29.

NRIs cannot directly invest in India using international credit cards. Regulations require NRIs to transfer funds for investments in India from verified bank accounts, either NRE or NRO.

The information, provided herein, may not be treated as a solicitation request in any manner. Any decision to buy online insurance by NRIs is completely his/her choice. The insurer is permitted to solicit insurance in India and settles claim in INR only.

Param Raksha Life Pro+ is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). These products are also available for sale individually without the combination offered/ suggested.

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP, a non-participating, unit-linked, individual life insurance savings plan (UIN: 110L174V02), and Tata AIA Health Buddy, Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually.

Tata AIA Fortune Guarantee Supreme - Individual, Non-Linked, Non-participating, Life Insurance Savings Plan (UIN110N163V13)

Tata AIA Shubh Flexi Income Plan (UIN: 110N207V02) - Individual, Non-Linked, participating, Life Insurance Savings Plan

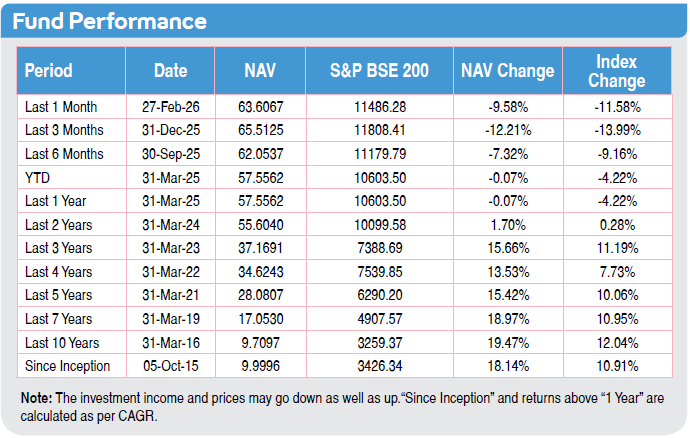

1Illustration shows a monthly premium of ₹30,000 for Tata AIA Premier SIP for a 20-year-old male, standard life, premium payment term: 10 years, policy term: 20 years with 100% investment in Tata AIA Multi Cap Fund in Future Secure plan option. 4% and 8% are assumed rates of return. 19.47% is the 10-year returns of Tata AIA Multi Cap Fund as of March 2026. Maturity amount: ₹49,81,642 at 4% returns, ₹89,85,023 at 8% returns and ₹4,55,37,159 at 19.47% returns. The fund value calculation is done by projecting the past returns of Tata AIA Multi Cap Fund after adjusting for all expenses in Tata AIA Premier SIP. The above values have been calculated assuming 19.47% CAGR, which is the past 10-year returns of Tata AIA Multi Cap Fund as of March 2026.

2No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfillment of conditions of aggregate premium within threshold limit of ₹2.50 Lakh/annum for ULIP and ₹5.0 Lakh/annum for non ULIP Life insurance and maintaining conditions of premium to sum assured ratio as stipulated therein in section 11 read with schedule II of Income Tax Act 2025. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

310-year computed NAV for Multi Cap Fund as of March 2026. Other funds are also available. Benchmark of this fund is S&P BSE 200.

4All funds open for new business which have completed 5 years since inception are rated 4 star or 5 star by Morningstar as of August 2025.

©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

6Source: https://telanganatoday.com/nri-remittances-to-india-soar-to-record-135-46-billion-in-fy25

7Market-linked returns are subject to market risks and terms & conditions of the product. The assumed rate of returns or illustrated amount may not be guaranteed and depends on market fluctuations.

8Guaranteed Income shall be total of Guaranteed annual Income plus Income Booster payable in a year. Guaranteed Income as per the chosen Income Frequency shall commence after maturity till the end of the Income Period, irrespective of survival of the life insured(s) during the Income Period.

9This will be basis chosen policy option, certain income term and age criteria, 6% IRR availability.

10Cash bonuses (if declared) may be opted to be paid out at the end of the chosen pay-out frequency or as premiums offset. Cash bonuses are applicable for Early income and Deferred income option. Please refer Brochure for additional details

11Only available with cash bonus option. The current loyalty addition rate on the Sub-wallet will be 5.25% compounding monthly. The loyalty addition rate shall be at which RBI absorbs liquidity which currently is the Standing Deposit Facility (SDF) rate. The current Standing Deposit Facility rate is 5.25% p.a. and the same shall be reviewed bi-monthly. The Company may in future change the reference rate from Standing Deposit Facility rate to some other index.

1289,43,554 families protected till 31st May 2025.

13Retail Sum Assured for FY 2025-26 is ₹9,00,876 Crore.

14Total Assets Under Management (AUM) as on 31st Mar’26 is 1,45,589 Crores.

15Individual Death Claim Settlement Ratio is 99.45% for FY 2025-26 as per the latest annual audited figures.

16Applicable to only non-early claims more than 3 years of policy duration, non-investigation cases, up to Sum assured of ₹50 Lakh. Applicable for branch walk in. Time limit to submit claim to Tata AIA by 2 pm (working days). Subject to submission of complete documents. Not applicable to ULIP policies and open title claims.

For Tata AIA Shubh Flexi Income Plan

The risk factors of the bonuses projected under the product are not guaranteed.

Past performance doesn't construe any indication of future bonuses.

These products are subject to the overall performance of the insurer in terms of investments, management of expenses, mortality and lapses.

For ULIP products

In this policy, the investment risk in investment portfolio is borne by the policyholder.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Linked Life Insurance products are different from traditional insurance products and are subject to risk factors.

The premium paid in Linked Life Insurance policies is subject to investment risks associated with capital markets and publicly available index. The NAV of the units may go up or down based on the performance of Fund and factors influencing the capital market/publicly available index and the insured is responsible for his/her decisions.

Tata AIA Life Insurance Company Limited is only the name of the Life Insurance Company & Tata AIA Smart SIP and Tata AIA Smart Sampoorna Raksha Supreme are only the name of the Linked Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the insurance company.

The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns.

Past performance is not indicative of future performance.

If your policy offers variable benefits, then the illustrations on this page will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

L&C/Advt/2026/May/3348

Popular Searches

Last updated on 20 Jul 2026

Reviewed by

Reviewed by