Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Life insurance for NRI provides financial security to Non-Resident Indians and their families in India. It helps cover essential... Read more expenses like education, loans, and emergencies. Life insurance for NRI helps ensure continued support for dependents during uncertain times and future needs. Read less

Get Life Cover of ₹1 Crore by paying a premium of

₹7,085/month

Total premium: ₹14.09 Lakh

Save ₹1,202 with discounts

Save ₹1,202 with discounts

Discounts

10% discount on 1st year premium is applicable on online purchase. This discount is auto-applied and can’t be removed

8.5% discount on 1st year premium is applicable for salaried personnel. You will need to share your corporate email ID if you opt for this discount. This discount is auto-applied if you select ‘Salaried’ as your occupation and can’t be removed

Applicable only if the policy is bought digitally. Some discounts will not be available when this option is selected.

1% discount on 1st year premium for all payments paid through any permissible electronic mode debited through an auto-debit mandate. Maximum discount capping: ₹100 over the year.

2% discount on 1st year premium on these milestones

| Event | Eligibility |

|---|---|

| Wedding (1 wedding only) | Within 6 months before or after the date of wedding |

| Birth/ Adoption of 1st child* | Within 6 months before or after the birth/ adoption date |

| Home loan | Within 6 months of loan getting sanctioned |

| First job | Within 6 months of joining date |

*Policy issuance eligibility for female customers will be determined by Board Approved Underwriting Policy (BAUP)

The above milestones cannot be clubbed to avail more discount, Such discount shall be capped to a maximum of ₹500 over the year.

A certified Tata AIA expert will call you from a 1600‑series number to customize your plan.

Buy your plan

Please select an option

Minimum income: ₹5 Lakh

Tata AIA Sampoorna Raksha Promise - Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V11)

₹1 Crore

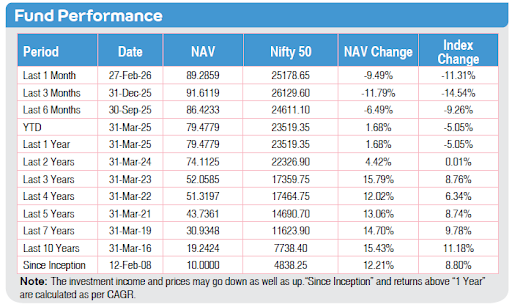

4% and 8% are assumed rates of return. Tata AIA Multi Cap Fund 5-year Returns: 15.42% (Benchmark: 10.06%) as of Mar'26

by paying a premium of ₹21,749/month (for 5 years)

Total premium: ₹14.09 Lakh

Save ₹1,202 with discounts

Select an option

Select an option

10% discount on health product premium every year Additional fund booster will be added at the end of the policy term which is a defined % of average fund value on the last business day of the last eight policy quarters (2 years)

| Policy Term (years) | Fund Booster % |

|---|---|

| 30-34 | 7% |

| 35-39 | 8% |

| 40 and above | 10% |

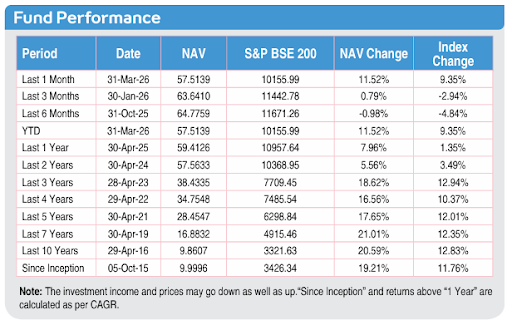

| Fund Name | 5 Year Returns |

Benchmark Returns |

Benchmark Name |

|---|---|---|---|

| Multi Cap Fund | 15.42% | 10.06% | S&P BSE 200 |

| Top 200 Fund | 16.09% | 10.06% | S&P BSE 200 |

| India Consumption Fund | 16.21% | 10.06% | S&P BSE 200 |

Returns as of March, 2026

A certified Tata AIA expert will call you from a 1600‑series number to help customise your plan.

Param Raksha Life Pro +. This advertisement is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). These products are also available for sale individually without the combination offered/suggested. This benefit illustration is the arithmetic combination and chronological listing of combined benefits of individual products. The customer is advised to refer the detailed sales brochure of respective individual products mentioned herein before concluding sale.

ULIP Calculator

Make Your Dream a Reality with Guaranteed9 Returns

Life insurance policy for NRI is a financial product that provides financial protection to Indians living abroad. This type of plan provides a death benefit to family members in case of the policyholder’s death. The premium can be paid in Indian rupees or foreign currency, depending on the payment source. The best life insurance policy for NRI in India accepts premium through NRE (Non-Resident External), NRO (Non-Resident Ordinary), or FCNR (Foreign Currency Non-Resident) accounts.

Medical tests, income documents, and video-based verifications are usually required. It also helps in tax savings6 under Indian law and allows secure claim settlement through nominee accounts. Payment modes are flexible, and the documentation can be completed digitally.

There are various types of Life Insurance plans that are being offered. Select appropriate category to view plans.

Protect the financial future of your loved ones against uncertainties of life with our Term Insurance plans that offer you larger cover, higher security, and a speedy settlement.

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V12)

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product

(UIN: 110N171V15)

Grow your wealth with our guaranteed return plans for a fikar-free future and also save on tax. No GST on premium payments through SWIFT/NRE/Forex accounts.

Non-Linked, Non-Participating, Individual Life Insurance Savings Plan

(UIN: 110N158V14) | 21T&C apply

Individual, non-linked, participating, Life Insurance Savings Plan

(UIN: 110N207V02)

Individual, Non-Linked, Non-participating, Life Insurance Savings Plan (UIN110N163V13)

Discover Complete Health and Wealth: Our comprehensive plan takes care of your health, wellness, and financial security all in one.

A non-linked, Non-Participating Individual Health rider

(UIN:110B046V02)

A non-linked, Non-Participating Individual Health rider

(UIN:110B046V02)

Plan your retirement wisely with a suitable pension plan for peace of mind in your golden years.

Non-Participating, Unit Linked, Individual Life Insurance Pension Plan

(UIN: 110L182V09)

A Non-Linked, Non-Participating, Annuity Plan

(UIN:110N161V13) | 13T&C apply

There are several NRI life insurance plans available in India, and each one serves a slightly different purpose. Some focus purely on protection, while others combine savings or retirement planning. In practice, the right choice depends on what you need today and what you expect in the long term.

| Plan Type | Best For | Key Features / NRI Benefits |

|---|---|---|

| Term Insurance | NRIs seeking high coverage at affordable premium rates for long-term financial protection needs | Provides pure life cover for a fixed period with flexible terms and optional riders16. Many times, this is the first choice for those who want straightforward financial protection for dependants without adding investment components. |

| Whole Life Insurance | NRIs looking for lifelong coverage and structured wealth transfer for their family members | Offers coverage for the entire lifetime of the policyholder with guaranteed payout to nominees, supporting long-term financial security and legacy planning objectives |

| ULIPs | NRIs interested in combining insurance protection with market-linked15 investment opportunities for wealth creation | Allocates premium between life cover and investment funds, allowing switching between equity and debt options with flexibility to align with changing financial goals |

| Endowment Plans | NRIs who prefer a combination of protection and disciplined savings for future financial commitments | Provides life cover along with guaranteed maturity benefits, helping build a corpus over time while ensuring financial protection throughout the policy duration |

| Money Back Plans | NRIs who prefer periodic payouts along with continued life insurance protection benefits | Offers survival benefits at regular intervals during the policy term while ensuring remaining sum assured is paid at maturity or in case of unforeseen events |

| Child Insurance Plans | NRIs aiming to secure their child’s education and future financial needs effectively | Ensures financial support for a child’s future goals, offering structured payouts even in the absence of the policyholder. It helps manage education and milestone expenses |

| Retirement Plans | NRIs preparing for a stable income after retirement in India | Helps build a retirement corpus with options for annuity or lump-sum payouts. Over time, it supports a more predictable income stream during |

All eligible NRIs, OCIs/PIOs, and Foreign Nationals can purchase NRI life insurance plan in India. We offer the following features for the long term.

We provide the required life insurance coverage based on the chosen policy term and the affordable premium cost. This covers them worldwide.

The NRIs can avail of life insurance for a term suitable to their needs.

The policyholders can also avail themselves of the flexible features provided in India's NRI life insurance policies. For example, they can choose to pay the premium for a limited term while enjoying the benefits through the entire policy term, opting to include the add-on rider16 benefits, etc.

Premium payments by NRIs/OCIs/PIOs/Foreign Nationals can be made from their NRO/NRE/FCNR accounts in Indian Rupees. Alternatively, they can pay the same amount in foreign currency from their foreign bank account. The banker can be instructed on electronic money remittance through SWIFT into our bank account.

To purchase NRI insurance policies, online medical check-ups and consultation facilities are made available to the policyholders. Therefore, purchasing life insurance plans becomes a simple and convenient option.

Purchasing life insurance plans in India is considered beneficial for the NRIs based on the following:

The table below clearly outlines who can buy life insurance for NRI in India.

| Category of People | Meaning | Eligibility Criteria | Exceptions |

|---|---|---|---|

| Non-Resident Indian (NRI) | Indian citizen residing outside India for more than 182 days annually | Valid Indian passport, foreign address proof, NRE/NRO/FCNR account | Must maintain Indian citizenship status |

| Overseas Citizen of India (OCI) | Former Indian citizen or foreign national of Indian origin | OCI card, foreign residence proof, banking relationship in India | Cannot hold an Indian passport simultaneously |

| Person of Indian Origin (PIO) | Foreign citizen with Indian ancestry up to great-grandparent level | PIO card, ancestry documentation, foreign residence proof | Documentation process may be lengthy |

| Indian Students Abroad | Temporary residents studying overseas | Student visa, university enrollment proof, Indian address for correspondence | Subject to individual insurer policies |

| Indian Workers on Assignment | Employees working abroad temporarily | Employment visa, company sponsorship letter, intention to return proof | Assignment duration should be clearly defined |

All categories need valid documents like a passport, NRE/NRO proof, and address. This helps ensure compliance and eligibility under Insurance Regulatory and Development Authority (IRDAI) rules.

Before buying NRI life insurance, consider the following:

These points may help you choose the best life insurance policy in India for NRI based on your individual needs and family protection goals.

The table below explains the common eligibility rules:

| Factor | Detail |

|---|---|

| Age | Must be between 18–65 years (varies by insurer) |

| Documents | Required documents include valid passport with latest immigration stamps, visa copy or work/study permit, and proof of residence (Indian and foreign). Identity proof, age proof, income proof, FATCA annexure, and a completed NRI questionnaire are also needed. |

| Medical Requirements | Medical tests are mandatory for higher coverage amounts, usually conducted remotely or at approved centres. Disclosure of medical history is required. Video medicals may be accepted by some insurers. Additional tests may be requested based on the underwriting policy. |

4T&C apply

Protect the financial future of your loved ones against uncertainties of life with our Term Insurance plans that offers you larger cover, higher security, and speedy settlement.

The claim process for term insurance is as follows:

NRI insurance offers living benefits to policyholders and death benefits to the respective family members in the event of the policyholder's death, irrespective of their location. Here are a few guidelines that every NRI should know.

In rupee life insurance policies, if the claim needs to be settled in favour of the claimants residing outside India, the payout in foreign currency should be proportionate to the amount of premium that has been paid in foreign currency out of the total premiums payable.

Nominees/beneficiaries residing outside India are permitted to credit insurance claims/maturity/surrender value settled in foreign currency to their NRE/FCNR account if they so desire.

A resident beneficiary can open a Resident Foreign Currency (RFC) Account and credit claims/maturity benefits/surrender value settled in foreign currency to the account.

Resident beneficiaries previously residing outside India can open an RFC Account on becoming a resident and credit the proceeds of claims/maturity proceeds/surrender value settled in foreign currency.

If a rupee life insurance policy is issued to an Indian resident outside India and the premiums have been collected in non-repatriable rupees, the claims/maturity benefits surrender value will be credited to the beneficiary’s NRO account in rupees. The same applies if a death claim is settled in favour of the assignees/nominees of a resident outside India.

For rupee policies issued to foreign nationals who do not live permanently in India, claims, maturity proceeds, or surrender values can be paid in rupees or sent abroad if the claimant requests it.

The following points may help you choose the right life insurance for NRIs

NRI Insurance India offers a combination of cost efficiency, flexibility, and practical benefits for NRIs. Many times, they also help simplify financial planning for family members who stay in India.

| Benefit | Explanation |

|---|---|

| Tax and Currency Benefits | Premiums may qualify for deductions under Section 80C, while maturity proceeds can be exempt under Section 10(10D), subject to applicable conditions. For NRIs, Double Taxation Avoidance Agreements may also provide relief, which is worth considering in cross-border financial planning. |

| Cost-Effective Premiums | Life insurance plans in India are generally priced lower compared to countries such as the United States and the United Kingdom. This makes long-term coverage more affordable due to favourable underwriting and operational efficiencies |

| Access to Diverse Investment Plans | Plans such as ULIPs provide exposure to different asset classes, including equity and debt. This allows NRIs to align their investments with changing goals while still keeping life cover in place. |

| Comprehensive Product Range | There is a wide range of plans available, from pure protection to savings and retirement-focused options. Basically, this gives NRIs the flexibility to choose based on their financial priorities rather than fitting into a single structure. |

| Cross-Border Financial Planning | Insurance benefits can be transferred smoothly to nominees residing in India, ensuring compliance with regulatory frameworks and supporting efficient estate planning across different countries. |

The tax benefits6 for NRI life insurance are as follows:

The claim process for term insurance is as follows:

For further guidance, you can visit the Tata AIA Claim Settlement Ratio page.

Our experts are happy to help you!

(for existing customers)

NRIs can purchase life insurance policies from anywhere. Here are the details:

While In India

Life insurance policy can be purchased in India easily through quick, digital process.

When outside India

NRI can purchase the life insurance policy from their current place of residence subject to our Board approved underwriting policy.

1.

Yes. NRIs, OCIs, and PIOs can purchase life insurance policies from abroad via digital application, video‑KYC, and medical tests worldwide.

2.

You will need valid passport, NRE/NRO/FCNR account details, proof of foreign residence, PAN or TRC, and income documents or salary proof.

3.

Premiums can be paid via Non‑Resident External (NRE), Non‑Resident Ordinary (NRO) accounts, as well as through NEFT or SWIFT international bank transfers.

4.

Yes. Many insurers allow premium payments in foreign currencies if the premium is sourced from NRE, FCNR, or appropriate bank accounts.

5.

Not always. But having an NRE/NRO/FCNR account simplifies premium payments and helps ensure smooth claim and maturity settlements.

6.

Yes, a Permanent Account Number (PAN) or Tax Residency Certificate (TRC) is required for tax reporting and regulatory compliance.

7.

Yes. Many providers support digital submission and electronic transfer of claim proceeds, subject to documentation and verification processes.

8.

You can inform the insurer by phone, email, or through their website. Policy details, claim form, and required certificates should be shared for timely processing.

9.

The insurance claim is settled after reviewing submitted documents (claim form, policy papers, medical and bank details). The insurer verifies all the details and transfers funds to the nominee’s account.

10.

Communication is possible via:

· Phone helpline

· Official email ID

· Customer portal or mobile app

· Branch office visitation (if in India)

11.

You can download the e‑policy from the insurer’s website or request a physical copy delivered to your Indian or foreign address.

12.

Yes. Premium rates may vary based on country of residence due to different mortality rates and risk assessments.

13.

Yes, NRIs can purchase policies under the Married Women's Property Act (MWPA) for the well-being of their spouse and children.

14.

Yes. Within the free‑look period (usually 15–30 days from receipt), an NRI may return the policy for a refund as per policy terms.

15.

Death benefits are generally tax-free6, but maturity proceeds may be taxable2 if premium exceeds specified limits under Section 10(10D).

16.

Yes. Annuity income is taxable as per slab rates in India. The lump sum pension amount received in advance may be partially exempt under Section 10 of the Income Tax Act.

17.

Amounts received by the nominee (including guaranteed additions) are generally tax‑free under Section 10(10D)2, subject to policy conditions.

18.

TDS will not be deducted if the NRI resides in a country where DTAA is applicable provided the following documents are submitted at least once a year (During the pay-out period):

· FATCA/CRS (self-declaration form)

· Form 10F (self-declaration form)

· No Permanent Establishment (PE) declaration (self-declaration form)

· Tax residency certificate (TRC) issued by Govt. of the respective country

A list of major countries where DTAA benefits are available and payment can be made without deduction of TDS subject to submission of mandatory documents is as below.

No DTAA benefit is available for countries other than those mentioned in the table below, and payment will be subject to deduction of TDS irrespective of submission of mandatory documents.

| Country | Country |

|---|---|

| Australia | Sudan |

| New Zealand | Ukraine |

| Singapore | Zambia |

| Sri Lanka | Switzerland |

| UAE (Dubai) | Ethiopia |

| UK | Ireland |

| USA | Norway |

| Indonesia | Czech Republic |

| Thailand | Hungary |

| Saudi Arabia | Iceland |

| France | Uganda |

| Germany | Mauritius |

| Mozambique | Vietnam |

| Nepal | Kazakhstan |

| Oman | Belgium |

| Philippines | Romania |

| Portugal | Poland |

| Netherland |

In countries where DTAA benefit is not available or policyholders do not submit the mandatory document, TDS will be deducted at the following rates:

| Particulars | Tax Rate* |

|---|---|

| Aggregate Taxable payout is up to ₹ 50 Lakh |

31.20% |

| Aggregate Taxable payout exceeds ₹ 50 Lakh, but up to ₹ 1 crore |

34.32% |

| Aggregate Taxable payout is more than ₹ 1 crore | 35.88% |

Including applicable surcharge and cess. This is as prevailing Tax rates.

In case a valid PAN is provided, the policyholder can claim credit for TDS deducted by filing a Non-Resident Indian income tax return.

Above DTAA benefits would be applicable for annuity payout, however in case of ULIP and non ULIP plans, payout would be taxable. Such NRI are required to file tax return in India, in accordance with provisions of income tax law. NRI will be eligible to get a tax credit of tax so paid.

19.

TDS applies only on the surrender value exceeding total premiums paid. No TDS is deducted if the surrender value is equal to or less than the total premium paid.

20.

Yes. FATCA/CRS declarations, Tax Residency Certificate (TRC), local tax identification number (TIN), and foreign address proof may be required.

21.

If an NRI customer relocates to India while the policy is still active, you just need to submit the following documents.

· Indian address proof

· Declaration as per format - Residential Undertaking-Section 195

· Indian Bank account details for NEFT

22.

If a resident Indian relocates abroad and becomes an NRI, the following documents need to be submitted to the insurer:

· FATCA-CRS form 10F form (Form 10F can be downloaded from https://www.incometaxindia.gov.in/Pages/downloads/forms.aspx )

· No PE form

· TRC

· Foreign Address proof

· Bank account details for NEFT

The life insurance policy will carry on in Indian currency after you move abroad. The maturity and death benefits will be payable if the premiums are paid regularly

23.

The policy continues, but the insurer should be notified of the address change for proper servicing and compliance.

24.

The Foreign Account Tax Compliance Act (FATCA) and Common Reporting Standard (CRS) are tax information exchange frameworks to prevent cross‑border tax evasion.

25.

The FATCA & CRS apply to customers with foreign tax residence or financial accounts abroad, including NRIs, based on global reporting regulations.

26.

Yes. If any personal details change (tax residence or account jurisdiction), you may need to submit updated FATCA/CRS declarations.

27.

The Tax Identification Number (TIN) may be required if your country of residence mandates it for tax reporting or financial transactions.

Yes. Non‑Resident Indians (NRIs), OCIs, and PIOs can buy life insurance policies in India subject to IRDAI rules and eligibility criteria.