Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Pension calculators provide an easy way to calculate how much income you can expect after retirement. It's important to use... Read more a pension calculator to plan ahead for an ideal retirement. You can easily map your savings, investments, and returns with it. A well-planned retirement plan starts by considering future needs and how to achieve them. When you take control of your investment decisions now, you'll be able to live comfortably after retirement. Whether you're starting out or about to retire, this tool gives you clarity and confidence. Read less

A retirement and pension calculator is a simple online tool that helps you estimate how much pension income you may receive after retirement. It uses basic details like your salary, age, current savings, years of service, and future contributions to give you an estimate. By entering these details, you can plan your savings better and stay on track to reach your retirement goals.

This tool is easy to use and saves time while giving useful insights into your future financial needs. You can also try different combinations of inputs to compare and choose the right retirement plan. While selecting the best pension plan calculator in India, look for one that offers an assured payout to match your financial needs.

Since retirement planning takes time, it’s preferable to start early to benefit from compounding. Using a pension plan calculator helps you plan your income wisely and gives you a clear idea of what to expect after you retire.

The pension calculator works based on a few formulas. They involve the following components.

Tata AIA Pension Calculator is an online financial tool that allows you to estimate your pension amount once you retire. After visiting the Tata AIA Pension calculator page, follow these steps:

Enter your date of birth (DD/MM/YYYY) to calculate your age and retirement date.

Enter your monthly expenses in ₹ to determine your financial needs after retirement. In this way, you can estimate how much pension you need.

To calculate the future value of your retirement fund, enter the expected return on your savings and investments.

Provide information regarding your monthly investments in different financial instruments, such as fixed deposits, mutual funds, stocks, and other retirement savings plans.

The full name should be entered in the same manner as the full name on your official ID document, such as your Aadhar card or PAN card.

Enter your mobile phone number in the provided field.

After entering your details, click "Check Returns" to get your estimated pension amount and accumulated corpus. By learning how much more investment you need to make to reach your retirement goals, you will be able to plan accordingly.

Tata AIA

Tata AIA Smart Pension Secure (UIN: 110L182V09) - Non-Participating, Unit Linked, Individual Life Insurance Pension Plan

Tata AIA

Tata AIA Life Insurance Fortune Guarantee Pension Plan (UIN:110N161V13) - A Non-Linked Non-Participating Individual Life Insurance Plan

Here’s why retirement planning is important:

Once you retire and stop working, you no longer secure a regular income through a salary. But the daily expenses, along with some other needs doesn't end. Without an efficient financial plan, managing all the requirements may be difficult. With a suitable retirement plan in place, you can have an income source consisting of investments, pensions, and savings that may ensure you live independently post-retirement.

Emergencies, be they health, accidental, or any other, usually never end. Even after one's retirement, unforeseen medical expenditures, financial crisis or costly home repairs, may arise at any time and reduce your savings. Retirement planning is vital to ensure a reliable emergency fund is in place to help you deal with all kinds of sudden and urgent financial needs.

There is a steady rise in the cost of food, utilities, healthcare, and other necessities over time. 15–20 years from now, what may seem affordable may become expensive. You can beat inflation by planning early. You won't have to compromise on your lifestyle since your retirement income maintains its purchasing power.

It is common for medical needs to increase as we age — doctor visits, medicines, tests, or possible hospitalisation. In India, healthcare inflation is higher than general inflation. Saving for future medical expenses and investing in products like health insurance or medical funds will help you avoid financial stress in the event of an emergency.

It usually takes time for wealth to grow, and patience, discipline, and appropriate investment choices are vital to achieve the desired results. Using a retirement calculator early on helps set realistic expectations and gives a clearer view of how investments may grow over time. Investing early is important, as it gives the investments more time to benefit from the compounding effect. Many times, a retirement calculator also highlights how small delays can impact the final corpus. Diversifying across a variety of products, like mutual funds, NPS, pension plans, and fixed-income investments can help build the required retirement corpus.

NPS, PPF, EPF, and pension plans are among the retirement schemes that offer tax9 benefits. With a planned approach, you can choose the right mix of tax-saving and retirement-building instruments to reduce your tax outgo today and enjoy tax-efficient withdrawals in the future. Over time, this will increase your total savings.

Our retirement calculator can help you in several ways, as listed below:

In India, there are different types of pension plans. You can use the pension plan calculator and find the suitable ones from the following options.

Pension schemes offered by governments provide individuals with financial security post-retirement. Typically, these schemes are funded through employer contributions, employee contributions, with government support. Furthermore, government schemes provide a steady source of income and help build long term financial security after retirement. This plan allows individuals to receive a predefined pension income after retirement.

The Employee Provident Fund (EPF) was introduced by the EPFO (Employee Provident Fund Organisation) in 1952. The plan aims to provide employees with financial security and stability after retirement. After crossing the age of 58, eligible employees with sufficient years of service can begin receiving a monthly pension under the Employee Pension Scheme (EPS)

Each month, 12 percent of an employee's basic salary plus dearness allowance is contributed towards the provident fund. A portion of the employer's contribution is separately directed to the Employee Pension Scheme (EPS). Private sector employees are required to participate, which offers various tax benefits.

A private pension plan is a retirement plan offered by an employer or another financial institution. Individuals can continue saving and investing post-retirement with this option. In addition, a private pension allows you to choose different investment strategies depending on your level of risk tolerance.

In this plan, you receive regular income either for life or for a chosen term, making it suitable for those who are retiring soon.

This plan lets you pay premiums in instalments over time, known as the accumulation period. Using a retirement calculator during this phase helps estimate how much needs to be invested to achieve a desired retirement income. Once this period ends, you start receiving pension payouts. It’s suitable if you want to plan early for retirement. A retirement calculator can help you understand how delaying payouts or increasing contributions can improve the final pension amount.

NPS is a government-supported retirement plan available to employees in the public, private, and organised sectors, as well as self-employed individuals. You can invest in a mix of equity and debt instruments and build a retirement corpus gradually.

With multiple pensions plans available, it’s important to choose one that matches your financial goals and retirement needs. A retirement and pension plan calculator helps you compare different options by estimating your future income based on inputs like your age, savings, investment amount, and retirement age.

Pension calculations are affected by the following factors:

Pension calculations are significantly influenced by economic factors. Here is a detailed description of inflation and interest rates.

Inflation, or the rate of increase in the price of goods and services, negatively impacts our purchasing power. With time, you will be able to buy comparatively a fewer amount of goods or services for the same price you pay. This significantly affects the standard of living, especially after retirement, if your pension amount doesn't account for long-term inflation.

The pension savings are often impacted by uncertain changes in the interest rates that determine the returns from different pension plans, especially the government-backed ones. Decrease in interests forces individuals to save or invest more to stay on track with their financial goals. So, monitoring interest rate fluctuatios is important to optimise your pension calculations.

There are a lot of factors that go into pension calculations, along with ensuring financial stability after retirement. The factors are then tailored based on each individual's needs and preferences.

Life expectancy is a key factor in retirement planning and asset allocation. It decides how long your savings must last. Individuals with longer life spans need higher savings. This helps maintain financial stability in later years. It also reduces the risk of running out of money.

Life expectancy affects contribution amounts and investment strategies. It also guides withdrawal planning. For example, someone expecting to live up to 90 years needs a stronger pension plan. In contrast, a shorter life span requires less funding. Lifestyle, medical history, and daily habits all influence life expectancy.

The lifestyle requirement plays an important role in determining pension needs. Those with a moderate standard of living might need less money than those with a higher standard. Hence, an individual's lifestyle preferences determine the need for pension income. In order to achieve your financial goals without worrying about the future, the income should be sufficient.

The overall costs one's healthcare needs may incur are quite an unpredictable factor. As the individual ages, the costs can increase, which may involve expenses from routine checkups to long-term treatments. You must carefully assess all the costs while estimating post-retirement needs. Moreover, those who have a known history of illnesses in their family should consider saving more for healthcare.

When planning retirement with pension calculators, it is crucial to take market factors into account. The returns and performance of investments have an impact on retirement savings. Below is a detailed breakdown of these factors:

You should consider an asset's past returns and future expected cash flows before investing your funds. For higher returns, you may invest in stocks, mutual funds, bonds, and other high-yield assets. However, market fluctuations can make returns unpredictable. To get high returns, you should choose the right investment strategy based on your risk appetite.

The overall performance of a pension fund also determines its future value. Savings can be negatively impacted if your chosen funds perform poorly. Therefore, you should review your investment plans regularly and switch to other investment plans if necessary.

Several calculations can be done with the help of a retirement calculator. It helps you to estimate how much money you need to save today to be able to get the desired income during retirement. It incorporates inflation rate and estimates rate of return to determine the retirement corpus you need to build to maintain your lifestyle even after retirement.

Based on the monthly saving required and the expected rate of return on investment, you may choose appropriate investment options.

A pension calculator is a practical tool that helps users understand, plan, and optimise their retirement savings with more clarity and control.

Understanding the purpose of your retirement plan is crucial to retirement planning. Based on your future financial commitments, you can opt for a pension plan with a regular income or a retirement plan with a lump sum benefit.

It is always better to go through all the available options, their features, benefits, and offerings, to ensure that you pick a retirement plan that is right for you. With a pension plan calculator, you can determine the desired annuity amount at an affordable premium by comparing the flexible features, such as the premium payment term, premium payment mode, and annuity option.

Ensure you are able to save the retirement funds as estimated with the monthly pension plan calculator. This is because the inflation rate and the interest rate are also calculated to help give you a better estimate of how much you need to save. If you need to cut down on some unnecessary expenses, consider it, but do not compromise on your retirement planning.

You can choose between different annuity plans. The deferred annuity plan allows you to receive the benefits after the premium payment term, while an immediate annuity if you want to invest a lump sum and receive the benefits soon after.

Once your retirement plan becomes mature, the pension benefits are paid out either as a lump sum, a regular income, or a combination of both for you to meet your goals. Most retirement plans offer regular income as a payout option.

Even though you may have other savings for emergencies, make some provision for emergency funds in your retirement planning as well. A medical emergency can require significant financial resources, depleting your savings. Hence, some extra savings can be beneficial.

A savings calculator helps you calculate the premiums you need to pay to get life insurance coverage for your family and also build a long-term savings corpus throughout the policy tenure.

With a term insurance calculator, you can understand how much life insurance cover is required to secure the financial future of your loved ones.

A Unit-Linked Insurance Plan or ULIP calculator enables you to know the returns you can receive on your policy and the premium amount you need to pay for the life insurance cover as well as investment.

1.

‘Current expenses’ in the pension calculator is the monthly amount spent to maintain your current standard of living, like housing, groceries, health and other lifestyle-related costs.

2.

‘Expected post-retirement expenses’ in a pension calculator are the amount you expect to spend after you retire, including rent, food, healthcare and discretionary spending like travel.

3.

Pension calculators help choose the right retirement plan by estimating your future needs and comparing different investment options based on your age, desired retirement age and expected expenses.

4.

It is important to use a retirement calculator before planning to invest in a retirement plan for the following:

● Determine an affordable premium for the required annuity amount.

● Find a suitable premium payment term & mode, and annuity option

● Make appropriate long-term financial planning decisions to ensure a dignified lifestyle.

5.

During retirement planning, consider your expected expenses, current savings, inflation, desired lifestyle, life expectancy, healthcare costs, and income sources such as pensions or investments.

6.

In India, the "optimal" pension depends on your lifestyle, location, healthcare needs, and inflation. In general, you may aim for a retirement corpus covering nearly two-thirds of pre-retirement monthly expenses.

7.

A good pension value allows you to maintain your desired standard of living after retirement. The amount should cover all your expenses, including inflation, and provide a buffer in case of emergencies.

8.

Your ten-year pension depends on retirement corpus, annuity rates, payout frequency, inflation, investment returns, lifestyle needs, retirement age, and chosen pension plan type.

9.

You become eligible for the pension income upon policy maturity. You can receive the accumulated funds in a lump sum, regular instalments (annuity), or a combination of both.

10.

The pension amount can be calculated using a pension calculator based on the amount you can invest in a retirement plan, affordable premium payment term, premium payment mode and desired annuity option.

11.

The pension amount can be calculated using a pension calculator based on the amount you can invest in a retirement plan, affordable premium payment term, premium payment mode and desired annuity option.

12.

To calculate your pension's present value, you must estimate your future pension payments, discount them at an appropriate interest rate, and sum them.

13.

Employees' Provident Fund (EPF) pension is calculated using the formula: Monthly Pension = (Pensionable Salary x Pensionable Service) / 70. The pensionable service is the number of years contributed to the EPS.

14.

In NPS pension calculation, contributions and investment duration determine the retirement corpus. A part of the corpus is converted into a lifetime annuity, depending on annuity payout and any lump-sum withdrawals.

15.

Yes, you can calculate the premium and the annuity amount for your retirement plan with the help of our Tata AIA Life Insurance Retirement and Pension calculator.

16.

A retirement calculator is a tool that helps people figure out how much they'll need to save for retirement based on their age, desired retirement age, and estimated living expenses.

17.

Retirement corpus requirements vary greatly based on one's needs and lifestyle. Consider your current expenses, expected inflation, desired lifestyle, and life expectancy while calculating.

18.

In retirement planning, it's wise to assume conservative annual returns of around 6% to 8%. Using realistic estimates ensures you don’t fail to achieve your retirement goals later.

19.

Set clear financial goals and save regularly for retirement. Invest according to your risk tolerance. Make sure you regularly review your retirement plan and adjust as needed.

20.

You should start retirement planning as soon as possible once you start earning. Planning for retirement as early as your 20s or 30s can help you achieve financial independence and stability in the long run.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Tata AIA Smart Pension Secure (UIN: 110L182V09) - Non-Participating, Unit Linked, Individual Life Insurance Pension Plan

The complete name of Tata AIA Fortune Guarantee Pension Plan is Tata AIA Life Insurance Fortune Guarantee Pension Plan (UIN:110N161V13) - A Non-Linked Non-Participating Annuity Plan

1 All funds open for new business which have completed 5 years since inception are rated 4 or 5 Star by Morningstar as of August 2025.

2 ©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

3 The word Guaranteed and Guarantee means the annuity payout is fixed at inception of the policy and will be payable for whole of life or till death of the Annuitant(s).

Some benefits are guaranteed, and some benefits are variable with returns based on the future performance of your insurer carrying on life insurance business. If your policy offers guaranteed benefits, then these will be clearly marked “guaranteed’ in the illustration table on this page. If your policy offers variable benefits, then the illustrations on these pages will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

6 Partial withdrawals only available 3 times during the entire policy term and only for reasons specified in IRDA Regulations as amended from time to time

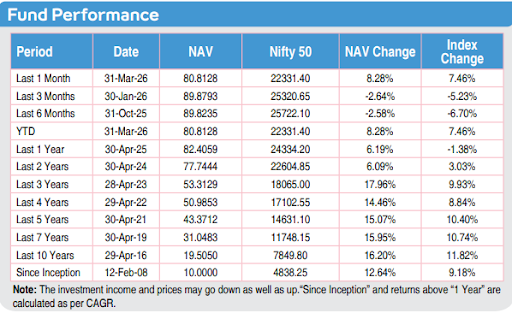

7Data from our Tata AIA fund fact sheet shows the performance of “Tata AIA Multi Cap fund” & SFIN NO: ULIF 020 04/02/08 FEP 110 as on Apr 2026. Benchmarked with Nifty 50

9Income Tax benefits would be available as per the prevailing income tax laws under old tax regime, subject to fulfilment of conditions stipulated therein. Income Tax laws are subject to change from time to time. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfilment of conditions stipulated therein. The Tax-Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

The products are underwritten by Tata AIA Life Insurance Company Limited. The plans are not guaranteed issuance plans, and it will be subject to Company's underwriting and acceptance. Whilst every care has been taken in the preparation of this content, it is subject to correction and markets may not perform in a similar fashion based on factors influencing the capital and debt markets; hence this advertisement does not individually confer any legal rights or duties. This is not an investment advice, please make your own independent decision after consulting your financial or other professional advisor.

The premium paid in Linked Life Insurance policies is subject to investment risks associated with capital markets and publicly available index. The NAV of the units may go up or down based on the performance of Fund and factors influencing the capital market/publicly available index and the insured is responsible for his/her decisions. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. On survival to the end of the policy term, the Total Fund Value including Top-Up Premium Fund Value valued at applicable NAV on the date of Maturity will be paid.

The fund is managed by Tata AIA Life Insurance Company Ltd. (hereinafter the Company).Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & Tata AIA Smart Pension Secure are only the names of the Unit Linked Life Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns. This is not an investment advice, please make your own independent decision after consulting your financial or other professional advisor.

Buying a Life Insurance policy is a long-term commitment. An early termination of the policy usually involves high costs, and the Surrender Value payable may be less than the all the Premiums Paid.

Life Insurance cover is available under the product. For more details on risk factors, terms and conditions please read sales brochure carefully before concluding a sale.

The products are underwritten by Tata AIA Life Insurance Company Limited.

The plans are not guaranteed issuance plans, and it will be subject to Company's underwriting and acceptance.

L&C/Advt/2026/Jun/4068