Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Term insurance is the type of life insurance. In exchange for a fixed premium, it provides financial protection for a specific... Read more period. The term insurance plan protects the financial needs of your dependants in the event of your absence. In the event of your death, your nominee will receive a death benefit that can be used to cover basic living expenses, such as food, clothing, healthcare, education, and so on. For example, a 27-year-old opting for a term insurance plan can ensure a ₹1 Crore life cover for his family at a low monthly premium, providing financial security in case of unforeseen events. Therefore, it is crucial that you purchase the best term insurance plan for your family's financial security. Read less

Get Life Cover of ₹1 Crore by paying a premium of

₹7,085/month

Total premium: ₹14.09 Lakh

Save ₹1,202 with discounts

Save ₹1,202 with discounts

Discounts

10% discount on 1st year premium is applicable on online purchase. This discount is auto-applied and can’t be removed

8.5% discount on 1st year premium is applicable for salaried personnel. You will need to share your corporate email ID if you opt for this discount. This discount is auto-applied if you select ‘Salaried’ as your occupation and can’t be removed

Applicable only if the policy is bought digitally. Some discounts will not be available when this option is selected.

1% discount on 1st year premium for all payments paid through any permissible electronic mode debited through an auto-debit mandate. Maximum discount capping: ₹100 over the year.

2% discount on 1st year premium on these milestones

| Event | Eligibility |

|---|---|

| Wedding (1 wedding only) | Within 6 months before or after the date of wedding |

| Birth/ Adoption of 1st child* | Within 6 months before or after the birth/ adoption date |

| Home loan | Within 6 months of loan getting sanctioned |

| First job | Within 6 months of joining date |

*Policy issuance eligibility for female customers will be determined by Board Approved Underwriting Policy (BAUP)

The above milestones cannot be clubbed to avail more discount, Such discount shall be capped to a maximum of ₹500 over the year.

Save up to 5% when you and a family member purchase policy together. Some discounts will not be available when this option is selected.

A certified Tata AIA expert will call you from a 1600‑series number to customize your plan.

Buy your plan

Please select an option

Minimum income: ₹5 Lakh

You opted for

Select details for the 2nd Policy

Select your relationship with the person you're buying this policy with.

Tata AIA Sampoorna Raksha Promise - Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V12)

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Success

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Failure

Your details could not be saved.

Please try again.

Your premium calculation is in progress

Term insurance policy is a basic form of life insurance offering financial protection for a specific period. The nominee of a term insurance policy will receive a financial benefit if you die during the policy period.

The purpose of term life insurance is to provide financial benefits only in the event of the policyholder's death during the term period. This policy does not return any financial value if you survive its term. You can choose term insurance with return of premium if you wish to get your premiums back after the policy term ends

When you buy term insurance, you pay regular premiums in exchange for a financial benefit that goes to your nominee in the event of your untimely demise

For example, a 30-year-old Akshay opts for a ₹1 crore cover for 30 years and pays around ₹12,000 annually. If something happens within those 30 years, Akshay’s family receives ₹1 crore. If not, the policy simply ends, unless there’s a return of premium feature.

Mr. Nakul, 30-year-old, Male, salaried professional

Life cover: ₹1 Crore

Annual Premium: ₹9,135

Pays premium term: 40 years

Gets Cover for: 30 years

Mr. Satish, 35-year-old, Male, salaried professional

Life cover: ₹1 Crore

Annual Premium26: ₹12,614

Pays premium term: 30 years

Gets Cover for: 40 years

Mrs. Lekha, 30-year-old, Female

Life cover: ₹1 Crore

Annual Premium27: ₹17,711

Pays premium term: 30 years

Gets Cover for: 30 years

Our bestselling Term Insurance plans

Choose a Tata AIA term insurance plan that suits your needs:

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product

(UIN:110N176V11)

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product

(UIN: 110N171V15)

Here is an example to help you understand our term plans better.

Share your needs and get

Non-Linked, Non-Participating, pure risk, Individual Life Insurance Product (UIN:110N176V11)

Tata AIA Sampoorna Raksha Promise

Get ₹1 Crore Life cover @ ₹826/month1

Age: 25

Cover till age: 60 yrs

Payment duration: 35 yrs

99.45%

Individual Death Claim

Settlement Ratio2

pay later option

Defer premium

by

12 months3

Instant Payout

on terminal illness

Purchasing a term insurance plan helps ensure financial security for your loved ones in your absence. Here is how a term insurance plan can help you

The following examples show why choosing the right term insurance plan is important at every stage of life.

The key features of term insurance plan are as follows:

Calculate Term Premium For 1 Crore

Gender

Male

Monthly premium

4T&C apply.

The following are some of the types of people who may consider buying a term insurance plan, depending on their life stage and responsibilities:

Term life insurance is important if you want to protect your family from financial challenges. It is helpful when you are the only earner in your family. Here are some important stages in life where term insurance becomes very important.

When you begin a family, your responsibilities increase. If something happens to you during this stage, term insurance provides a fixed amount to your nominee. This helps your family cover daily expenses.

Higher education needs good financial support. If you are not there when your child is ready for school or college, term insurance provides the assured amount to your nominee. This helps your child continue their studies without financial worries.

Weddings come with heavy expenses like jewellery and celebrations. In case of your untimely death, the term insurance amount can help your family arrange for your child’s wedding without financial pressure.

If you have a home, car, or personal loan, your family may struggle to repay the loans in your absence. If something happens to you, the insurance amount can help clear these debts. This prevents your family from dealing with unpaid EMIs.

Prices rise every year, making daily life more expensive. If you pass away, term insurance gives a fixed amount that helps your family keep their regular lifestyle. It also supports them in the long term, especially if you haven’t built large savings. This amount works as financial support in your absence.

Savings plan premiums are calculated based on measurable underwriting parameters. Here are the primary factors:

There are different types of term insurance plans you can choose based on your needs. Some of them are as follows:

Many individuals look for the best term insurance plan in India based on their life stage and goals. You can also use online tools to compare and find the best term plan.

The following table highlights the difference between a term life insurance policy and a whole life insurance plan:

Features

Term Life Insurance

Whole Life Insurance

Coverage Duration

Coverage lasts for a specific period chosen by the policyholder. Protection is provided only during this selected term.

Coverage under a whole life insurance policy continues for the insured’s entire lifetime, until age 10014, as long as premiums are paid regularly.

Premium Amount

The premium amount of a term insurance policy is typically lower because it covers a specific period.

The premium of a whole life insurance policy is higher because it includes lifelong coverage and offers additional long-term features.

Riders10

The best term insurance plans in India include useful riders10, such as critical illness, accidental death, and waiver of premium for enhanced protection.

Some whole life insurance plans also allow riders10, but they are more commonly used with term life insurance policies.

Payout Type

The nominee receives the sum assured if the policyholder dies during the selected term of the policy, provided all premiums are paid.

Pays the full sum assured on the policyholder’s death at any age, along with any accumulated savings or bonuses.

Bonus Eligibility

Not eligible for bonuses; designed solely for protection.

May offer bonuses such as loyalty additions or guaranteed accruals.

Loan/Withdrawal Facility

No loan or withdrawal options are available.

Loans and partial withdrawals are allowed after the lock-in period.

Surrender Value

No surrender value; policy lapses if premiums are unpaid.

Partial surrender value is available after a few years of continued premium payment.

Tax Benefits9

Premiums are eligible under Section 80C; death benefit exempt under Section 10(10D).

Same tax benefits as term plans, with added exemption on maturity proceeds under Section 10(10D).

The following table explains some of the best term insurance plans in India in 2026 and their key features:

Term Insurance Plan Type

Key Features

Key Features of Term Insurance Plan

Basic Term Insurance

This basic term insurance plan offers coverage for a chosen number of years. It provides a lump sum to your nominee in case of death during the policy term.

Increasing Sum Assured Plan

The sum assured increases every year by a fixed percentage. This helps deal with inflation and future financial needs, though premiums may be higher.

Term Insurance with Monthly Income

In addition to a lump sum payout, the term insurance with a monthly income plan provides a certain sum every month to the family. It may help manage household expenses after the policyholder’s death.

Return of Premium Term Plan

If the policyholder survives the policy term, the total premiums paid are returned, and the death benefit is still available during the coverage period.

Critical Illness Rider10 Term Plan

This plan allows you to add protection for specific major illnesses. On diagnosis of a listed condition, a lump sum is paid, based on rider10 terms.

Waiver of Premium Benefit

If the insured is diagnosed with a critical illness or suffers permanent disability, future premiums may be waived while the policy continues.

Accidental Death and Disability Cover

This rider10 offers an extra payout if death or disability occurs due to an accident. It can be added to enhance the base term plan coverage.

Group Term Insurance

This plan is often offered by employers to their employees. It provides financial cover for death or disability under group coverage terms.

Tata AIA's best Term Insurance plans in India

Tata AIA Sampoorna Raksha Promise - Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V11)

Tata AIA Maha Raksha Supreme Select - Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN: 110N171V14)

Non-Linked, Non-Participating, pure risk, Individual Life Insurance Product (UIN:110N176V02)

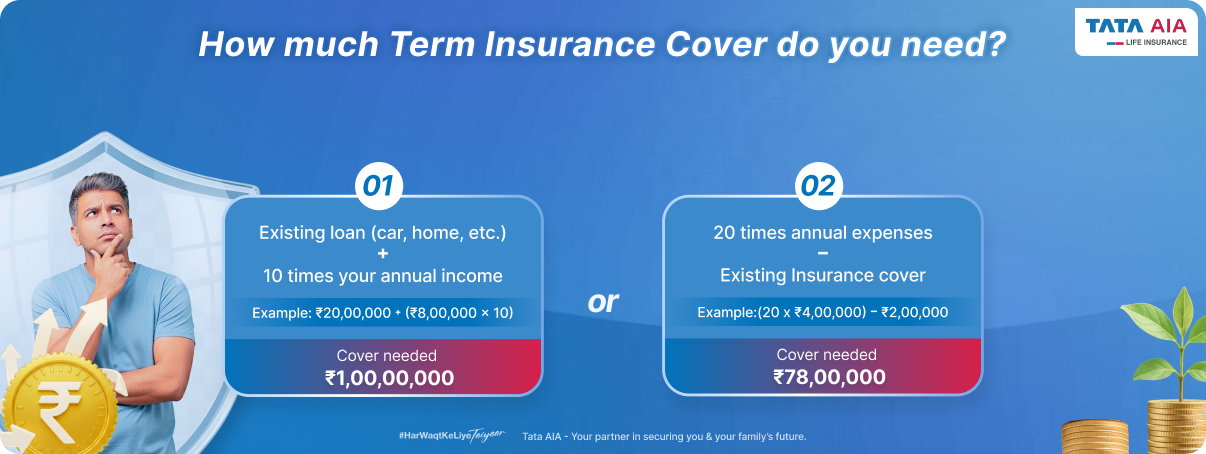

Before buying a term insurance policy, it is important to determine the sum assured your family should receive in your absence and ensure that it covers all their financial needs and emergencies.

Tata AIA Benefits: You can use our online term insurance calculator to understand the coverage you need to protect your family.

The term insurance premium is a regular, long-term amount. You need to assess and account for the same to better structure your budget. Hence, be sure that the amount of the term insurance premiums you choose to pay for your plan ensures sufficient coverage.

Tata AIA Benefit: Our term plan calculator helps you compare plans on the basis of the premium.

While you can purchase a policy as per your eligible age applicable for the product, it is always better to get a term plan as early as possible to avail of low term insurance premiums in return for higher insurance coverage for your family

Tata AIA Benefit: You can purchase a term insurance plan as early as from 18 years of age.

If your loved ones need a regular income for a fixed-period, you can go ahead with this choice or choose a lump sum payout. Alternatively, you can also choose a combination of a fixed-period income and a lump sum if it suits your beneficiaries.

Tata AIA Benefit: We offer multiple payout modes - Lump sum / Regular / Lump Sum+Regular: to help you secure your family in the best manner possible.

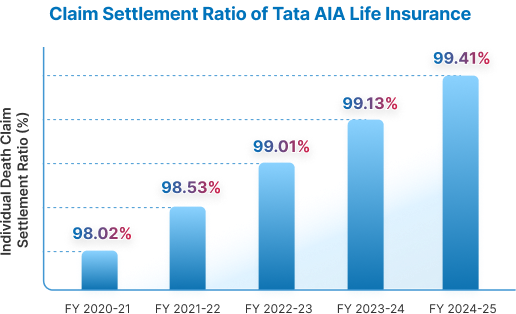

Consider the claim settlement ratio of the insurance provider, as it determines their ability to settle your claims effectively and on time when the need arises. The higher the claim settlement ratio, the better the chances of your beneficiaries receiving the claim on time.

Tata AIA Benefit: Tata AIA Life Insurance has an Individual Death Claim Settlement Ratio23 of 99.41% for FY 24–25.

Coose riders10 that offer benefits such as protection against critical illnesses, accidental death and disability, along with waiver of premium benefits tailored to unique needs for targeted protection against various circumstances.

Tata AIA Benefit: We offer a choice of add-on riders10 for protection to help you enhance your term plan protection.

Always ensure that the sum assured you select for your family’s needs also accounts for the inflation rates over the years. The financial needs your family has today will not be the same after 10 years, and so consider how much additional coverage they will need in the future.

Tata AIA Benefit: We offer a Life Stage Benefit16 with our term insurance plans to allow increasing the sum assured at important milestones, such as marriage, birth/adoption of a child, etc.

It is always better to compare term insurance plans and make an informed choice instead of picking the first plan you see. Comparing term policies helps you decide which features and benefits are best suited for your needs.

Tata AIA Benefit: We offer a wide range of term insurance plans, coverage options and protection + wellness combination solutions to suit varied insurance and budget needs. You can compare our plans here.

If you want to understand how to choose the best term insurance plan, you can get some help from your financial advisor or even contact your insurance company for further assistance.

Tata AIA Benefit: We offer round-the-clock assistance with our expert advisors. Book a call today to talk to our expert today.

Read the insurance policy’s terms and conditions. It helps you understand the plan in detail and most importantly, know what the policy does not cover. This can help your beneficiaries avoid any confusion regarding the policy and payouts.

Tata AIA Benefit: Detailed policy literature, including sales brochures, policy bonds, etc. is available online and can be accessed for an in-depth understanding. You can also access our vast repository of blogs and other supporting content for a detailed understanding of all products and services.

Selecting the best term insurance plan depends on many personal and financial factors. The following points may help you choose the suitable term insurance plan based on your needs.

The time taken for claim approval depends on how complete and accurate the submitted documents are.

Here’s a snapshot of our best term insurance plans:

Plan name

Tata AIA Sampoorna Raksha Promise: Life Promise

Tata AIA Maha Raksha Supreme Select: Life Secure

Entry Age (years)

Minimum

Minimum

Minimum

Maximum

Maximum

Maximum

Maturity Age (years)

Minimum

Minimum

Minimum

Maximum

Maximum

Maximum

Pay premium for (Premium Payment Term in years)

Minimum

Minimum

Minimum

Maximum

Maximum

Maximum

Stay covered for (Policy Term in years)

Minimum

Minimum

Minimum

Maximum

Maximum

Maximum

Life cover (Basic Sum Assured in Rs)

Minimum

Minimum

Minimum

Maximum

Maximum

Maximum

Premium payment mode

Death benefit

Option to cover till age of 100

Return of premium

Terminal illness cover

Early exit feature

Instant claim payout

FlexiPay (Pay later) benefit

Health benefit

Tax benefit on premiums paid

Tax on death benefit

Digital purchase discount

Salaried personnel discount

Female premium benefit

Milestone discount

Tata Group staff discount

Other discounts

Explanation

Premium payment term: Period for which premiums will be paid

Policy term: Period for which policy will remain active subject to premiums paid on time

Basic sum assured: Life cover provided under the policy

Single pay: Pay premium once

Limited pay: Pay premium for a defined number of years, lesser than the policy term

Regular pay: Pay premiums for the entire policy term

The right time to buy a term plan is when you start earning or when your financial responsibilities begin to grow. Basically, the earlier you start, the better it works for you.

| Life Stage / Situation | Why It Matters | How a Term Plan Helps |

|---|---|---|

Starting your career |

Premiums are lowest at this stage, and responsibilities are limited. |

You can lock in a low premium for a long time and start early. |

Getting married |

Financial responsibilities begin to increase. |

It helps protect your partner financially. |

Taking a home loan |

A long-term liability needs proper planning. |

The coverage can help repay the loan if needed. |

Becoming a parent |

Expenses increase with long-term goals like education. |

A higher cover secures your child’s future needs. |

Mid-career growth |

Income and responsibilities both increase. |

You can increase coverage or add riders. |

Self-employed |

Income may not always be stable. |

Flexible plans help maintain protection. |

Nearing retirement |

Focus shifts to remaining liabilities. |

It provides protection for the remaining working years. |

Term insurance premiums vary for each policyholder based on several factors. Understanding these factors can help you take steps to reduce your premiums.

Yes, NRIs can buy term insurance plans in India, as long as they meet basic eligibility conditions. Most insurers offer plans specifically designed for NRIs.

Typically, NRIs, PIOs, and OCIs can apply. You need valid documents like an Indian passport, age proof, and residence details.

In practice, the process is quite simple now. Many insurers allow online purchase with video KYC. Medical tests can be done in India or abroad. Premiums can be paid through NRE or NRO accounts, depending on the plan.

Term insurance in India is often more affordable compared to similar plans abroad. It also offers global coverage in most cases. Overall, it is a practical option for NRIs who want to financially protect their family in India

Sum assured in term insurance is the amount the policy beneficiaries get in case of the policyholder's demise when the policy is active. It is a guaranteed amount decided at the term plan’s inception as a death benefit against the policy.

Getting a sufficient sum assured is crucial when buying term insurance because it is the actual amount your family members will receive from the insurer. Thus, you must ensure that the sum assured is sufficient to cover your family’s continuing and future financial liabilities.

However, remember that the term insurance premium is directly affected by the sum assured. Selecting an unreasonably high sum assured can be a financial burden for you

Due to an increase in mortality risk, term insurance premiums increase with age. The risk of death increases with age, and so does the premium. Based on their assessment of risk, life insurance companies determine your premium. The following are the main reasons for higher premiums:

A younger person has a longer life expectancy, so the premiums of term life insurance plans are likely to last longer before a claim occurs. As the individual ages, the years that they have to pay premiums reduce, so a higher premium is needed to cover the same death benefit.

Diabetes, hypertension, heart problems, cancer and other diseases are more likely to develop as you age. As a result of these risk factors, insurers can increase the premiums on term life insurance plans for people with diabetes or other pre-existing conditions.

The life insurance industry transfers part of its risk to other companies known as reinsurers. Reinsurance costs also go up with age, which translates into higher premiums for policyholders.

Delay in purchasing term insurance can result in higher premiums, limited coverage, and increased financial risks for your loved ones. Act now to lock in affordable rates and secure your family's future.

Worried about the term insurance plans cost? Here are a few ways to get affordable term insurance:

When you buy a term insurance plan, you will be asked to name a policy nominee who will be entitled to the policy benefits in case of an unfortunate event. You must also select the term insurance payout option you want for the plan beneficiary.

Here are the various payout options you can choose from:

| Payout Option | Details | Example | When to Buy |

|---|---|---|---|

| One-time Lump Sum Payout | The most straightforward type of payout is the one-time lump sum method. Here, your policy nominee receives the entire sum assured for a death benefit as a single payment. | If you choose a sum assured of ₹2 Crore and name your spouse as the policy beneficiary, your spouse will receive ₹2 Crore as a single payment under covered situations. | If you are confident your beneficiaries will be able to manage the single lump sum amount efficiently or may require a significant amount for a major expense, you can opt for this payout option. |

| Fixed Monthly Payments | Under this payout option, your plan beneficiary receives the death benefit as regular payments from the insurer. Here, the sum assured acts as a regular source of income for your family in your absence. | If you choose a sum assured of ₹2 Crore and opt for a regular payout for 5 years, the sum will be divided into 60 units and paid out monthly. | Regular payouts are great if you want the death benefit to serve as a monthly income replacement. It is also better if the nominees are young and cannot manage a lump sum amount efficiently. |

| One-time Lump Sum + Fixed Monthly Payments | This option is a combination of the lump sum and regular payment options. Here, the policy nominee receives a part of the sum assured as a lump sum and the remaining amount as regular payments for a fixed tenure. You can decide how the death benefit is to be bifurcated between the two payment options here. | You choose a sum assured of ₹2 Crore and opt for a lump sum payment of 50% of the sum assured and the other 50% as a regular monthly payout for 5 years. In this case, ₹1 Crore will be paid out immediately to the beneficiary, and the remaining ₹1 Crore will be paid out over the next 60 months. | This option is perfect if you have any loans or other major financial liabilities that need to be repaid. The family can use the lump sum payout to clear any debts and then use the monthly payments for regular expenses. |

The following are some common types of term insurance riders10.

The following points may help you understand why term insurance riders10 are important.

A critical illness rider10 is an important add-on to your term insurance plan. It gives you a lump sum amount when you are diagnosed with a serious illness like cancer, heart attack, or stroke. The payout can be used for treatment, medicines, or daily household expenses. It supports you during times when you may not be able to earn because of health issues.

The top riders10 of Tata AIA term insurance plan are as follows:

The Tata AIA term insurance plan has many benefits, some of which are as follows.

The following is the eligibility criteria to buy a term insurance policy:

The following table lists what is covered and what is not in a term life insurance plan:

| What is Covered in Term Insurance? | What is Not Covered in Term Insurance? |

|---|---|

| Death due to natural causes such as illness, age-related complications, or medical conditions. | Death due to suicide in the first policy year is excluded under most term plans. |

| Death due to accident, including road, air, or other external incidents, is generally covered. | Non-disclosure of key facts, like smoking habits or existing illnesses, may result in rejection. |

| Terminal illness, if the rider10 is chosen, which allows early payout of the benefit before death. | |

| Critical illness rider10 pays a lump sum if diagnosed with listed illnesses like cancer or stroke. | |

| Accidental death rider10 provides extra payout in case of death due to a covered accident. |

Buying a term insurance plan is a responsible step, but many people make simple mistakes that affect its value. Avoiding these mistakes may help you choose the best term insurance plan in India for your needs.

Buy a term insurance plan online for the following benefits:

These are just suggestive documents, and the life insurance company may request additional documentation based on the policy conditions.

| Identity Proof | Address Proof |

|---|---|

|

|

The claim process for term insurance is as follows:

Understanding the following points may help you avoid claim rejection.

Here are the documents required to raise a term insurance claim.

| Document Type | Details |

|---|---|

| Claim Form | Duly filled form by nominee or legal heir |

| Death Certificate | Original or certified copy from local authority |

| ID Proof of Nominee | Government IDs such as Aadhaar, PAN or Passport |

| Address Proof of Nominee | Government IDs such as Aadhaar or Passport |

| Bank Details | Cancelled cheque (with name and account no. printed) along with bank passbook copy or bank statement |

| Medical Reports | Hospital records and medical history, if applicable |

| FIR/Postmortem Report | Required in accidental or unnatural death cases |

| FATCA/CRS Self Declaration | This form needs to be submitted in case of NRIs. Details can be checked here |

Note: Additional documents may be required asked on a case-to-case basis.

The time taken for claim approval depends on how complete and accurate the submitted documents are.

A GST is an indirect tax charged on term insurance premiums. Individual term insurance policies were taxed at 18% until 22 September 2025. For instance, a premium of ₹10,000 incurred an additional GST of ₹1,800, making the total payable amount ₹11,800.

However, from 22 September 2025, the GST on individual term insurance premiums is 0%. This makes term plans cost-effective and encourages more people to purchase pure protection insurance. The government implemented this reform to improve financial security. Here’s an overview.

Due to the new GST rate structure, term insurance sales are expected to increase, thereby advancing the vision of ‘Insurance for All by 2047’.

A strong Claim settlement ratio reflects the insurer’s consistency in fulfilling claim obligations over time. Tata AIA Life Insurance has consistently maintained a high Individual Death Claim Settlement Ratio over the past four financial years:

| Sr.no | Financial Year | Individual Death Claim Settlement Ratio (%) |

|---|---|---|

| 1 | FY 2025-26 | 99.45% |

| 2 | FY 2023-24 | 99.13% |

| 3 | FY 2022-23 | 99.01% |

| 4 | FY 2021-22 | 98.53% |

| 5 | FY 2020-21 | 98.02% |

The following are the key terms related to term life insurance plans:.

Source: IRDAI - First year premium of Life Insurers as on 31.12.2025 (https://irdai.gov.in/document-detail?documentId=8504103)

In the last financial year, 93% of Tata AIA Term customers opted for riders, with the most popular being accidental death cover, followed by critical illness. One of the key reasons for adding these riders is that, with a term plan, you lock in the rider premium for life, unlike health insurance where premiums can increase each year.

L&C/Advt/2026/Feb/0997

Customer reviews of our Term Insurance plans

Our experts are happy to help you!

Our experts are happy to help you!

Last updated on 04 Aug 2026

Reviewed by

Reviewed by