Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Claim Settlement Ratio (CSR) shows how many life insurance claims an insurer settles out of total claims received. This is... Read more calculated using the formula: Total Claims Settled x Total Claims Received x 100. A high CSR shows an insurer's reliability and commitment to honouring claims, ensuring policyholders' families are provided with timely financial support. Thus, CSR serves as an important indicator of trust and credibility when choosing a life insurer. Read less

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Your details could not be saved.

Please try again.

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Get Life Cover of ₹1 Crore by paying a premium of

₹7,085/month

Total premium: ₹14.09 Lakh

Save ₹1,202 with discounts

Save ₹1,202 with discounts

Discounts

10% discount on 1st year premium is applicable on online purchase. This discount is auto-applied and can’t be removed

8.5% discount on 1st year premium is applicable for salaried personnel. You will need to share your corporate email ID if you opt for this discount. This discount is auto-applied if you select ‘Salaried’ as your occupation and can’t be removed

Applicable only if the policy is bought digitally. Some discounts will not be available when this option is selected.

1% discount on 1st year premium for all payments paid through any permissible electronic mode debited through an auto-debit mandate. Maximum discount capping: ₹100 over the year.

2% discount on 1st year premium on these milestones

| Event | Eligibility |

|---|---|

| Wedding (1 wedding only) | Within 6 months before or after the date of wedding |

| Birth/ Adoption of 1st child* | Within 6 months before or after the birth/ adoption date |

| Home loan | Within 6 months of loan getting sanctioned |

| First job | Within 6 months of joining date |

*Policy issuance eligibility for female customers will be determined by Board Approved Underwriting Policy (BAUP)

The above milestones cannot be clubbed to avail more discount, Such discount shall be capped to a maximum of ₹500 over the year.

A certified Tata AIA expert will call you from a 1600‑series number to customize your plan.

Buy your plan

Please select an option

Minimum income: ₹5 Lakh

Tata AIA Sampoorna Raksha Promise - Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V12)

Claim settlement ratio is defined as how many claims an insurance company settled out of all claims they received in a financial year. As a result of insurance claim settlement ratios, you can usually tell whether a company is reliable or not when it comes to settling claims.

Usually, a higher ratio means that your claim will be settled on time. Therefore, the claim settlement ratio is an important indicator of an insurer's credibility since it indicates the likelihood of your claim being settled promptly and effectively.

You can find the claims settlement ratio of insurance providers on the official website of the Insurance Regulatory and Development Authority of India (IRDAI). Tata AIA Life Insurance can protect your family from a wide range of financial risks and emergencies by settling your claim on time.

Tata AIA Life Insurance aims to provide a stable record of CSR, with consistent Individual Death Claim Settlement Ratios in each of the past four years, with 98.02% in FY 2020-21, 98.53% in FY 2021-22, 99.01% in FY 2022-23, 99.13% in FY 2023-24, in 99.41% in FY24-25 and 99.45% in FY25-26. This gives assurance to policyholders and their families of getting dependable financial security in a tough time.

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V09)

Non-Linked, Non-Participating, Individual Life Insurance Savings Plan (UIN: 110N158V14)

Solution Composition

In this policy, the investment risk in investment portfolio is borne by the policyholder.

This advertisement is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme - Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Vitality Protect Advance - A Non-Linked, Non- Participating Individual Health Product (UIN: 110N178V01). These products are also available for sale individually without the combination offered/ suggested. This benefit illustration is the arithmetic combination and chronological listing of combined benefits of individual products. The customer is advised to refer the detailed sales brochure of respective individual products mentioned herein before concluding sale.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

105-year returns as of October 2025.

We have consistently improved our Claim Settlement Ratio over the years and these consistent figures highlight our unwavering commitment to settling claims promptly and efficiently.

When you purchase a life insurance policy from a life insurance provider, there are several factors you look at, such as the company’s offerings, the reviews by other customers and so on. However, the life insurance claim settlement ratio is the primary factor that should be researched and looked into when selecting a company as your life insurance provider.

Here are two important reasons why the claim settlement ratio can help you decide whether you should purchase your policy from the life insurance provider of your choice:

The calculation of the claim settlement ratio of your insurance provider is quite simple, and the figure can be arrived at with the help of the following formula:

Claim Settlement Ratio (CSR) = (Total number of approved claims / Total number of received claims) x 100

The arrived figure is always represented as a percentage. Hence, when a life insurance provider has an insurance claim settlement ratio of 90%, in simple terms, it means that the company has settled 90 claims out of the 100 claims they had received. A high percentage, such as the Tata AIA Life Insurance individual death claim settlement ratio of 99.45%1 in the FY 2025-26, is an indication of the company’s reliability.

A reputed life insurance provider not only honours claims within the regulatory Turn-Around-Time (TAT) but also ensures a smooth and convenient process. This makes it easier for customers to file their claims promptly . Insurance companies can also choose to disclose the total amount paid in claims and the number of policies successfully settled.

When a life insurance provider has a claim settlement ratio of 90% or above, it is generally considered to be a good claim settlement ratio. This is because 90% is an indication that the insurance provider has settled 90 of the 100 claims they have received during a financial year.

Every year, the insurer's claim settlement ratio changes based on how many claims they have successfully settled. An insurer that settles over 95% of claims consistently demonstrates strong financial reliability to buyers.

It's important to consider other things before choosing an insurance policy, like claims processing time, online reviews, sum assured offered, and premium amount.

Many people tend to hide information to receive their claims without providing proof. However, this can raise suspicion and lead to an investigation. By the end of the investigation the claim can be rejected if the policyholder's fraud is revealed and will negatively influence the insurance company's Claim Settlement Ratio.

Spend some time understanding the terms and conditions of the insurance policy properly. If you are unable to receive your claim settlement because you could not understand any of the policy exclusions, it leads to claim rejection.

If you, the policyholder, hold back or hide important information that could affect the claim process in any way, it will be considered as a case of fraud. Since such an instance prevents your insurance company from settling your claim.

In case of your untimely death, your insurer will help your nominee receive the death benefits through the due process. However, if you have been unable to update the correct nominee details or mention any changes, the insurer will not be able to help your nominee.

A consistent Claim Settlement Ratio (CSR) is important because it shows the reliability and stability of an insurance company to honour claims over time. If a CSR is high or stable year after year, it indicates that the insurer has a history of paying out claims quickly and fairly for its policyholders. This can be beneficial for those looking for financial security for their families. A consistent and high term insurance claim settlement ratio may also indicate that the insurer has an efficient claims processing system and transparent policies.

Choosing the insurer affects your Claim Settlement Ratio. Insurers with a higher CSR are more reliable and process claims quickly. If you choose an insurer with a lower CSR, you might face delays or higher claim rejections. It’s important to look at the CSR, customer service, and how easy it is to make a claim when selecting an insurer. A higher CSR generally means a smoother experience during claims.

Life insurance covers you and your family when you pay your premiums on time. When you miss a premium payment, there are provisions such as the grace period and policy revival to help you continue the life insurance coverage. In the case of unpaid premiums, it can affect the coverage benefits and even result in the claim being denied.

Letting your policy lapse puts your family's financial security at risk. Although you can revive the policy, subject to the policy terms and conditions, a slight delay or sudden emergency can cause quite a lot of problems when your nominee files the claim. A lapsed policy can't get any benefits if it hasn't been revived.

If your medical records are misrepresented or missing, your claims may be rejected. Hiding your smoking habits may result in lower premiums, but it always leads to claim rejection. Any medical condition should be disclosed to your insurance company when you purchase the policy.

An insurance company's claim settlement ratio is an important consideration before choosing an insurance provider, as it reflects their credibility and integrity. The claim settlement ratio of the last five years of Tata AIA Life Insurance is shown below.

Financial Year |

Individual Claim Settlement Ratio (CSR) |

FY 2020–21 |

98.02% |

FY 2021–22 |

98.53% |

FY 2022–23 |

99.01% |

FY 2023–24 |

99.13% |

FY 2024–25 |

99.41% |

FY 2025–26 |

99.45% |

Maturity claims and death claims are the two types of claims that you can file under a life insurance policy.

Under a life insurance policy, a death benefit is paid out to your family members, or the nominee/nominees named in the policy if you pass away during the policy term. Your nominee will be required to produce a set of documents requested by the company as proof of your death, such as the death certificate, doctor’s certificate and so on. The death benefit ensures that your family can sustain themselves financially in your absence.

A lot of life insurance policies, such as savings plans, retirement plans, ULIPs and endowment plans, come with maturity benefits which are paid out according to the policy once it matures. When a life insurance policy reaches its maturity date and the policyholder is alive, the insurer pays the maturity benefit as per the policy terms.

It can take longer to get your payment if you delay filing your claim. Anyhow, a life insurance company should pay out a death claim within 120 days.

From a policyholder's perspective, insurers with higher claim settlement ratios are better. It's because the higher number means there's a higher chance of claims being approved for the nominee/policy beneficiaries who filed a claim after the policyholder dies. Here are some things to consider when choosing an insurance company in India with a high claim settlement ratio:

IRDAI mandates that insurers publish quarterly and annual records of claims received, settled, and rejected on their websites. In the IRDAI Annual Report, all insurers in India provide this information. You can use this source as an authentic source to check the claim settlement ratio of different insurance companies for free.

Check the number of claims settled by the insurance company in a particular financial year. An insurer that processes more claims and maintains a high settlement ratio is preferred over one that processes fewer claims. Try to check the claim settlement ratio of the last 10 years.

Check how many claims the insurance company has resolved in a year. Insurers that handle a lot of claims and have a high settlement ratio are better than those that don't.

Find out what other consumers have to say about their experience with the insurer, especially concerning claim settlement. A positive review indicates that the insurer can provide a hassle-free claim settlement process.

Choose a company that offers easy access to customer service through a variety of methods. In this way, you can reach out to them for any future questions.

Claim form

Death certificate

Photo identification proof of the nominee

Current address proof of the nomine

Cancelled Cheque of the nominee

First Information Report

(in case of a claim due to an accident)

Post Mortem Report (if conducted)

Discharge summary / Death summary

(in case of hospitalisation)

For NRI customers

FATCACRS self-certification forms—Individual

FATCACRS self-certification forms—Non-Individual

Note: Tata AIA may ask for other documents, which are required on a case-by-case basis.

Mandatory documents

Claim form

Final Hospital Bill

Cancelled Cheque (Insured)

Photo identification proof of the Insured

All the related clinical reports about the claim event

ID/Address proofs

Accidental hospitalisation

MLC / FIR

First Immediate Consultation notes post-accident.

Critical illness

Report confirming the diagnosis of critical illness as per listed illnesses (Definition fulfilling document)

Attending Physician’s statement as applicable

Disability & Dismemberment

MLC/FIR

Attending physician’s statement confirming the permanent disability of the insured as applicable

Terminal Illness

Life expectancy certificate from two (2) independent Medical Practitioners specialising in the treatment of such illness, mentioning the irreversible terminal medical condition suffered by the insured and that is expected to result in the death of the insured within 6 months of diagnosis.

Certificate / Report specifying the terminal stage with all hospitalisation records & diagnostic reports.

Mandatory documents

Claim forms

Copies of hospital bills for the confinement & copies of all related clinical reports about the claim event

Attested true copy of Indoor Case Papers of the hospital

Discharge summary of present and past hospitalisations

Photo identity of life assured with age and address proof

Bank details of the claimant

Medical examination certificate

All related clinical reports pertaining to the claim event

Laboratory test reports

X-Ray / CT Scan / MRI reports & plates

Ultrasonography report

Histopathology report

Clinical / hospital reports

Angiography reports & plates

Certificate of Diagnosis

All follow-up consultation notes in relation to the hospitalized condition

All police reports / First Information Report & Final Investigation Report

Proof of accident - Panchnama / Inquest report

Newspaper cutting / photographs of the accident, if available.

Mandatory documents

Claim Forms

For Disability:

(Part I: Claimant's statement)

(Part II: Physician's statement)

For Dismemberment:

(Part I: Application form for dismemberment (life assured's statement))

(Part II: Dismemberment claim form (attending physician's report))

Attested true copy of indoor case papers of the hospital

Discharge summary of present and past hospitalizations

Photo identity of life assured with age and address proof (list of acceptable ID and address proofs of claimant)

Bank details of the claimant – Cancelled cheque (with printed name and account number) / bank passbook and NEFT form

All related medical examination reports

A disability certificate by the attending physician/institute for the disabled

Rehabilitation certificate, if applicable

Employer's written confirmation / statement — for disability claim

Clinical photographs showing the injured areas, if available

Valid records/proof showing death of the insured member due to floods, cyclones, or other natural calamities.

Claimant’s Statement (to be filled by nominee) with bank details of the nominee.

Photo ID, Address proof of the nominee and Relationship proof of the nominee with the insured.

Mandatory documents

Claim form

Death certificate

Photo identification proof of claimant

Current address proof of claimant

Cancelled Cheque of claimant

(ensure name and account number is printed on cancelled cheque with copy of bank passbook / bank statement).

First Information Report

(in case of claim due to accident)

Post Mortem Report

(if conducted)

Discharge summary / Death summary

(in case of hospitalisation)

For NRIs Customers

Note: We may ask for other documents, which is required on a case-by-case basis.

With our easy claim initiative, you can call our helpline to schedule an appointment for claim service at your doorstep. Our agent will visit your residence and help in completing the documentation and quickly initiate the claim process.

With our Express claim service, the beneficiary can submit the necessary documents with our agent who will initiate the claim process and ensure that the claim amount is received within 4 hours2. | 2T&C apply.

A life insurance claim rejection is not a desirable outcome. When you have life insurance, the death claim serves a valuable purpose. Maturity claims can be used primarily to fulfill financial goals, but death benefits will provide financial support for your family in the event of your death. Find out why a life insurance claim is rejected in order to prevent it from getting rejected:

Any document you send to the insurance company needs to contain the right information. All spellings, dates, and other details should match your official documents and identity proofs. A truthful disclosure of your lifestyle and health records is also required. Your nominee's information should be accurate so they do not face any difficulties when filing their claim.

Paying your premiums on time is crucial to receiving life insurance coverage for yourself and your loved ones. If you fail to pay the premiums, there are provisions such as the grace period and policy revival to help you activate your policy and continue coverage. Even so, it is always better to pay your premiums on time, since an untimely death, coupled with unpaid premiums, can affect your coverage benefits.

Letting your policy lapse is just as risky as not paying your premiums. You can revive the policy, subject to the policy terms and conditions, but a slight delay and sudden emergency can cause quite a lot of problems when your nominee attempts to submit a claim. Lapsed policies cannot be eligible for benefits if they have not been revived. In order to prevent this, you should not let your policy lapse.

It is common for claims to be rejected due to misrepresented, missing, and incorrect medical records. The act of hiding your smoking habits can lead to lower premiums, but it almost always results in claim rejections. Make sure your insurance company knows about any medical conditions you have, past or present, when you purchase the policy or whenever they are diagnosed. If you do this, your insurance company and policy may support you in any way possible to ensure your claim is not rejected and that you receive all the benefits you are entitled to.

A policyholder's occupation and hobbies are also taken into account by insurers when assessing risk. It is important to disclose high-risk jobs like mining, aviation or firefighting, as well as hobbies like skydiving, mountaineering, or deep-sea diving.

It is possible for claims to be rejected later on if certain information is omitted or misrepresented. When insurers receive honest disclosures, they are able to properly assess risk and price policies fairly, ensuring that your family is able to receive the claim amount.

Life insurance policies contain exclusions (situations in which claims are not payable). The most common exclusions are suicide within the first 12 months, illegal activity, and war-related deaths.

If the insured's death falls within these exclusions, the claim will be denied even if premiums were paid. Before purchasing a policy, policyholders should carefully read the exclusions section and explain them to nominees.

There are two ways to file the claim: online and offline.

Our customers trust us to be there when they need us the most. Here’s what some of them have to say:

Our experts are happy to help you!

The Individual death claim settlement ratio of Tata AIA Life Insurance in FY 25-26 is 99.45%1.

The life insurance claim settlement ratio is important because it is an essential indicator that your claims can be settled by your insurance provider in a timely and effective manner when needed. This ratio shows how many claims have been honoured by the insurance company in a given year as against the number of claims filed or received.

A claim settlement ratio of 90% or above is said to be a good claim settlement ratio for an insurance provider. However, each year, the claim settlement ratio can change, depending on how many claims the insurance company has been able to honour. And so, if you are looking for a reliable insurance company, you can look for a consistent track record of successful claim settlements in the last few years.

Factors such as fair disclosure of information, accurate nominee data, and fraud detection by the insurer affect CSR. Additionally, misstatement or non-disclosure may result in the rejection of claims, reducing CSR. The efficiency of claim processing by the insurer along with the financial strength, may also influence the CSR.

The life insurance claim settlement ratio is calculated as the percentage of claims successfully honoured by an insurance company. It is the number of claims that have been settled by the insurer out of all the claims received by them in a single year.

Hence, if the claim settlement ratio of a company is 98%, it means that the company has settled 98 out of 100 claims for that year. The claim settlement ratio can change every year depending on the company’s efficiency at claim settlement.

You can file a death claim and a maturity claim, depending on the situation and the type of claim that needs to be filed. For example, if the policyholder meets their untimely demise during the policy term, then the nominee can file a death claim. But if the policyholder survives the policy term, they can file a maturity claim on the maturity of the policy, if any.

The insurance claim is paid to the nominee specified in the policy upon the death of the policyholder. Legal heirs can also claim the amount with valid documents if no nominee is specified.

Yes, the insurance companies often expect nominees to inform them about claims as soon as possible after the policyholder's death. This may help to prevent unnecessary delays in the claim settlement process and tends to ensure smoother processing.

A death claim should be filed soon after the death of the policyholder during the policy term. Ensure that all the documents needed for the claim settlement, such as the death certificate, the policy document, etc., are submitted on time so that the claim can be filed correctly.

To file a claim, you can choose any of the following channels to reach out to us.

Email us at: customercare@tataaia.com

Call our helpline number - 1860-266-9966 (local charges apply)

Walk into any of the Tata AIA Life Insurance Company branch offices

Write directly to us at:

The Claims Department,

Tata AIA Life Insurance Company Limited

B- Wing, 9th Floor,

I-Think Techno Campus,

Behind TCS, Pokhran Road No.2,

Close to Eastern Express Highway,

Thane (West) 400 607.

IRDA Regn. No. 110

Please click here to know the list of documents needed for the claim intimation and settlement process.

Your insurance claim can be rejected if you do not disclose all the information required for the insurance company to settle your claim. Likewise, misrepresentation or misstatement of facts also leads to claim rejection. This means that you have provided incorrect information on the proposal form or held back some crucial information from the insurance company regarding your health, risks, etc.

Leaving the claim form incomplete and not providing all the details on the insurance proposal form are two of the most common mistakes people make while filing a claim. Unfortunately, both of these mistakes can lead to claim rejection.

Yes, Tata AIA Life Insurance enables you to file an online claim through our official website. Alternatively, you can also locate any of our office branches and visit us to file your claim.

Yes, you can track claim status through Tata AIA’s official website using your claim details.

Yes, a higher ratio indicates that the insurer has a strong history of honoring claims, giving policyholders greater confidence in the financial security of their loved ones.

Popular Searches

Last updated on 22 Jul 2026

Disclaimer

Tata AIA Sampoorna Raksha Promise - Non-Linked, Non-Participating, pure risk, Individual Life Insurance Product (UIN:110N176V09)

The complete name of Tata AIA Fortune Guarantee Plus is Tata AIA Life Insurance Fortune Guarantee Plus (UIN: 110N158V14) - Non-Linked, Non-Participating, Individual Life Insurance Savings Plan.

This advertisement is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). These products are also available for sale individually without the combination offered/ suggested. This benefit illustration is the arithmetic combination and chronological listing of combined benefits of individual products. The customer is advised to refer the detailed sales brochure of respective individual products mentioned herein before concluding sale.

1©2024 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India, and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates, or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

2Applicable to only non-early claims with more than 3 years of policy duration, non-investigation cases, up to Sum Assured of ₹50 Lakh. Applicable for branch walk in. Time limit to submit claim to Tata AIA Life Insurance is 2 pm on working days. Subject to submission of complete documents. Not applicable for ULIP policies and open title claims.

3The Individual Death Claim Settlement Ratio of Tata AIA is 99.45%, as per the latest annual audited figures for FY 2025-26.

4Illustrated premium of ₹501 is the monthly premium excluding taxes for a 20 yr. old female, Standard Life, Non-Smoker for ₹1 Cr. Sum Assured with Policy Term of 20 yrs. (Regular Pay) under Life Promise Option with first year premium discount of 10% for digital purchase and 8.5% for salaried person. Please refer Benefit Illustration for more details. Premium is subject to applicable taxes, cesses & levies which will be entirely borne/paid by the Policyholder, in addition to the payment of such Premium. Tata AIA Life shall have the right to claim, deduct, adjust, recover the amount of any applicable tax or imposition, levied by any statutory or administrative body, from the benefits payable under the Policy. Kindly refer the sales illustration for the exact premium.

5As per the duly approved product design and terms & conditions of the product. This includes first year digital discount of 10% for Limited Pay/Regular Pay and 8.5% salaried discount. For Single Pay, 1% discount will be available for online purchase and salaried discount each.

6Under Life Promise Plus Option, an amount equal to the 100% of the Total Premiums Paid (excluding loading for modal premiums) shall be payable at the end of the Policy Term, provided the life assured survives till maturity and the policy is not terminated earlier.

7Guaranteed Income shall be total of Guaranteed annual Income plus Income Booster payable in a year. Guaranteed Income as per the chosen Income Frequency shall commence after maturity till the end of the Income Period, irrespective of survival of the life insured(s) during the Income Period.

8Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfillment of conditions stipulated therein. For ULIP policies, maturity income will be taxable if annual aggregate premium exceeds ₹2.5 Lakh in a financial year. For non ULIP insurance policies, maturity income will be taxable if annual aggregate premium exceeds ₹5 Lakh in a financial year. Tax laws are subject to change from time to time. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Tax laws are subject to amendments from time to time. If any imposition (tax or otherwise) is levied by any statutory or administrative body under the Policy, Tata AIA Life Insurance Company Limited reserves the right to claim the same from the Policyholder.

9Available under Regular Income with an Inbuilt Critical Illness Benefit option

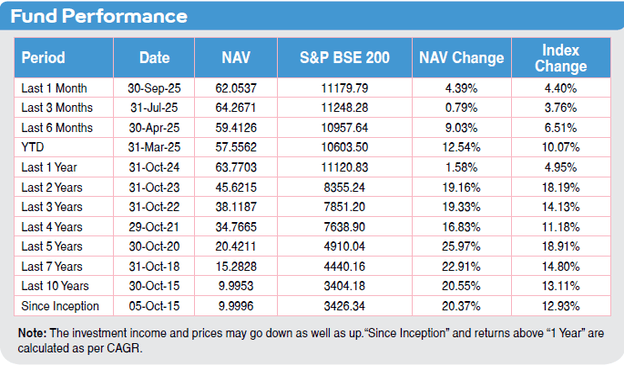

105-year computed NAV for Multi Cap Fund as of October 2025. Other funds are also available. Benchmark of this fund is S&P BSE 200.