Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Retirement and pension plans refer to different types of insurance or annuity plans that are specifically designed to support... Read more individuals after retirement. These plans help them manage their essential needs, like medical and daily expenses. Individuals have to make regular deposits to avail the pension, which can be regular payments (pension) or a lump sum amount on maturity. For example, a retiree may use the monthly pension to pay household bills and medical expenses, while the lump sum received at maturity can be used for major healthcare needs, home renovation, or fulfilling long-term goals such as travel or supporting family members. Read less

The purpose of retirement plans is to provide you with a reliable income stream even after you stop working. There are two general types of pension plans:

Non-Participating, Unit Linked, Individual Life Insurance Pension Plan

(UIN: 110L182V09)

Non-Linked Non-Participating Individual Life Insurance Plan

(UIN:110N161V13)

Retirement planning has become increasingly important due to longer life expectancy, rising medical expenses, and changing family structures.

Increasing healthcare and lifestyle costs

Rising inflation impacting retirement savings

Longer post-retirement life expectancy

Reduced dependence on traditional pension structures

Starting retirement planning early can help individuals build a larger retirement corpus through the power of compounding.

Since inflation has been on the rise, family dynamics have changed, and there is no social security system in India, planning your retirement is extremely important. The following are reasons why you need a retirement plan:

A retirement plan works in two simple stages over time. The following example explains how it works:

| Pension Scheme | Key Features/Description |

|---|---|

| Public Provident Fund (PPF) |

|

| Employee Provident Fund (EPF) & Employee Pension Scheme (EPS) |

|

| National Pension Scheme (NPS) |

|

| Atal Pension Yojana (APY) |

|

| Pradhan Mantri Vaya Vandana Yojana (PMVVY) |

|

| Senior Citizen Savings Scheme (SCSS) |

|

| Pradhan Mantri Shram Yogi Maan-Dhan (PM-SYM) |

|

| Annuity Type | Key Features/Description |

|---|---|

| Deferred Annuity |

|

| Immediate Annuity |

|

| Annuity Certain |

|

| Guaranteed Period Annuity |

|

| Life Annuity |

|

| National Pension System (NPS) |

|

| Unit-Linked Pension Plans (ULPPs) |

|

| Increasing or Escalating Annuity Plans |

|

| Pension Plans with Return of Purchase Price |

|

Retirement planning options differ based on flexibility, returns, and risk. The table below highlights key differences:

| Feature | Pension Plans | PPF | NPS |

|---|---|---|---|

Nature |

Life Insurance + investment |

Government backed savings scheme |

Market-linked retirement scheme open to all citizen |

Type of Returns |

Fixed or market-linked, depending on plan chosen |

Fixed (government-set), revised quarterly |

Market-linked |

Lock-in Period |

Long-term, align with chosen policy term |

15 years |

Till retirement (partial withdrawal allowed) |

Tax Benefits |

Section 80C / 10(10D) |

Section 80C |

80C + 80CCD(1B) |

Liquidity |

Limited |

Partial withdrawal allowed after 7 years |

Partial withdrawal allowed |

Annuity Requirement |

Yes, in many plans to provide regular post-retirement income |

Not applicable |

Partial mandatory |

Flexibility |

Moderate: Fund choice, premium options and rider addons available |

Low: Fixed structure with no customisation |

High: Choice of asset allocation, Fund manager, and investment mode |

Ideal For |

Structured and Long-term income planning |

Risk averse individuals seeking Safe savings |

Growth + retirement planning |

Withdrawal Options |

Structured payouts |

Lump sum |

Mix of lump sum + annuity |

Overall, pension plans are suitable for guaranteed3 income, PPF are suitable for safe savings, and NPS offers a balanced growth approach.

Here are some prominent features of retirement pension policies from Tata AIA:

Planning for retirement has become important because of the rising living costs, increasing healthcare expenses, and longer life expectancy in India.

Anyone planning to retire one day or who lacks sufficient corpus to support themselves after retirement will benefit from purchasing a retirement plan. During certain life stages, investments in retirement planning become particularly essential:

For calculating the pension returns, there needs to be a careful evaluation of the contributions, returns, time horizon, and external factors that affect the final retirement corpus.

To use a retirement planning calculator, follow the below steps:

Below is a comparative overview of the Tata AIA Fortune Guarantee Pension Plan and the Tata AIA Smart Pension Secure Plan:

| Parameters | Tata AIA Fortune Guarantee Pension Plan | Tata AIA Smart Pension Secure Plan |

|---|---|---|

| Premium Mode | Single premium and limited/regular premium options |

Regular premium payment only |

| Annuity Type | Immediate and Deferred annuity options available |

Deferred pension plan (benefits at vesting/maturity)

|

| Features | Multiple annuity options:

|

Offers:

|

Returns |

Guaranteed annuity payouts for life |

Market-linked returns via unit-linked funds (ULIP-based) |

Tax Benefits |

Eligible for tax benefits under Section 80CCC/80C and 10(10A), as per prevailing laws |

Eligible for tax benefits under Section 80C and 10(10D), as per prevailing laws |

There are several factors to be considered before investing in a pension plan. The following may be considered when choosing the best retirement plan in India:

An important aspect of retirement planning is estimating how much you will need in retirement. There is no fixed number because it depends on several factors, including age, lifestyle, financial goals, and others. To determine how much you need to save for retirement, consider the following factors:

Here are some of the important benefits of purchasing a pension plan online:

Tata AIA’s growing Assets Under Management (AUM) reflect the scale and consistency of professionally managed long-term investments. It’s another reason you can consider our plans. Here’s a snapshot.

| Financial Year | Total AUM (₹ Crore) |

|---|---|

| FY23 | 71,006 |

| FY24 | 99,207 |

| FY25 | 1,22,922 |

| FY26 | 1,45,589 |

A large and steadily growing AUM indicates long-term customer trust and disciplined investment management.

Planning retirement requires estimating future financial needs realistically. The Tata AIA Retirement Readiness Formula helps simplify this process.

Current Age |

Monthly Investment |

Investment Period |

@4%15 |

@8%15 |

@15.07%15 |

|---|---|---|---|---|---|

25 |

₹10,000 |

35 Years |

24.76 Lakh+ |

79.86 Lakh+ |

₹5.73 Cr+ |

30 |

₹10,000 |

30 Years |

21.83 Lakh+ |

58.01 Lakh+ |

₹3.02 Cr+ |

35 |

₹10,000 |

25 Years |

19.27 Lakh+ |

42.18 Lakh+ |

₹1.59 Cr+ |

40 |

₹10,000 |

20 Years |

17.03 Lakh+ |

30.71 Lakh+ |

₹84.46 Lakh+ |

Note: Returns shown are illustrative and not guaranteed.

Starting early allows investors to benefit from:

Long-term compounding

Lower financial burden through smaller regular contributions

Greater flexibility in risk management

Even a delay of 5–10 years can significantly reduce the final retirement corpus.

Feature |

Retirement Plans |

Mutual Funds |

Fixed Deposits |

PPF |

|---|---|---|---|---|

Retirement Focus |

High |

Moderate |

Low |

Moderate |

Life Cover |

Yes |

No |

No |

No |

Market-linked8 Growth |

Available |

Yes |

No |

No |

Guaranteed Income Options |

Available |

No |

Yes |

No |

Tax Benefits |

Applicable |

Limited |

Limited |

Applicable |

Long-term Discipline |

High |

Moderate |

Low |

High |

Life Stage |

Focus Area |

Suggested Approach |

|---|---|---|

20s |

Wealth accumulation |

Higher equity allocation |

30s |

Family protection + retirement |

Balanced allocation |

40s |

Corpus consolidation |

Moderate-risk approach |

50s |

Capital preservation |

Conservative allocation |

You should avoid the following mistakes while planning your retirement life.

L&C/Advt/2026/Apr/2568

The following are the eligibility criteria for a retirement plan in India:

The following is the list of documents that you need to buy a pension plan in India:

7T&C apply

Our experts are happy to help you!

Our experts are happy to help you!

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Tata AIA Smart Pension Secure (UIN: 110L182V09) - Non-Participating, Unit Linked, Individual Life Insurance Pension Plan

The complete name of Tata AIA Fortune Guarantee Pension is Tata AIA Life Insurance Fortune Guarantee Pension (UIN:110N161V13) - A Non-Linked, Non-Participating, Annuity Plan.

1All funds open for new business which have completed 5 years since inception are rated 4 star or 5 star by Morningstar as of August 2025.

©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

2Partial withdrawals only available 3 times during the entire policy term and only for reasons specified in IRDA Regulations as amended from time to time

3The word Guaranteed and Guarantee means the annuity payout is fixed at inception of the policy and will be payable for whole of life or till death of the Annuitant(s).

4Income Tax benefits would be available as per the prevailing income tax laws under old tax regime, subject to fulfillment of conditions stipulated therein. Income Tax laws are subject to change from time to time. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfilment of conditions stipulated therein. The Tax-Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

589,43,554 families protected till 31st May 2025.

6Individual Death Claim Settlement Ratio is 99.45% for FY 2025 - 26 as per the latest annual audited figures.

7Applicable to only non-early claims more than 3 years of policy duration, non-investigation cases, up to Sum assured of 50 lacs. Applicable for branch walk in. Time limit to submit claim to Tata AIA by 2 pm (working days). Subject to submission of complete documents. Not applicable to ULIP policies and open title claims.

8Market-linked returns are subject to market risks and terms & conditions of the product. The assumed rate of returns or illustrated amount may not be guaranteed and depends on market fluctuations.

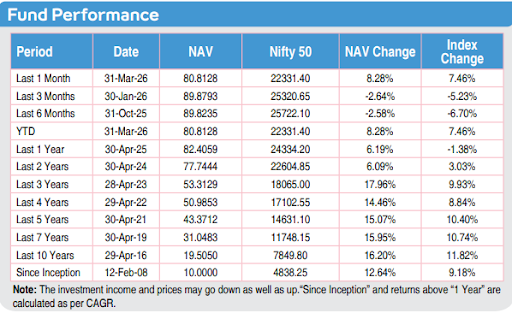

9Illustration shows monthly premium of ₹10,000 for Tata AIA Smart Pension Secure for a 30-year-old male, standard life, premium payment term: 10 years, policy term: 30 years with 100% investment in Tata AIA Future Equity Pension fund. 4% and 8% are assumed rates of return. 15.07% is the 5-year return of Tata AIA Future Equity Pension fund as of April'26. Maturity amount: ₹21,83,733 at 4% returns, ₹58,01,296 at 8% returns and ₹3,02,63,047 at 15.07% returns. The fund value calculation is done by projecting the past returns of Tata AIA Future Equity Pension Fund for 30 years after adjusting for all expenses in Tata AIA Smart Pension Secure Plan. The above values have been calculated assuming 15.07% CAGR, which is the past 5-year return of Future Equity Pension Fund projected for 30 years as of April'26. Benchmark of this fund is Nifty 50

105-year computed NAV for Future Equity Pension Fund as of April 2026. Other funds are also available. Benchmark of this fund is Nifty 50.

Some benefits are guaranteed, and some benefits are variable with returns based on the future performance of your insurer carrying on life insurance business. If your policy offers guaranteed benefits, then these will be clearly marked “guaranteed’ in the illustration table on this page. If your policy offers variable benefits, then the illustrations on these pages will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

11Source: https://www.pib.gov.in/PressReleasePage.aspx?PRID=2122148®=3&lang=2

12Rider is not mandatory and is available for a nominal extra cost. For more details on benefits, premiums, and exclusions under the Rider, please contact Tata AIA Life's Insurance Advisor/ branch.

13Loyalty additions and maturity boosters are only available for purchase through online/digital channels

14As on 31st March 2025, the company has a total Assets Under Management (AUM) of ₹130,053 Crore

15Illustration shows monthly premium of ₹10,000 for Tata AIA Smart Pension Secure for a 25,30,35,and 40 year-old male, standard life, premium payment term: 10 years, policy term: 35,30,25,20 years with 100% investment in Tata AIA Future Equity Pension fund. 4% and 8% are assumed rates of return. 15.07% is the 5-year return of Tata AIA Future Equity Pension fund as of April'26. Maturity amount for 25 years old, Policy term:35 years, Premium term: 10 years is ₹24,76,534 at 4% returns, ₹79,86,013 at 8% returns and ₹5,73,28,930 at 15.07% returns. Maturity amount for 30 year old, Policy Term:30 years, Premium payment Term: 30 years is ₹21,83,733 at 4% returns, ₹58,01,296 at 8% returns and ₹3,02,63,047 at 15.07% returns . Maturity amount for 35 years old, Policy term: 25 years, Premium Payment Term: 10 years is ₹19,27,521 at 4% returns, ₹42,18,459 at 8% returns and ₹1,59,81,690 at 15.07% returns. Maturity amount for 40 years old, Policy term: 20 years, Premium payment term: 10 Years is ₹17,03,317 at 4% returns, ₹30,71,686 at returns 8% and ₹84,46,112 at 15.07% returns. The fund value calculation is done by projecting the past returns of Tata AIA Future Equity Pension Fund for 35,30,25,20 years after adjusting for all expenses in Tata AIA Smart Pension Secure Plan. The above values have been calculated assuming 15.07% CAGR, which is the past 5-year return of Future Equity Pension Fund projected for 35,30,25,20 years as of April'26. Benchmark of this fund is Nifty 50

Unit Linked Life Insurance products are different from the traditional insurance products and are subject to the risk factors. Please know the associated risks and the applicable charges, from your Insurance Agent or Intermediary or Policy Document issued by the Insurance Company.

The fund is managed by Tata AIA Life Insurance Company Ltd. For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. The precise terms and condition of this plan are specified in the Policy Contract.

Past performance is not indicative of future performance. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any).

Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. Premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions

Investments are subject to market risks. The Company does not guarantee any assured returns. The investment income and price may go down as well as up depending on several factors influencing the market. Please make your own independent decision after consulting your financial or other professional advisor.

The fund is managed by Tata AIA Life Insurance Company Ltd. (hereinafter the “Company”). Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & Tata AIA Smart Pension Secure is only the name of the Unit Linked Life Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns

The performance of the managed portfolios and funds is not guaranteed, and the value may increase or decrease in accordance with the future experience of the managed portfolios and funds.

The investment income and price may go down as well as up depending on several factors influencing the market. Please know the associated risks and the applicable charges, from your Insurance Agent or the Intermediary or Policy Document issued by the Insurance Company. Please make your own independent decision after consulting your financial or other professional advisor. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any). All investments made by the Company are subject to market risks. The Company does not guarantee any assured return

Life insurance cover is available under the solution. For details on products, associated risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale

L&C/Advt/2026/Jun/3888

Last updated on 29 Jul 2026

Reviewed by

Reviewed by