Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Tata AIA introduces New Fund Offers (NFOs) under its market-linked plans. These offerings combine long-term investment opportunities... Read more with essential life insurance protection. NFOs are managed by asset management companies and provide dual advantages: financial security through comprehensive life cover and the potential to participate in equity market growth. Through a New Fund Offer, policyholders can access diversified investment portfolios while ensuring their family's financial well-being remains protected. Read less

New Fund offer

Investment Calculator

Premier SIP Calculator

Here’s your customised plan

Get Maturity Benefit

As per assumed rate of return

₹34.57 Lakh

As per actual past performance

₹70.50 Lakh

Total premium: ₹11.99 Lakh

Additional Benefits

Life Cover (including Terminal Illness Cover)

Accidental Death Cover

Accidental Total & Permanent Disability

Discount

Applicable if the policy is purchased digitally.

This discount is auto-applied and can't be removed

A certified Tata AIA expert will call you from a 1600‑series number to help customise your plan.

Buy Now

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP - Non-participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V01) and

Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually. Product option: Future Secure.

The primary objective of the fund is to generate capital appreciation by investing in India's top leading companies, that focus on innovation for long term value creation. The fund maintains flexibility to invest in carefully selected companies that offer opportunities across large or mid capitalization space. Its dynamic asset allocation allows 60%–100% investment in equity and equity-related instruments for growth potential.

The NFO meaning simply stands for New Fund Offer, which is the term used when a fund is introduced. These new fund launches introduce distinct investment approaches and portfolio strategies. Each NFO is designed with a clear investment objective, determining how your premiums will be allocated across different asset categories. The subscription period offers policyholders an opportunity to enter the fund at its inception, potentially benefiting from long-term wealth accumulation while maintaining life insurance protection throughout the policy term.

An NFO (New Fund Offer) is the initial phase when a new ULIP fund is launched. Now that you know the NFO full form, here’s how the process works:

The fund opens for initial investment for a limited period. During this window, you can allocate part of your ULIP premium to the new fund.

Your funds are converted into units, usually priced at ₹10 each during the NFO. The number of units you get depends on how much premium you allocate.

After the subscription closes, the fund manager starts investing according to the fund’s strategy and objectives.

Once the fund goes live, its NAV is updated regularly based on market movements. Your investment value rises or falls with the NAV.

The fund is actively monitored and adjusted over time. You can track performance through statements and decide whether to continue or switch to future premiums.

Overall, the process is transparent and helps you decide whether the new fund fits your long-term financial plan.

In this policy, the investment risk in investment portfolio is borne by the policy holder

Last 5 Years CAGR7 |

Since Inception CAGR8 |

|||

Tata AIA Funds |

Fund Return (%) |

Benchmark Return (%) |

Fund Return (%) |

Benchmark Return (%) |

Multi Cap Fund |

18.54% |

13.07% |

19.46% |

12.33% |

Top 200 Fund |

19.13% |

13.07% |

18.31% |

14.72% |

India Consumption Fund |

19.01% |

13.07% |

19.16% |

12.33% |

7Data as on Feb, 2026. Past performance is not indicative of future performance. Fund Benchmark: Multi Cap Fund – S&P BSE 200; India Consumption Fund - S&P BSE 200; Top 200 Fund - S&P BSE 200. SFIN: Multi Cap Fund – ULIF 060 15/07/14 MCF 110; Top 200 Fund - ULIF 027 12/01/09 ITT 110; India Consumption Fund - ULIF 06115/07/14 ICF 110. 8Inception Dates: Top 200 Fund: 12 Jan 2009, Multi Cap Fund: 05 Oct 2015, India Consumption Fund: 05 Oct 2015. Other funds are also available under this solution.

The different types of NFO are as follows:

These funds remain available for buying and selling even after the NFO period closes, and they do not come with a fixed maturity date. Their NAV updates regularly based on market movements, providing flexibility and general liquidity access. They are typically chosen by investors seeking long-term participation. Because they stay open, you may adjust your investment over time depending on personal financial preferences.

Close-ended funds operate for a set duration, generally between three and five years. Investments can be made only during the NFO window, but units might be traded on stock exchanges once the period ends. They often attract investors who prefer a fixed investment horizon. The closed structure helps maintain a steady fund size, which may support more consistent portfolio execution by the manager.

Interval funds combine features of both open-ended and close-ended formats, allowing purchases and redemptions during specific intervals. These provide occasional liquidity without continuous trading access. They are considered by investors looking for medium-term exposure with limited liquidity points. This format offers a balance between maintaining stability and meeting periodic withdrawal needs.

ETF NFOs follow specific indices, sectors, or commodities and are traded on stock exchanges like regular shares. They offer real-time market pricing and usually involve relatively lower operating costs. These funds are generally selected by individuals who prefer a passive investment style. Daily disclosure of holdings provides clarity on how the fund’s portfolio is structured.

A thematic or sector-focused NFO focuses on a specific theme or industry, such as technology, healthcare, energy, or infrastructure. The portfolio largely consists of companies operating within that segment, aiming to align with developments in that area. These funds carry varied return potential depending on how the theme evolves. They are typically considered by investors who have a specific outlook on a sector and are comfortable with associated fluctuations.

Index-based NFOs aim to reflect the performance of a selected market index by holding similar stocks in comparable proportions. As these funds replicate the index, their movements usually correspond with broader market trends. They provide a straightforward and cost-efficient way to gain market-linked exposure. This passive structure can help reduce the influence of individual stock selection and offer benchmark-aligned behaviour.

Asset allocation NFOs spread investments across different asset classes such as equity, debt, and money market instruments. The mix may stay constant or shift based on preset guidelines and market conditions. These funds work toward maintaining balance between stability and exposure to growth areas. They are suitable for investors who prefer a diversified framework that adjusts according to market changes.

Returns as of Apr'26. Fund ratings by Morningstar as of Apr'26.

A ULIP policy offers essential life cover to ensure financial protection for the policyholder’s family while also providing the opportunity to invest in the financial market based on their risk profile and financial goals.

NFOs are designed with specific financial objectives such as sustainability, growth potential, flexibility, stability, etc. Individuals can compare the investment options based on their objectives and choose a suitable ULIP fund option as per their risk appetite.

A ULIP Policy is a combination of insurance and investment, offering a single solution that addresses both financial protection and wealth creation goals.

Investors can choose to invest in the NFOs through a ULIP Policy to focus on long-term capital appreciation. It can help them plan and secure funds for their long-term financial objectives.

Amounts are based on a 20-year-old non-smoker male, with a 20-year premium payment term and a 30-year policy term, Future Secure plan option under the limited payment method with 100% invested in Tata AIA MultiCap fund at 8% Rate of Return.

Here’s why you should invest in NFOs.

Access to new strategies: NFOs introduce fresh strategies created by asset management teams, giving you exposure to themes, sectors, or indices that may not be available in your existing ULIP fund options.Early participation: Investing during the NFO stage lets you join a fund right from the start, giving you the chance to follow its entire journey as the portfolio develops.Better diversification: Adding a new fund can broaden your ULIP portfolio by bringing in different styles, sectors, or asset mixes, which may help balance overall risk.Professional oversight: Each NFO is managed by trained fund managers who research and monitor investments to keep the fund aligned with its stated objectives.Straightforward pricing: Since NFOs usually start with a fixed price, understanding your unit allocation becomes simple and transparent.More Choice and Flexibility: Frequent NFO launches let you refine your ULIP strategy over time, making it easier to adjust your investments as your goals or market conditions change.

Access to new strategies: NFOs introduce fresh strategies created by asset management teams, giving you exposure to themes, sectors, or indices that may not be available in your existing ULIP fund options.Early participation: Investing during the NFO stage lets you join a fund right from the start, giving you the chance to follow its entire journey as the portfolio develops.Better diversification: Adding a new fund can broaden your ULIP portfolio by bringing in different styles, sectors, or asset mixes, which may help balance overall risk.Professional oversight: Each NFO is managed by trained fund managers who research and monitor investments to keep the fund aligned with its stated objectives.Straightforward pricing: Since NFOs usually start with a fixed price, understanding your unit allocation becomes simple and transparent.More Choice and Flexibility: Frequent NFO launches let you refine your ULIP strategy over time, making it easier to adjust your investments as your goals or market conditions change.The NFOs are advantageous due to the following reasons.

NFOs are built using current market insights and evolving economic trends, helping the fund structure remain relevant to the present environment.

They come with well-defined objectives, risk levels, and asset allocation details, making it easier to judge whether a fund aligns with your financial plan.

By investing according to the fund’s theme or strategy, NFOs aim to contribute to long-term wealth-building efforts.

Your ULIP statements will show how the NFO is performing, allowing you to review progress and switch funds if you feel adjustments are required.

Because NFOs operate within a ULIP, you continue to get life insurance protection while your premium is also invested.

If an NFO doesn’t match your expectations over time, ULIPs generally allow you to move your funds to other funds available in the policy.

Fund managers bring research-driven insights and market experience to handle the portfolio; which may be difficult individually.

The following are the categories of investors who can invest in NFOs.

Long-term investors: NFOs may be suitable for those who can stay invested for many years to gain from potential capital appreciation and market growth.Investors looking for new strategies: Investors interested in exploring new fund strategies or asset classes can consider NFO investment to diversify their portfolio.Young professionals starting investments: Individuals starting their financial investments may invest in new NFO launch plans under ULIPs for long-term wealth creation and life cover.Investors seeking lower entry cost: As NFOs are usually priced at a fixed rate during launch, some investors may prefer them as an entry point into new funds.The following points need to be checked before investing in NFO:

Understanding the fund’s goal is important to know how it plans to generate returns and in which sectors it will invest.

The asset mix between equity, debt, and cash shows the level of risk and growth potential the fund holds.

Every NFO has a different level of market risk. Check if the fund’s risk aligns with your personal risk tolerance.

The skills and track record of the fund manager influence how well the fund is managed under different market conditions.

Check which index or benchmark the fund follows and what investment strategy is used to meet its objective.

Review if there are any charges for early withdrawal, fund management charges, or other policy-related costs.

Some NFOs may come with a lock-in period. It is important to check this before investing.

There are a few straightforward ways to invest in an NFO:

You can invest by connecting with a financial advisor or broker. They help you choose an NFO that fits your risk profile and financial goals, while also taking care of the paperwork and formalities. This option works well if you prefer personal guidance while making investment decisions.

Many people prefer using their bank’s investment portal or mutual fund apps to invest in NFOs. These platforms make it easy to complete transactions, track your portfolio, and access useful tools like comparisons and research insights. It’s a convenient choice for anyone who likes a quick, digital, and paperless process.

Various financial websites and fintech platforms list NFOs from multiple asset management companies. They provide all the key details in one place: fund information, features, and basic analysis. This makes it easier to review several options side by side and pick one that matches your investment plan.

Our experts are happy to help you

Looking to buy a new life insurance plan?

Our experts are happy to help you!

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Tata AIA Large Mid Cap Innovation Fund is a part of a various funds which a policyholder can choose from. For further details on funds, refer the sales brochure.

Tata AIA Large Mid Cap Innovation Fund - SFIN: ULIF 099 31/03/26 LMI 110

99.45% is the Individual Death Claim Settlement Ratio for FY 2025-26 as per latest audit figures

Param Raksha Life Pro + is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). These products are also available for sale individually without the combination offered/ suggested.

Param Raksha Life Pro is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, A Non-linked, Non-participating, Individual Health Product (UIN:110N183V01). These products are also available for sale individually without the combination offered/ suggested.

Param Raksha Life Maxima + is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, A Non-linked, Non-participating, Individual Health Product (UIN:110N183V01). These products are also available for sale individually without the combination offered/ suggested.

Param Raksha Life Growth + is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, A Non-linked, Non-participating, Individual Health Product (UIN:110N183V01). These products are also available for sale individually without the combination offered/ suggested.

Param Raksha Life Advantage + is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, A Non-linked, Non-participating, Individual Health Product (UIN:110N183V01). These products are also available for sale individually without the combination offered/ suggested.

Param Raksha Life Pro Advance is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, A Non-linked, Non-participating, Individual Health Product (UIN:110N183V01). These products are also available for sale individually without the combination offered/ suggested.

Tata AIA Smart Fortune Plus - Non-Participating, Unit Linked Individual Life Insurance Savings Plan (UIN: 110L177V01)

Tata AIA Pro-Fit comprises of Tata AIA Health Pro, A Non-Participating, Unit-linked, Individual Health Insurance Plan (UIN: 110L180V01), Tata AIA Health Secure, A Non- Participating, Unit Linked, Individual Health rider (UIN: 110A050V01) & Tata AIA Health Buddy, - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01).

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP, a non-participating, unit-linked, individual life insurance savings plan (UIN: 110L174V02), and Tata AIA Health Buddy, Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually.

The complete name of Tata AIA Wealth Pro is Tata AIA Life Insurance Wealth Pro (UIN: 110L111V05) – Non-Participating, Unit Linked, Individual Life Insurance Savings Plan

The complete name of Tata AIA Fortune Pro is Tata AIA Life Insurance Fortune Pro (UIN: 110L112V07) – Non-Participating, Unit Linked Individual Life Insurance Savings Plan.

The complete name of Tata AIA Wealth Maxima is Tata AIA Life Insurance Wealth Maxima – Non-Participating, Unit Linked Individual Life Insurance Savings Plan (UIN:110L114V05)

The complete name of Tata AIA Fortune Maxima is Tata AIA Life Insurance Fortune Maxima - Non-Participating, Unit Linked Individual Life Insurance Savings Plan (UIN: 110L113V09)

Tata AIA Smart SIP - Non-Participating, Unit Linked Individual Life Insurance Savings Plan (UIN:110L174V02)

Shubh Muhurat Solution is a combination of Tata AIA Life Insurance Fortune Guarantee Secure (Individual, Non-Linked, Non-Participating, Life Insurance Savings Plan) UIN:110N206V03 and Tata AIA Life Insurance Smart Fortune Plus (Unit Linked, Individual Life Insurance Savings Plan)-UIN:110L177V01. Tata AIA Life Insurance Fortune Guarantee Secure and Tata AIA Life Insurance Smart Fortune Plus are also available for sale individually.

Shubh Fortune Solution is a combination of Tata AIA Life Insurance Fortune Guarantee Secure (Individual, Non-Linked, Non-Participating, Life Insurance Savings Plan) UIN:110N206V03 and Tata AIA Life Insurance Smart Fortune Plus (Unit Linked, Individual Life Insurance Savings Plan)-UIN:110L177V01. Tata AIA Life Insurance Fortune Guarantee Secure and Tata AIA Life Insurance Smart Fortune Plus are also available for sale individually.

Tata AIA i Systematic Insurance Plan - Non-Participating. Unit Linked Individual Life Insurance Savings Plan (UIN:110L164V10)

Tata AIA Health SIP - A Non-participating, Unit Linked, Individual Health Insurance Plan (UIN:110L184V01)

Tata AIA Shubh Health Plus comprises of Tata AIA Health SIP - A Non-Participating, Unit-linked, Individual Health Insurance Plan (UIN: :110L184V01), Tata AIA Health Buddy, A Non-linked, Non-participating, Individual Health Product (UIN: 110N183V01 or any other later version). Tata AIA Health SIP and Tata AIA Health Buddy are also available individually for sale.

Asset Allocation: Equity & Equity related instruments: 70%-100%, Debt: 0%, Cash / Money Market Instruments, Bank Deposits and Mutual Funds: 0 – 30%

1Illustration shows a monthly premium of ₹15,000 for Tata AIA Premier SIP + for a 20-year-old male, standard life, premium payment term: 12 years, policy term: 30 years with 100% investment in Tata AIA Large midcap innovation fund in Future Secure plan option. 4% and 8% are assumed rates of return. 14.88% is the 5-year return of Nifty 500 Index as of February'26. Maturity amount: ₹10,80,024 at 4% returns, ₹35,20,478 at 8% returns and ₹ 4,36,93,547 at 14.88% returns. The fund value calculation is done by projecting the past returns of Nifty 500 Index after adjusting for all expenses in Tata AIA Premier SIP. The above values have been calculated assuming 14.88% CAGR, which is the past 5-year return of Nifty 500 Index Fund as of February'26.

Some benefits are guaranteed, and some benefits are variable with returns based on the future performance of your insurer carrying on life insurance business. If your policy offers guaranteed benefits, then these will be clearly marked “guaranteed’ in the illustration table on this page. If your policy offers variable benefits, then the illustrations on these pages will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

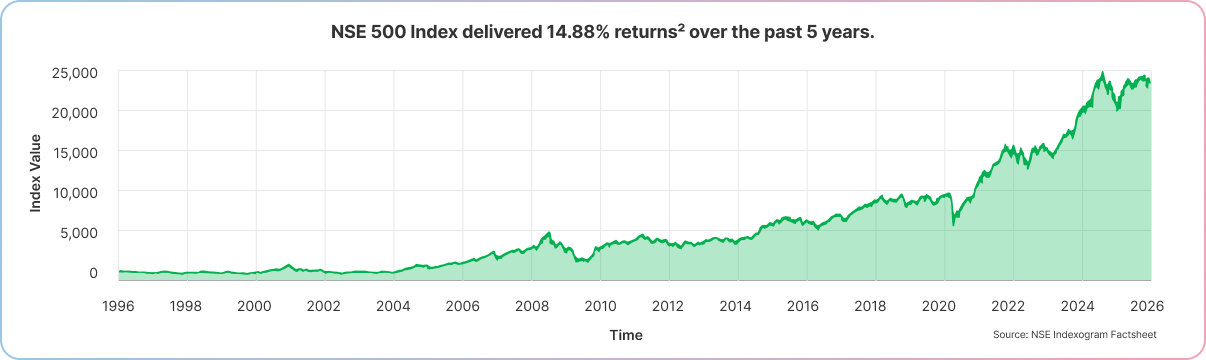

2Benchmark Fund: NSE 500 Index. Data as of February, 2026. Source: https://www.niftyindices.com/market-data/return-profile

3No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfilment of conditions stipulated therein. The Tax-Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

4All funds open for new business which have completed 5 years since inception are rated 4 or 5 Star by Morningstar as of August 2025.

5Market-linked returns are subject to market risks and terms & conditions of the product. The assumed rate of returns or illustrated amount may not be guaranteed and depends on market fluctuations.

5©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

6Data as on Dec 31, 2025. Past performance is not indicative of future performance. Fund Benchmark: Multi Cap Fund – S&P BSE 200; India Consumption Fund - S&P BSE 200; Top 200 Fund - S&P BSE 200. SFIN: Multi Cap Fund – ULIF 060 15/07/14 MCF 110; Top 200 Fund - ULIF 027 12/01/09 ITT 110; India Consumption Fund - ULIF 06115/07/14 ICF 110.

7Inception Dates: Multi Cap Fund: 05 Oct 2015, India Consumption Fund: 05 Oct 2015, Top 200 Fund: 12 Jan 2009. Other funds are also available under this solution.

8Tax benefits of up to ₹46,800 u/s 80C is calculated at highest tax slab rate of 31.20% (including cess excluding surcharge) on life insurance premium paid of ₹1,50,000 as per old tax regime. Tax benefits under the policy are subject to conditions laid under Section 80C, 80D,10(10D), 115BAC and other applicable provisions of the Income Tax Act,1961. The Tax-Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961.Tax laws are subject to amendments made thereto from time to time. Please consult your tax advisor for details, before acting on above

9As on 31st Oct 2025, the company has a total Assets Under Management (AUM) of ₹1,40,345 Crores

1089,43,554 families protected till May 31, 2025

11©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

Unit Linked Life Insurance products are different from traditional insurance products and are subject to risk factors. The premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of funds and factors influencing the capital market and the insured is responsible for his/her decisions. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. The underlying Fund’s NAV will be affected by interest rates and the performance of the underlying stocks. The fund is managed by Tata AIA Life Insurance Company Ltd. (hereinafter the Company"). The performance of the managed portfolios and funds is not guaranteed, and the value may increase or decrease in accordance with the future experience of the managed portfolios and funds. Past performance is not indicative of future performance. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any). All investments made by the Company are subject to market risks. The Company does not guarantee any assured returns. The investment income and price may go down as well as up depending on several factors influencing the market. Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the insurance company.

The products are underwritten by Tata AIA Life Insurance Company Limited. The plans are not guaranteed issuance plans, and it will be subject to Company's underwriting and acceptance. Whilst every care has been taken in the preparation of this content, it is subject to correction and markets may not perform in a similar fashion based on factors influencing the capital and debt markets; hence this advertisement does not individually confer any legal rights or duties. This is not an investment advice, please make your own independent decision after consulting your financial or other professional advisor.

The fund is managed by Tata AIA Life Insurance Company Ltd. (hereinafter the Company).

Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & the Unit linked insurance product with Tata AIA /Tata AIA Life Insurance as its prefix is only the name of the Unit Linked Life Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

Buying a Life Insurance policy is a long-term commitment. An early termination of the policy usually involves high costs, and the Surrender Value payable may be less than the all the Premiums Paid.

Insurance cover is available under the product. For more details on risk factors, terms and conditions please read sales brochure carefully before concluding a sale.

The products are underwritten by Tata AIA Life Insurance Company Limited.

L&C/Advt/2026/Mar/1897