![]() Get Life cover till 100 years1

Get Life cover till 100 years1

Endowment Policy

Fulfil your life goals with our Endowment Plans

Fulfil your life goals with our Endowment Plans

-

100% Guaranteed2 Returns

-

Tax-free3 Returns

-

Inbuilt Life Cover

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Get Life Cover of ₹1 Crore by paying a premium of

₹7,085/month (for 30 years)

₹8,287/month

Save ₹1,202 with discounts

Save ₹1,202 with discounts

Excludes GST

Our sales representative will connect with you soon to assist further

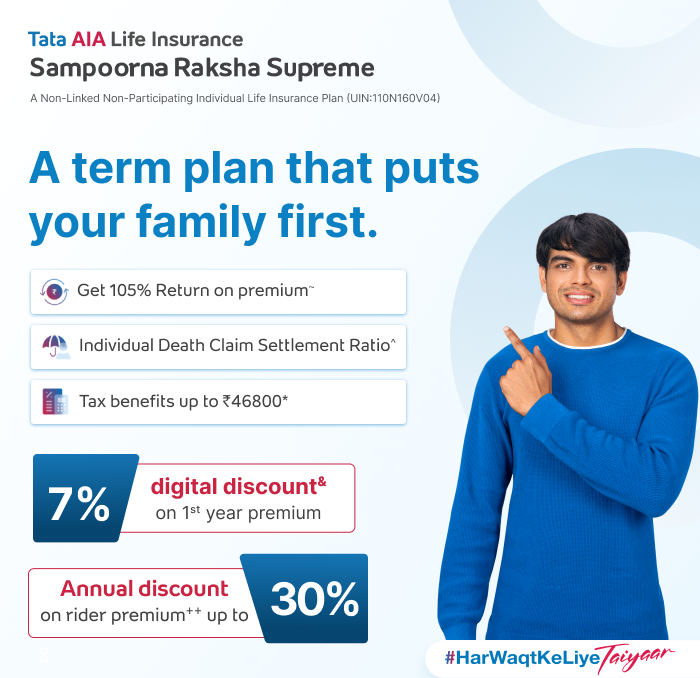

Tata AIA Life Insurance Sampoorna Raksha Promise (A Non-Linked Non-Participating, Pure Risk, Individual Life Insurance Plan) • UIN: 110N160V7

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Your details could not be saved.

Please try again.

https://author1westindia-28595824.prod.talic.adobecqms.net/editor.html/life-insurance-plans/term-insurance/2-crore-term-insurance.html

https://author1westindia-28595824.prod.talic.adobecqms.net/editor.html/life-insurance-plans/term-insurance/50-lakh-term-insurance.html

Term Insurance Calculator

Term Insurance Calculator

https://author1westindia-28595824.prod.talic.adobecqms.net/editor.html/term-plan-with-return-of-premium.html

https://author1westindia-28595824.prod.talic.adobecqms.net/editor.html/life-insurance-plans/term-insurance/term-insurance-for-women.html

Term Insurance Calculator

Term Insurance Calculator

https://author1westindia-28595824.prod.talic.adobecqms.net/editor.html/life-insurance-plans/term-insurance/term-insurance-for-nri.html

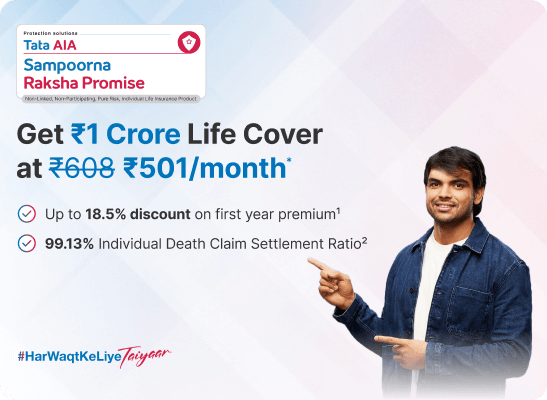

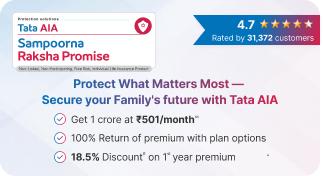

Get ₹1 Crore Life Cover at ₹501/Month1

Get ₹1 Crore Life Cover at ₹501/Month1

Sampoorna raksha Promise

Start building your wealth today to enjoy the power of compounding on your investment!

When you budget your finances, an understanding of how compounding works can help guide you in making informed decisions. A compound interest calculator is a useful tool that allows you to estimate how your investments will grow over time.

Unlike simple interest, which is calculated only on the principal amount, compound interest calculates interest on both the principal and on the interest already earned in previous periods. This means that with each compounding period (monthly, quarterly, or annually), your investment grows more rapidly.

The frequency of compounding and the time you stay invested play a major role in how the final amount grows. Over the years, this effect can result in a larger amount when compared to the simple interest amount.

Using a calculator, it is easier to see how different amounts, time frames, and rates can impact your overall investment worth.

Read on to learn more about how compound interest works.

people have explored this plan recently!

Investment Calculator

Investment Calculator

In India, there are four types of endowment policies:

Traditional Endowment Plans

These are traditional life insurance plans that combine the benefits of insurance and savings. Under a traditional endowment plan, the policyholder pays premiums for a certain period, and upon maturity of the policy, the policyholder receives a lump sum payout.

Unit Linked Endowment Plan

These are insurance plans that combine the features of both insurance and investment. A part of the premium amount is invested in equity or debt securities. The policyholder can choose the desired fund, and returns are based on the fund’s performance.

Non-Profit Endowment Plan

Under this type of endowment policy, a maturity amount is paid to you at the end of the policy term, or a lump sum benefit will be paid out to your nominee in the event of your unfortunate demise. These policies are known as non-profit endowments because the life insurance policy does not comprise any additional bonuses. Therefore, the guaranteed2 payout will remain the same as the amount pre-determined at the time of policy purchase.

Low-cost Endowment

The premium amount under this type of endowment plan is low, which helps you save your money for future payments. A certain amount is guaranteed2 to be paid out on maturity; in the event of your death, your nominee will receive the same. Moreover, yearly bonuses, as and when declared, will be payable, which boosts the maturity corpus. Hence, these plans can help you accumulate a financial fund within a defined period.

Fulfil your life goals with our Endowment Plans

Fulfil your life goals with our Endowment Plans

100% Guaranteed2 Returns

Tax-free3 Returns

Inbuilt Life Cover

Our Easy Claim Initiative offers doorstep claim service where beneficiaries can schedule an appointment via our helpline, and our agent will assist with documentation and expedite the claim process at their residence.

Also, with our Express Claims15 service, the beneficiary can submit the necessary documents with our agent who will initiate the claim process and ensure that the claim amount is received within 4 hours.

15T&C apply

Voice of happy customers

Tata AIA Sampoorna Raksha Promise

Plan Option |

|

Life promise |

Life Promise Plus |

Entry Age (Years) |

Minimum |

18 |

18 |

Maximum |

65 |

65 |

|

Maturity Age (Years) |

Minimum |

18 |

28 |

Maximum |

100 |

100 |

|

Pay Premium For (Premium Payment Term in Months)

|

Minimum |

• Single Pay

|

• Single Pay

|

Maximum |

• Single Pay

|

• Single Pay

|

|

Stay Covered For (Policy Term in Months) |

Minimum |

• Single Pay - 60

|

• Single Pay - 120

|

Maximum |

• Single Pay - 564 |

• Single Pay - 564 |

|

Life Cover Amount (Base Sum Assured in Rs) |

Minimum |

25 lakhs |

25 lakhs |

Maximum |

No Limit

(Subject to Board approved underwriting policy (BAUP)) |

No Limit

(Subject to Board approved underwriting policy (BAUP)) |

|

Premium Payment Mode

|

Single Pay Annual Semi-annual Quarterly Monthly |

Single Pay Annual Semi-annual Quarterly Monthly |

|

Death Benefit |

Highest of: • 1.25 x Single Premium (excluding discount) or DB multiple x Annualised Premium (excluding discount) • 105% of Total Premiums Paid (excluding loading for modal premiums and discount) up to date of death; or • An absolute amount assured to be paid on death |

Highest of: • 1.25 x Single Premium (excluding discount) or DB multiple x Annualised Premium (excluding discount) • 105% of Total Premiums Paid (excluding loading for modal premiums and discount) up to date of death; or • An absolute amount assured to be paid on death |

|

Option To Cover till Age Of 100 (Whole Life Coverage)10

|

Yes |

Yes |

|

Option To Get Your Premium Amount** Back |

No |

Yes |

|

Increase Life Cover at Important Milestones* such as Marriage/Childbirth/home loan/First Job |

Available |

Available |

|

Terminal Illness Cover |

No |

Payor accelerator benefit is payable on confirmed diagnosis of terminal illness of the life assured |

|

Health Benefit |

Available with Riders |

Available with Riders |

|

Income Benefit

|

No |

No |

|

Tax Benefit Up to Rs. 46,8009 |

Yes |

Yes |

|

Upfront Premium Discount |

discount of 1% of single premium or 5% on First year premiums for regular and limited pay. |

discount of 1% of single premium or 5% on First year premiums for regular and limited pay. |

|

2T&C apply

13T&C apply.

Get personalized guidance to choose the best-fit insurance plan for your specific needs.

Lorem ipsum dolor sit amet consectetur. Magna vestibulum urna in tellus in porta suspendisse dui. Parturient cursus ultricies commodo lectus condimentum odio auctor blandit fringilla. Nisl urna in ornare mi lectus pretium. Sagittis amet curabitur pharetra hendrerit venenatis. Pellentesque sagittis tempor vitae ut adipiscing nibh sit condimentum.

Quisque nisi purus dictum odio massa sit ac consectetur eget. Diam aliquet a libero tellus suspendisse habitant morbi commodo. Vitae sed erat tellus orci facilisi et aliquam consectetur quisque. Blandit ornare facilisi sagittis velit id. Adipiscing sapien elit tellus accumsan arcu mi. Eget vitae dictum sagittis tempor vitae odio non risus. Adipiscing ornare quis odio bibendum sapien sed vel morbi massa. Mauris sem odio arcu sollicitudin. Vitae hendrerit dui id cras diam ut vitae rhoncus consectetur.

Lorem ipsum dolor sit amet consectetur. Magna vestibulum urna in tellus in porta suspendisse dui. Parturient cursus ultricies... commodo lectus condimentum odio auctor blandit fringilla. Nisl urna in ornare mi lectus pretium. Sagittis amet curabitur pharetra hendrerit venenatis. Pellentesque sagittis tempor vitae ut adipiscing nibh sit condimentum.

Quisque nisi purus dictum odio massa sit ac consectetur eget. Diam aliquet a libero tellus suspendisse habitant morbi commodo. Vitae sed erat tellus orci facilisi et aliquam consectetur quisque. Blandit ornare facilisi sagittis velit id. Adipiscing sapien elit tellus accumsan arcu mi. Eget vitae dictum sagittis tempor vitae odio non risus. Adipiscing ornare quis odio bibendum sapien sed vel morbi massa. Mauris sem odio arcu sollicitudin. Vitae hendrerit dui id cras diam ut vitae rhoncus consectetur.

First Step: Enter details

Lorem ipsum dolor sit amet consectetur. Magna vestibulum urna in tellus in porta suspendisse dui. Parturient cursus ultricies commodo lectus condimentum odio auctor blandit fringilla. Nisl urna in ornare mi lectus pretium. Sagittis amet curabitur pharetra hendrerit venenatis. Pellentesque sagittis tempor vitae ut adipiscing nibh sit condimentum.

Quisque nisi purus dictum odio massa sit ac consectetur eget. Diam aliquet a libero tellus suspendisse habitant morbi commodo. Vitae sed erat tellus orci facilisi et aliquam consectetur quisque. Blandit ornare facilisi sagittis velit id. Adipiscing sapien elit tellus accumsan arcu mi. Eget vitae dictum sagittis tempor vitae odio non risus. Adipiscing ornare quis odio bibendum sapien sed vel morbi massa. Mauris sem odio arcu sollicitudin. Vitae hendrerit dui id cras diam ut vitae rhoncus consectetur.

Lorem ipsum dolor sit amet consectetur. Magna vestibulum urna in tellus in porta suspendisse dui. Parturient cursus ultricies... commodo lectus condimentum odio auctor blandit fringilla. Nisl urna in ornare mi lectus pretium. Sagittis amet curabitur pharetra hendrerit venenatis. Pellentesque sagittis tempor vitae ut adipiscing nibh sit condimentum.

Quisque nisi purus dictum odio massa sit ac consectetur eget. Diam aliquet a libero tellus suspendisse habitant morbi commodo. Vitae sed erat tellus orci facilisi et aliquam consectetur quisque. Blandit ornare facilisi sagittis velit id. Adipiscing sapien elit tellus accumsan arcu mi. Eget vitae dictum sagittis tempor vitae odio non risus. Adipiscing ornare quis odio bibendum sapien sed vel morbi massa. Mauris sem odio arcu sollicitudin. Vitae hendrerit dui id cras diam ut vitae rhoncus consectetur.

Discover your savings goal

Just one more step to go!

Lorem ipsum dolor sit amet consectetur. Magna vestibulum urna in tellus in porta suspendisse dui. Parturient cursus ultricies commodo lectus condimentum odio auctor blandit fringilla. Nisl urna in ornare mi lectus pretium. Sagittis amet curabitur pharetra hendrerit venenatis. Pellentesque sagittis tempor vitae ut adipiscing nibh sit condimentum.

Quisque nisi purus dictum odio massa sit ac consectetur eget. Diam aliquet a libero tellus suspendisse habitant morbi commodo. Vitae sed erat tellus orci facilisi et aliquam consectetur quisque. Blandit ornare facilisi sagittis velit id. Adipiscing sapien elit tellus accumsan arcu mi. Eget vitae dictum sagittis tempor vitae odio non risus. Adipiscing ornare quis odio bibendum sapien sed vel morbi massa. Mauris sem odio arcu sollicitudin. Vitae hendrerit dui id cras diam ut vitae rhoncus consectetur.

Lorem ipsum dolor sit amet consectetur. Magna vestibulum urna in tellus in porta suspendisse dui. Parturient cursus ultricies... commodo lectus condimentum odio auctor blandit fringilla. Nisl urna in ornare mi lectus pretium. Sagittis amet curabitur pharetra hendrerit venenatis. Pellentesque sagittis tempor vitae ut adipiscing nibh sit condimentum.

Quisque nisi purus dictum odio massa sit ac consectetur eget. Diam aliquet a libero tellus suspendisse habitant morbi commodo. Vitae sed erat tellus orci facilisi et aliquam consectetur quisque. Blandit ornare facilisi sagittis velit id. Adipiscing sapien elit tellus accumsan arcu mi. Eget vitae dictum sagittis tempor vitae odio non risus. Adipiscing ornare quis odio bibendum sapien sed vel morbi massa. Mauris sem odio arcu sollicitudin. Vitae hendrerit dui id cras diam ut vitae rhoncus consectetur.

Restart

Here it is!

Cost of wedding after 16 years

Amount to be saved monthly to meet the cost of your child's wedding

During your lifetime, you have multiple responsibilities, which include excelling in your profession, taking care of your family, creating a financial plan for your loved ones and yourself and much more. Unfortunately, being caught up in the moment, most of us may simply miss out on securing our future.

However, in the future, this act of not having your future planned out may not be a wise move. Fortunately, when you are close to approaching retirement, you can easily get term insurance for senior citizens, which can help secure your post-retirement insurance needs. So, let’s look into what term insurance plans for senior citizens can do for you.

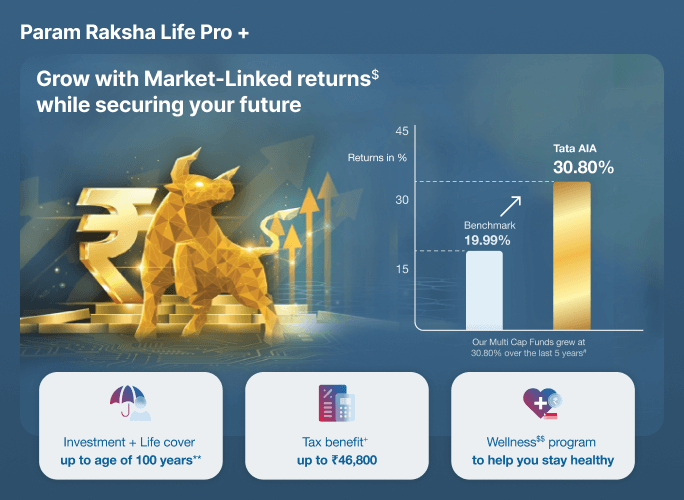

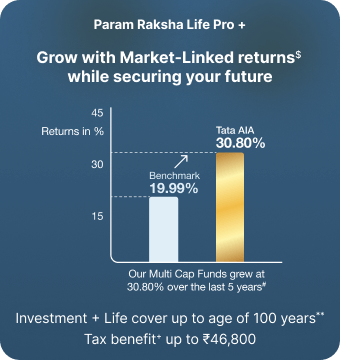

| Last 5 Years #Returns | Since Inception ''Returns | |||

| Tata AIA Funds | Fund Return (%) |

Benchmark Return (%) |

Fund Return (%) |

Benchmark Return (%) |

| Multi Cap Fund | 30.80% | 19.99% | 23.49% | 14.87% |

| India Consumption Fund | 30.15% | 19.99% | 22.80% | 14.87% |

| Top 200 Fund | 30.15% | 19.99% | 20.25% | 16.42% |

#Data as on Sep 30th,2024. Past performance is not indicative of future performance.

Fund Benchmark: Multi Cap Fund- S&P BSE 200; India Consumption Fund- S&P BSE 200; Top 200 Fund- S&P BSE 200; SFIN: Multi Cap Fund- ULIF 06015/07/14 MCF 110; Top 200 Fund- ULIF 02712/01/09 ITT 110; India Consumption Fund- ULIF 06115/07/14 ICF 110.

Other funds are also available under this solution

Wealth-Plan-Market-Linked-Return-Calculator

This advertisement is combination of products namely, Tata AIA Smart Sampoorna Raksha Supreme (UIN: 110L179V01) and Tata AIA Vitality Protect Advance (UIN: 110N178V01)

In this policy, the investment risk in investment portfolio is borne by the policyholder.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

TATA AIA Life Insurance

Wealth-Plan-Policy-Market-Linked-Return-Calculator

This advertisement is combination of products namely, Tata AIA Smart Sampoorna Raksha Supreme (UIN: 110L179V01) and Tata AIA Vitality Protect Advance (UIN: 110N178V01)

In this policy, the investment risk in investment portfolio is borne by the policyholder.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

TATA AIA Life Insurance

| Last 5 Years #Returns | Since Inception ''Returns | |||

| Tata AIA Funds | Fund Return (%) |

Benchmark Return (%) |

Fund Return (%) |

Benchmark Return (%) |

| Multi Cap Fund | 30.80% | 19.99% | 23.49% | 14.87% |

| India Consumption Fund | 30.15% | 19.99% | 22.80% | 14.87% |

| Top 200 Fund | 30.15% | 19.99% | 20.25% | 16.42% |

#Data as on Sep 30th,2024. Past performance is not indicative of future performance.

Fund Benchmark: Multi Cap Fund- S&P BSE 200; India Consumption Fund- S&P BSE 200; Top 200 Fund- S&P BSE 200; SFIN: Multi Cap Fund- ULIF 06015/07/14 MCF 110; Top 200 Fund- ULIF 02712/01/09 ITT 110; India Consumption Fund- ULIF 06115/07/14 ICF 110.

Other funds are also available under this solution

In this policy, the investment risk in investment portfolio is borne by the policyholder.

In this policy, the investment risk in investment portfolio is borne by the policyholder.

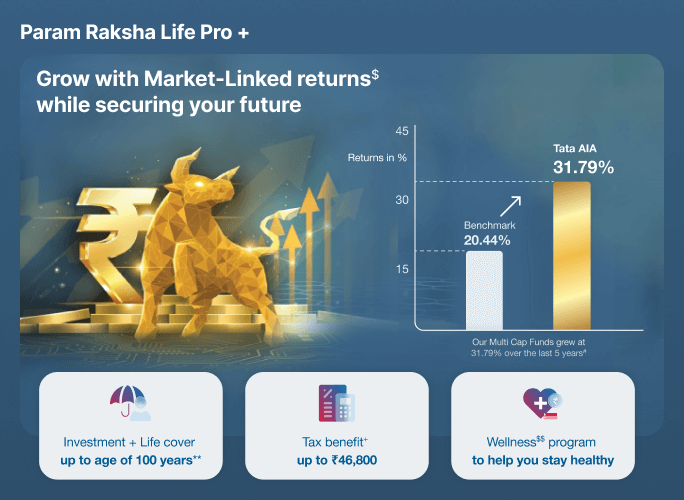

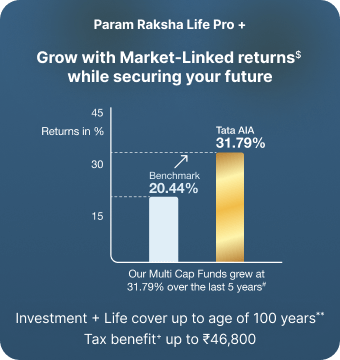

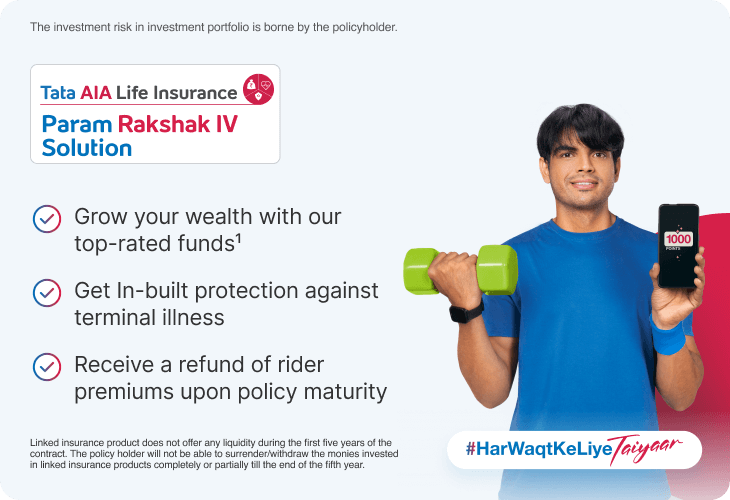

Param Rakshak IV

Experience the dual benefit of life insurance with market-linked~ wealth growth,

accompanied by access to the Tata AIA Vitality wellness program for a holistic

well-being experience.

Param Rakshak IV

Experience the dual benefit of life insurance with market-linked~ wealth growth, accompanied by access to the Tata AIA Vitality wellness program for a holistic well-being experience.

Grow your wealth with our top-rated funds1

Get In-built protection against terminal illness

Receive a refund of rider premiums upon policy maturity

For security of your policy details, please enter OTP sent to your registered mobile no. <b>8956******</b> and registered email Id <b>ra****</b>

03:00

Please enter valid OTP

Please check you credentials, as details entered does not match to our record

You have crossed 3 attempts for OTP authentication

Your request could not be completed please try after sometime.

Share your details for availing Personal Medical Case Management (PMCM)

Service

TATA AIA Life Insurance Co. Ltd will send you updates on your policy, new products and services, insurance solutions or related information.

Tata AIA Life Insurance Smart Annuity Plan

Additional coverage that can be added to your insurance policy

A Non-linked, Non-participating, Individual Health Rider (UIN: 110A048V04)

Tata AIA

Get financial protection against death, accidental death/disability

Tata AIA

Extended protection to your loved ones too under the same plan.

Return of balance premium$

Tax benefits* as per applicable laws.

Additional coverage that can be added to your insurance policy

A Non-linked, Non-participating, Individual Health Rider (UIN: 110A048V04)

Tata AIA

Get financial protection against death, accidental death/disability

Tata AIA

Extended protection to your loved ones too under the same plan.

Return of balance premium$

Tax benefits* as per applicable laws.

ULIPs provide life insurance coverage along with investment benefits. In the event of the policyholder's untimely demise, the nominee receives the sum assured or the fund value, whichever is higher.

ULIPs offer the flexibility of choosing between different funds based on the policyholder's risk appetite and share market investment goals. The policyholder can switch between different funds as per their financial goals and market conditions.

ULIPs offer the potential for higher returns compared to traditional life insurance policies. As ULIPs invest in equity, debt or balanced funds, the returns are linked to the market performance.

ULIPs offer tax benefits* under Section 80C of the Income Tax Act, which allows the policyholder to claim a deduction of up to Rs. 1.5 Lakh from their taxable income.

ULIPs can help in wealth creation over the long term by providing market-linked returns$.

ULIPs allow Liquidity after a specified lock-in period, which helps in meeting short-term financial needs.

ULIPs provide life insurance coverage along with investment benefits. In the event of the policyholder's untimely demise, the nominee receives the sum assured or the fund value, whichever is higher.

ULIPs offer the flexibility of choosing between different funds based on the policyholder's risk appetite and share market investment goals. The policyholder can switch between different funds as per their financial goals and market conditions.

ULIPs offer the potential for higher returns compared to traditional life insurance policies. As ULIPs invest in equity, debt or balanced funds, the returns are linked to the market performance.

ULIPs offer tax benefits* under Section 80C of the Income Tax Act, which allows the policyholder to claim a deduction of up to Rs. 1.5 Lakh from their taxable income.

ULIPs can help in wealth creation over the long term by providing market-linked returns$.

ULIPs allow Liquidity after a specified lock-in period, which helps in meeting short-term financial needs.

Safeguard the financial security of your loved ones with our affordable term insurance plans.

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN:110N176V01)

Tata AIA

Non-Linked, Non-Participating, Pure Risk, Individual Life Insurance Product (UIN: 110N171V03)

Grow your wealth with our guaranteed return plans for a fikar-free future and also save on tax7.

Individual, Non-Linked, Non-participating, Life Insurance Savings Plan

(UIN110N163V07) | 6T&C apply

Tata AIA

Non-Linked, Non-Participating, Individual Life Insurance Savings Plan (UIN: 110N158V12) | 10T&C apply

Tata AIA

A Non-Linked, Non-Participating, Individual Life Insurance Savings Plan)

(UIN: 110N126V05 | 12T&C apply

Tata AIA

Individual, Non-Linked, Non-Participating, Life Insurance Savings Plan (UIN:110N152V13) | 15T&C apply

Discover Complete Health and Wealth: Our comprehensive plan takes care of your health, wellness, and financial security all in one.

In This Policy, The Investment Risk in Investment Portfolio Is Borne by The Policyholder

Param Rakshak Pro solution comprises of Tata AIA Smart Sampoorna Raksha Pro, A Unit-linked, Non-participating, Individual Life Insurance Plan (UIN: 110L172V01) and Tata AIA Vitality Protect Plus, A Non-linked, Non-participating, Individual Health Rider (UIN: 110A048V03). Smart Sampoorna Raksha Pro is also available individually for sale

Tata AIA

Unit Linked Individual Life Insurance Savings Plan

(UIN: 110L112V06)

Tata AIA

Tata AIA Pro-Fit comprises of Tata AIA Smart Health, A Unit-linked, Non-participating, Individual Health Insurance Plan (UIN: 110L168V02), Tata AIA Sampoorna Health, A Non-Linked, Non- Participating Individual Health rider (UIN: 110A167V02) & Tata AIA OPD Care, A Linked, Non-Participating, Individual Health Rider (UIN: 110A166V02). Tata AIA Smart Health is also available individually for sale.

Plan your retirement wisely with a suitable pension plan for peace of mind in your golden years

Tata AIA

A Non-Linked, Non-Participating, Annuity Plan

(UIN:110N161V09) | 25T&C apply

Tata AIA

Individual Non-Linked, Non-Participating, Pension Plan

(UIN: 110N175V02) | 24T&C apply

Age |

Policy Payment Term |

Policy term | Sum Assured | Annual Premium |

Monthly Premium |

Annual Mode Fund Value& @4% |

Annual Mode Fund Value& @8% |

Monthly Mode Fund Value |

40 |

5 |

40 | ₹50,00,000 |

₹1,98,715 |

₹17,002 |

₹6,23,525 |

₹32,78,065 |

₹30,32,753 |

35 |

5 |

40 | ₹1,00,00,000 |

₹2,36,752 |

₹20,160 |

₹8,40,945 |

₹44,91,945 |

₹42,06,628 |

40 |

5 |

40 | ₹1,00,00,000 |

₹3,21,944 |

₹27,341 |

₹12,47,044 |

₹79,75,820 |

₹74,86,255 |

40 |

10 |

40 | ₹50,00,000 |

₹1,14,500 |

₹9,785 |

₹6,23,525 |

₹38,69,889 |

₹36,09,047 |

| 30 | 10 | 40 | ₹1,00,00,000 |

₹1,04,360 | ₹8,887 | ₹8,16,112 | ₹34,32,200 | ₹32,52,766 |

| 35 | 10 | 40 | ₹1,00,00,000 |

₹1,40,221 | ₹11,923 | ₹11,62,042 | ₹52,61,381 | ₹49,48,610 |

| 40 | 10 | 40 | ₹1,00,00,000 |

₹1,87,510 | ₹15,907 | ₹16,53,350 | ₹86,30,695 | ₹81,09,012 |

| 40 | 12 | 40 | ₹50,00,000 |

₹1,00,698 | ₹8,601 | ₹9,18,840 | ₹40,99,561 | ₹38,33,217 |

| 35 | 12 | 40 | ₹1,00,00,000 |

₹1,19,154 | ₹10,133 | ₹11,92,417 | ₹48,79,758 | ₹45,86,501 |

| 40 | 12 | 40 | ₹1,00,00,000 |

₹1,65,771 | ₹14,055 | ₹18,37,664 | ₹89,45,233 | ₹84,12,709 |

Fund allocation in Multi Cap Fund 100%. Give get denotes how much you pay versus how much you receive in return. Give-get of 3 means, you will receive 3 times of what you have paid

&Some benefits are guaranteed and some benefits are variable with returns based on the future performance of your insurer carrying on life insurance business. If your policy offers guaranteed benefits then these will be clearly marked "guaranteed" in the illustration table on this page. If your policy offers variable benefits then the illustrations on this page will show two different rates of assumed future investment returns. These assumed rates of return are not guaranteed and they are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

All Premiums are subject to applicable taxes, cesses & levies which will be entirely borne/ paid by the Policyholder, in addition to the payment of such Premium. Tata AIA Life shall have the right to claim, deduct, adjust, recover the amount of any applicable tax or imposition, levied by any statutory or administrative body, from the benefits payable under the Policy. Kindly refer the sales illustration for the exact premium.

In this policy, the investment risk in investment portfolio is borne by the policyholder.

Unit Linked Individual Life Insurance Savings Plan (UIN:110L112V06)

In this policy, the investment risk in investment portfolio is borne by the policyholder.

Unit Linked Individual Life Insurance Savings Plan (UIN:110L112V06)

Tata AIA

Fortune Pro

Be it insurance or investment, trust the top rated. Invest in a ULIP plan that promises market-linked returns1 from funds rated 4 or 5^ by Morningstar~

Investment growth with market-linked returns1 & loyalty additions~~

Investment growth with market-linked returns1 & loyalty additions~~

27.29% Returns+ for Multi Cap Fund (Benchmark: 15.68%)

27.29% Returns+ for Multi Cap Fund (Benchmark: 15.68%)

Save Income tax# as per applicable tax laws

Save Income tax# as per applicable tax laws

In this policy, the investment risk in investment portfolio is borne by the policyholder.

Unit Linked Individual Life Insurance Savings Plan (UIN:110L112V06)

In this policy, the investment risk in investment portfolio is borne by the policyholder.

Unit Linked Individual Life Insurance Savings Plan (UIN:110L112V06)

Tata AIA

Fortune Pro

Be it insurance or investment, trust the top rated. Invest in a ULIP plan that promises market-linked returns1 from funds rated 4 or 5^ by Morningstar~

Investment growth with market-linked returns1 & loyalty additions~~

Investment growth with market-linked returns1 & loyalty additions~~

27.29% Returns+ for Multi Cap Fund (Benchmark: 15.68%)

27.29% Returns+ for Multi Cap Fund (Benchmark: 15.68%)

Save Income tax# as per applicable tax laws

Save Income tax# as per applicable tax laws

Get Life Insurance cover to safeguard your family

Grow your income by choosing Sub Wallet~ feature and withdraw as and when required

Option to receive income on a ‘Special Date’ of your choice**

Non-Linked, Non-Participating, Individual Life Insurance Savings Plan (UIN: 110N158V12)

Tata AIA

Fortune Guarantee Plus

Non-Linked, Non-Participating, Individual Life Insurance Savings Plan (UIN: 110N158V12)

Tata AIA

Fortune Guarantee Plus

Give your future the financial security it deserves with this fixed income plan

that also provides life cover.

Give your future the financial security it deserves with this fixed income plan that also provides life cover.

Get guaranteed* tax free# income

Long term income for up to 45 years

Pay premium as per convenience in monthly instalments

Param Rakshak Plan Comparison

Benefit |

Tata AIA Param Rakshak |

Tata AIA Param Rakshak Plus |

Tata AIA Param Rakshak II |

Tata AIA Param Rakshak III |

Life Insurance Cover

|

Yes |

Yes |

Yes |

Yes |

Market Linked Returns~

|

Yes |

Yes |

Yes |

Yes |

Accidental Death • Additional Sum Assured in case of Accidental Death. • 2X Additional Sum Assured in case of accidental death in public transport. |

Yes |

Yes |

Yes

|

Yes

|

Accidental Total & Permanent Disability • Benefit payout in case of Total and Permanent disability to accident. • 2X Benefit in case of disability due to accident in public transport |

Yes |

Yes |

Yes |

Yes

|

CritiCare Plus 40 Critical Illness Conditions covered |

No |

Yes |

No |

No |

HospiCare Hospital Cash Benefit • Per day Hospitalization Benefit at 0.5% of Sum Assured • 2X of Per day Hospitalization Benefit for ICU Benefit |

No |

Yes |

No |

No |

Return on Maturity4 at the end of the Policy Term Get the fund value on maturity from the base plan

|

Yes |

Yes |

Yes |

Yes |

| Income Tax Benefits | Yes |

Yes |

Yes |

Yes |

Term Booster5 10% Sum Assured for Terminal Illness |

No |

No |

Yes |

Yes

|

Tata AIA Vitality2 A science-based wellness program that helps you improve your health while also rewarding you. Get up to 10% upfront discount3 on first year rider premium. |

Yes |

Yes |

Yes |

Yes |

Param Rakshak Pro

Param Rakshak Pro solution comprises of Tata AIA Smart Sampoorna Raksha Pro, A Unit-linked, Non-participating, Individual Life Insurance Plan (UIN: 110L172V01) and Tata AIA Vitality Protect Plus, A Non-linked, Non-participating, Individual Health Rider (UIN: 110A048V03). Tata AIA Smart Sampoorna Raksha Pro is also available individually for sale.

Param Rakshak (Return of Premium)

Param Rakshak solution comprises of Tata AIA Life Insurance Smart Sampoorna Raksha - A Unit-linked, Non-participating, Individual Life Plan for Savings and Protection (UIN:110L156V03), Tata AIA Vitality Protect Plus - A Non-linked, Non-participating, Individual Health Rider (UIN: 110A048V03 or any other later version). Tata AIA Life Insurance Smart Sampoorna Raksha is also available individually for sale.

Param Rakshak Plus

Param Rakshak Plus solution comprises of Tata AIA Life Insurance Smart Sampoorna Raksha, A Unit-linked, Non-participating, Individual Life Insurance Plan for Savings and Protection (UIN:110L156V03), Tata AIA Vitality Protect Plus, A Non-Linked, Non- Participating Individual Health rider (UIN: 110A048V03) and Tata AIA Vitality Health Plus, A Non-linked, Non-participating, Individual Health Rider (UIN: 110A047V02). Tata AIA Life Insurance Smart Sampoorna Raksha is also available individually for sale.

Param Rakshak II

Param Rakshak II solution comprises of Tata AIA Life Insurance Smart Sampoorna Raksha, A Unit-linked, Non-participating, Individual Life Insurance Plan for Savings and Protection (UIN:110L156V03), Tata AIA Vitality Protect Plus, Non-participating, Individual Health Rider (UIN: 110A048V03) Tata AIA Life Insurance Smart Sampoorna Raksha is also available individually for sale.

Param Rakshak IV

Param Rakshak IV solution comprises of Tata AIA Life Insurance Smart Sampoorna Raksha, A Unit-linked, Non-participating, Individual Life Insurance Plan for Savings and Protection (UIN: 110L156V03) and Tata AIA Vitality Protect Plus, A Non-linked, Non-participating, Individual Health Rider (UIN: 110A048V03). Tata AIA Life Insurance Smart Sampoorna Raksha is also available individually for sale.

Param Rakshak Elite

Param Rakshak Elite solution comprises of Tata AIA Smart Sampoorna Raksha Pro, A Unit-linked, Non-participating, Individual Life Insurance Plan (UIN: 110L172V01) and Tata AIA Vitality Protect Plus, A Non-linked, Non-participating, Individual Health Rider (UIN: 110A048V03). Tata AIA Smart Sampoorna Raksha Pro is also available individually for sale.

Param Rakshak Prime

Param Rakshak Prime solution comprises of Tata AIA Smart Sampoorna Raksha Pro, A Unit-linked, Non-participating, Individual Life Insurance Plan (UIN: 110L172V01) and Tata AIA Vitality Protect Plus, A Non-linked, Non-participating, Individual Health Rider (UIN: 110A048V03). Tata AIA Smart Sampoorna Raksha Pro is also available individually for sale.

Param Rakshak II 2.0

Param Rakshak II 2.0 solution comprises of Tata AIA Smart Sampoorna Raksha Pro, A Unit-linked, Non-participating, Individual Life Insurance Plan for Savings and Protection (UIN:110L172V01), Tata AIA Vitality Protect Plus, Non-participating, Individual Health Rider (UIN: 110A048V03) Tata AIA Smart Sampoorna Raksha Pro is also available individually for sale.

Param Rakshak (Return of Premium) 2.0

Param Rakshak ROP 2.0 solution comprises of Tata AIA Smart Sampoorna Raksha Pro - A Unit-linked, Non-participating, Individual Life Plan for (UIN:110L172V01), Tata AIA Vitality Protect Plus - A Non-linked, Non-participating, Individual Health Rider (UIN: 110A048V03). Tata AIA Life Insurance Smart Sampoorna Raksha is also available individually for sale.

L&C/Misc/2021/Dec/0575

Government of India has mandated regulations wherein, if the PAN shared by the customer is established as Invalid, Inoperative, or categorized as Specified Person’s PAN, then TDS is to be deducted at a higher rate.

PAN of individual considered as inoperative if it is not linked with Aadhar. For further details, please refer Link Aadhaar FAQ | Income Tax Department.

PAN Number provided is incorrect.

If an individual’s PAN established as inoperative or invalid, then TDS @20% will be applicable for all due future payouts, where benefits under section 10 (10D) of the Income Tax Act is not available.

Aadhaar-PAN linkage is not necessary for an individual who is:

To link PAN with Aadhar, visit Income tax website and follow the steps provided in Link Aadhaar User Manual.

As per Section 206AB of the Income Tax Act, a person who has not filed income tax return (ITR) for the preceding FY within 139(1) due date and TDS and TCS during last financial year exceeds specified limit.

If an individual is considered as a ‘Specified Person’ then TDS shall be levied at TWICE the applicable TDS rate for policies where benefits under section 10 (10D) of the Income Tax Act is not available.

In order to prevent the deduction of tax at higher rate, the specified person must visit the online portal Home | Income Tax Department and file their tax returns within available timelines.

You can use any of the following channels to inform us:

Tata AIA Life Insurance Company Limited | Claims Department

B- wing, 9th Floor, I-Think Techno (Lodha) Campus,

Behind TCS, Pokhran Road No.2,

Thane(West) - 400 607.

Claim intimation can be done online while claim payout can be made through NEFT

Yes. It can be lodged from any branch of TATA AIA Life Insurance

Click here to locate your nearest TATA AIA Life Insurance Branch

The Nominee has the option to submit the claim online by uploading the signed / self attested copies or submit the documents via email.

Click here to register a claim online.

Alternatively, the nominee can send the documents by courier to his / her representative in India. The representative may visit our branch and intimate us of the claim

Please click on link: https://www.tataaia.com/customer-service/easy-claims.html to know the list of documents needed for claim intimation

Yes, claim would be accepted as Original Policy Contract is not mandatory for submission of Claim. Declaration is to be provided by the claimant on a plain paper regarding the misplacement of the original policy document.

It is our endeavour to settle your claim in an expedited manner. We also offer guarantees subject to the criteria being met

We have the following services that can provide claims payout faster

You may track your claim status by referring to track your claim page or take assistance from our Contact Centre or Branches.

Click here to track your claim.

The nominee in the policy should intimate about the claim.

The death benefit is paid to:

The distribution of the claim settlement amount will be as mentioned in the application form by the life insured. The legal heir can claim for the nominee who has passed away.

For multiple nominees, the documents required will be the same in case of 'death claim' along with KYC & Cancelled cheque of all the nominee(s). Please refer to the documentation section for more details

In the event of the death of the Life Assured and Nominee at the same time, the legal heirs can claim for the claim settlement amount by submitting the below documents.

If Sum Assured <4 Lakh then,

If Sum Assured >4 Lakh then, Succession certificate issued by court would be required.

Claim will be decided on the basis of a legally valid succession certificate.

For cases where nominee is minor, an appointee is appointed by the Life Assured at the time of policy issuance. The appointee can apply for the claim. In absence of an appointee, the minor’s legal guardian can apply for the claim proceeds.

In case of the death of the Nominee(s) during the tenure of the policy, the Life Assured should make a fresh nomination. If that has been missed, claim will be decided on the basis of a legally valid succession certificate

Claim amount can only be paid by direct transfer to Bank Account via NEFT (National Electronic Fund Transfer).

Yes

Yes, both would be paid provided the provisions mentioned in policy contract are satisfied.

Claim amount is payable as per the provisions of the policy contract. You may refer the Policy Schedule (Policy Certificate) for the Death Benefit amount or refer the provisions on the contract for details

In most cases, claim settlement amount includes Basic Sum Assured + Rider Sum assured (if applicable) + Other policy additions (Accrued Bonus / Guaranteed additions, etc.)

Death benefit may differ product to product as specified in the policy contract. Only in case of Keyman insurance TDS is deducted, and all other death claim proceeds paid are tax free, and TDS is not deducted.

If the insured is diagnosed of any ailment post policy issuance, it will not be considered as a non-disclosure. However, it’s good to inform the insurance company incase of any such diagnosis.

In case of claim dispute, the claimant may approach the customer care department. If the response is not satisfactory, the claimant may write to the Regional Ombudsman Office

The IRDAI clearly articulates that a claim must be decided within 30 days from the date of receipt of all claim documents/required clarifications.

Investigation Cases: In case the claim warrants an investigation, Insurance Company is expected to complete the investigation in no later than 90 days from the date of receipt of claim intimation, and the claim shall be decided within 30 days thereafter.

Insufficiency of proof of title: If a claim is ready for payment but cannot be paid due to any reasons of proper identification of the payee, then the Insurer may apply to pay the amount at the Court of competent jurisdiction, or, the amount will earn interest at the prevalent rate as applicable.

If the date of death is after the grace period of the said policy, the policy is considered to be lapsed as on the date of death.

If policy is lapsed as on the date of death, no claim will be payable. In case of ULIP products, fund value is payable as per policy terms on the receipt of proof of loss. In traditional products, no amount is payable.

Non-disclosure refers to the situation where a customer fails to reveal a relevant fact when applying for or renewing an insurance contract. These facts are important to the Company for assessing the risk. At the claims stage if it is detected / found that the statements made at the time of application / reinstatement of the policy were false, or Life Assured had acted against the interest of the Company, the Company has the right not to pay the claim amount.

You can do it either through Cashless Process or through non-Cashless method.

For normal processing of Health / Living Claim, once the patient suffers from any illness / undergoes a surgery / is hospitalized and is under treatment, claim can be made to the company with all the details of hospitalization. Once the patient is discharged all the medical papers including Discharge Summary, all diagnostic test reports and treatment papers need to be submitted to the company along with the list of requirements specified as per Claim type.

Currently Cashless Hospitalization is available under Tata AIA Life Insurance Invest Assure Health, Tata AIA Life Insurance Health First and Tata AIA Life Insurance Hospi CashBack, Invest Assure Health Plus and Invest Assure Health Supreme.

You can call up Raksha TPA on the toll free numbers given on the health card.

Special Assistance number:18001801555

The duly filled & signed pre-authorization form along with photo ID proof & cashless card needs to be faxed from hospital to TPA. Cashless amount will be approved by TPA to the hospital basis the policy provisions.

Details of Raksha TPA:

Special Assistance number: 18001801555

E-mail : crcm@rakshatpa.com

Cashless facility will be provided as per policy terms & conditions. The difference between the approved Cashless claim amount & balance bill amount will need to be borne by the Customer.

Yes, you can change your premium payment frequency mode on all active policies as per your convenience. Premium payment frequency change will only take effect from policy anniversary date and can be changed 15 days prior to the policy anniversary date.

You have 4 premium payment frequency options – Yearly (once a year), Half Yearly ( twice a year ), Quarterly ( 4 times a year ) or Monthly ( 12 installments in a year )

The recommended premium payment frequency is annual premium payments. This will ensure that your policy is renewed every year hassle free. You also pay lesser premiums as well obtain continuous policy benefits.

You can change the name in your policy by sending an Email to us mentioning the changes along with the self-attested copies of the required documents.

Click here to send a request via email.

Alternatively, you can also log in to your Online Policy Account and make the required changes.

Click here to login to your Online Policy A/C

Proof for correction in name can be Birth Certificate, Passport, Pan Card, etc. Poof for change in name can be a Marriage Certificate or a Notarized affidavit or the copy of the newspaper advertisement if applicable.

Free Look is similar to the return policy that we can avail when we buy goods and are not satisfied with them. Every insurance policy offers a "Freelook" period of 15 days from the date of delivery of the policy documents. The Freelook period is of 30 days for policies sourced through Electronic / Distance mode. Where customers have opted for Electronic Insurance Account at the time of purchase, the freelook period is from the date of credit to the EIA account.

If the insured wishes to use this facility and return the policy within the free look period, he/she is entitled to a return of premium with the following deductions wherever applicable-

For every policy the provision to change the policy term is different. We request you to kindly go through the Terms & Conditions for your particular policy in your Policy Document to get the required details.

It is advisable to stay invested with your policy for the entire term. Longer the term of the policy, better it is for you in terms of coverage.

You can avail the facility of changing the ownership of the policy in case of current owner’s death or change in marital status. You can change the owner of your policy by raising a service request from our website and uploading the self-attested copies of the required documents.

Click here to raise a Service Request.

Taking a loan against your policy is really easy. Generally according to the eligibility criteria, you would be eligible to take loan of up to 60 to 80% of the Surrender Value as on the date of loan application.

To apply for a loan you have to raise a service request from our website and upload the self-attested copies of the required documents.

Click here to raise a Service Request.

Nomination is an authorization to someone to receive the policy money (sum assured) if/when the Life Insured dies. The Life Insured can nominate any person (usually a close relative) to receive the money from the insurance company if they pass away before the policy matures.

You can add/change the nomination at any time before the maturity of the policy.

To do so, you can login to your Online Policy Account and make the necessary changes.

Click here to login to your Online Policy A/C

Alternatively, you can directly raise a service request from our website and upload the self-attested copies of the required documents.

Click here to raise a Service Request.

A nominee is appointed by the policyholder, and can be anyone to whom the policyholder wants the financial benefits to accrue, in case of his/her death during policy tenure.

General practice is to appoint spouse, child or a parent as the nominee.

Under nomination, the nominee gets only the right to receive the policy money in the event of the death of the policyholder.

If the nominee dies after the death of the policyholder but before receiving the policy money, then nomination becomes ineffective and only the legal heirs of the policy owner can claim the money.

Assignment of an insurance policy is the transfer or assignment of all rights and liabilities to the insurance policy in favour of the assignee, and cannot be revoked. However, the policy can be re-assigned in favour of the insured at the written request of the assignee.

There are two types of assignments for an insurance policy.

Absolute Assignment – Under this process, the complete transfer of rights from the Assignor to the Assignee will happen. There are no conditions applicable.

Conditional Assignment – Under this type of assignment, the transfer of rights will happen from the Assignor to the Assignee subject to certain conditions. If the conditions are fulfilled, only then will the Policy will get transferred from the Assignor to the Assignee.

You can assign your policy to take a loan against it, as a security, or to gift it to someone.

You can easily do this by directly raising a service request from our website and uploading the self-attested copies of the required documents.

Click here to raise a Service Request.

Alternatively, you can also send an email to us mentioning all the required changes.

Click here to raise the request via email.

Downloading Policy Document is now easier than ever. You can do so directly from our website. Click here, enter your policy number, authenticate, and download it right away.

If you need the hard copy of the Policy document, you can raise a service request on our website for a duplicate policy document, and pay the printing fees of Rs. 250 + GST.

Click here to raise a Service Request.

The payment to the policyholder at the end of the stipulated term of the policy is called maturity amount.

If the due premiums are not paid while the policy is still within the lock-in period, then the policy would lapse and all benefits of the policy would cease.

The policy holder has a grace period for premium payment, which is 15 days from the due date for monthly premium payment frequency and 30 days from the due date for half-yearly and yearly premium payment frequency.

It is advisable to make the premium payment on time to continue having all the benefits that your policy provides you.

Click here to pay your premium.

An insurance grace period is a defined amount of time after the premium is due during which a policyholder can make a premium payment without coverage lapsing.

It is 15 days from the due date for monthly premium payment frequency, and 30 days from the due date for half-yearly and yearly premium payment frequencies.

If the due premiums are not paid while the policy is still within the lock-in period, then the policy would lapse and all benefits of the policy would cease.

The policy holder has a grace period for premium payment, which is 15 days from the due date for monthly premium payment frequency, and 30 days from the due date for half-yearly and yearly premium payment frequencies.

If the due premiums are not paid even after completion of 45 days of the grace period, then the policy acquires a "discontinued" status, at which time the policy benefits cease.

Once all outstanding premiums are paid and a Health Certificate (if required) is submitted within a period of 2/5 years from the last unpaid premium due date(as per policy contract), a policy gets revived, and the life cover restarts from the date of revival.

Policy holders can apply for the revival of the policy within two years from the date of policy discontinuance, by paying the due premium, reinstatement charges and submitting the Personal Health Declaration form (if applicable). The revival of policy is subject to underwriting.

Policy holder can reinstate his/her policy within the timeframe specified in the policy contract, which differs from product to product.

An automatic premium loan(APL) is an insurance policy provision that allows the insurer to deduct the amount of an outstanding premium from the Surrender Cash Value of the policy as on the date when the premium is due.

As per the product feature, a policy may use the APL facility and be in active state even after the non payment of premium in the grace period. The policy will be active until lapsation. However, interest will be charged on a daily basis on the premium amount, and the customer will have to pay the total amout of premium plus the daily interest charged as on the date of payment to get the policy out of APL state.

For immediate annuity option, pension income will start immediately as per the payment mode chosen. For deferred annuity, pension income will start post deferment period.

You have to submit the existence certificate attested by the authorities mentioned on the existence certificate, along with ID and address proof after every 3 years, if return of purchase price option is chosen, and every year if Immediate Life annuity is chosen.

Below are the different pension options available under Smart Annuity plan to meet your future needs.

Immediate Life Annuity - The annuity shall be payable in arrears as per payment mode chosen by you, for as long as the Annuitant is alive.

On death of the Annuitant, the annuity payments will

Immediate Life Annuity with Return of Purchase Price - The annuity shall be payable as per the payment mode chosen by you, as long as annuitant is alive. On death of annuitant, purchase price is payable.

as lump sum to nominee and no further payout will be payable.

Deferred Life Annuity with Return of Purchase Price - Deferment Period between 1 to 10 years as chosen by you at inception. The annuity shall be payable post deferment period as per payment mode chosen by you as long as annuitant is alive. On death of annuitant, purchase price is payable as lump sum to nominee and no further payout will be payable

You have to submit the existence certificate attested by the authorities mentioned on the existence certificate, along with ID and address proof after every 3 years, if return of purchase price option is chosen, and every year if Immediate Life annuity is chosen.

An Existence Verification check is applicable for customers who are receiving pension income from any of their pension policies with us. Once you start receiving pension income, we do a verification check every year*. This is known as the Existence Verification check. This check can be done online with a few clicks, as well as through any of our offline mediums mentioned. We will send you a detailed communication on the process closer to the time when you are required to complete it. This process is important to ensure that there is no interruption in the pension income that you receive.

Every year- If you have opted for pension option without return of purchase price.

Once in three years- If you have opted for pension option with return of purchase price.

You can now easily do existence verification by either calling our Customer Care, or by writing a mail to request an existence verification check via video call as well. You will just need a smartphone and a valid address proof for this.

Renewal premiums are the subsequent premiums that are paid by the policyholder to the insurer in order to keep the policy in operation and avail the benefits of the policy accordingly.

There are various convenient options to make the premium payments

You can get more information about the Premium Payment options by watching the video. Click here

Enrolling for Standing Instruction facility is a simple process. In this process, premium will be transferred from your credit card/bank account on due date.

To enroll- Visit www.tataaia.com; go to ‘Customer Service’ menu and select ' Set Standing Instruction'

Kindly ensure you register 7 days before the due date to ensure your standing instruction is ready for execution on the due date.

If you have opted for the Standing Instruction facility, the instruction is sent to your Bank 7 days in advance and the premium will be debited on due date.

Yes. Premium can be paid through various premium payment option during the pendency of the mandate. Click here to pay right away

Banks charge a one time fees for the mandate / standing instruction registration. The fee varies from bank to bank. Post registration, no extra amount is charged for execution of the Standing Instruction premium payment

After the premium is paid, you receive an instant 'premium acknowledgement statement' on the registered email id. This can also be used as an investment proof / tax filing purposes.

The premium is applied to your policy on the due date as per Insurance law. Once that is done, you will get the 'Premium Receipt' on your registered Email ID. You can also get it from 'download statements' or login to your 'Online Policy A/C' and download the Premium receipt.

Click here to login to your Online Policy A/C.

Alternatively, you can also download it from our WhatsApp services.

Click here to opt in for our WhatsApp services.

Premium status gets updated real-time normally. We request you to wait for 24-48 hours and recheck the status.

Any extra premium paid will be refunded to your bank account registered with us, by default. In case if the next renewal premium due is in the same financial year, it may be adjusted towards next premium. However you can always raise a Service Request in case you wish to receive the amount back.. Click here to raise a service request directly from our website.

Yes. It can be paid in foreign currency if your residential status is NRI/PIO/OCI, and country of residence is other than India

As per GST Act, if the consumer shows the evidence of paying premium via NRE account, his/her residence status is NRI/PIO/OCI, and country of residence is other than India, then such customers will be eligible for GST waiver.

To avail the same, customers will need to make premium payment by cheque (NRE Account), or transfer using SWIFT facility in foreign currency. Additionally, we request

To avail the GST waiver facility, you can send an email to us mentioning all the details. Click here to raise a request via email.

The Tax Certificate is a document that displays the total premium that you have paid for all your policies in a specific financial year. You can use this document as an investment proof for tax filing.

Yes. You will get a reminder via SMS on your mobile number and email ID registered in policy records.

Yes. We allow one year premium in advance, subject to premium due in current financial year.

Late payment fees will be levied if that is the case, along with the interest prevailing from time to time, which will be calculated from the due date till actual payment date.

Premium received for ULIP on Saturday/Sunday/after 3 PM, Unit allocation will be done basis the NAV Pricing declared on next working day.

In case the Standing Instruction is active, it is advisable to pay premium 7 days in advance to avoid double payment.

Cancer Care

Major Critical Illness (8/20/42 CI’s)

Comprehensive Critical Illness (8/20/42 CI’s + 15 Minor CI’s)

Accidental Death Benefit

Accidental Total and Permanent Disability

All cause Total and Permanent Disability

Accidental Partial and Permanent Disability

Accidental Dismemberment Benefit

Hospital Cash Benefit

Surgical Cash Benefit

Waiver of EMI on Hospitalization

Terminal Illness

Waiver of Premium on Major Surgery

Waiver of Premium on Major Critical Illness

Waiver of Premium on Accidental Total and Permanent Disability

Cancer Care

Major Critical Illness (8/20/42 CI’s)

Comprehensive Critical Illness (8/20/42 CI’s + 15 Minor CI’s)

Accidental Death Benefit

Accidental Total and Permanent Disability

All cause Total and Permanent Disability

Accidental Partial and Permanent Disability

Accidental Dismemberment Benefit

Hospital Cash Benefit

Surgical Cash Benefit

Waiver of EMI on Hospitalization

Terminal Illness

Waiver of Premium on Major Surgery

Waiver of Premium on Major Critical Illness

Waiver of Premium on Accidental Total and Permanent Disability

|

|

|

*Pre-existing diseases are only covered after their waiting period has been completed.

Features |

Details |

Claims |

Cashless Claims Reimbursement Claims |

Coverage |

|

Fixed Benefit Payout including pre and post hospitalisation, |

Covered |

Day Care Procedures |

Covered |

OPD Cover |

Available |

ICU Charges |

Covered |

Free Health Check-ups |

Available |

Pre-existing Diseases |

Covered* |

Ambulance Cover |

Available |

Critical Illness Cover |

Available |

Benefits |

|

Tax Benefits5 |

Up to ₹1,00,000 per financial year under Section 80D |

*Pre-existing diseases are only covered after their waiting period has been completed.

InstaProtect Solution comprises of Tata AIA Life Insurance Sampoorna Raksha Supreme (Non Linked, Non Participating, Individual Life Insurance Plan) (UIN: 110N160V03), Tata AIA Vitality Protect (UIN: 110B046V01) - A Non-linked, Non-participating, Individual Health Rider; Tata AIA Vitality Health (UIN: 110B045V01) - A Non-linked, Non-participating, Individual Health Rider.

In this policy, the investment risk in investment portfolio is borne by the policyholder.

In this policy, the investment risk in investment portfolio is borne by the policyholder.

Days

Premium calculator

Disclaimers

You can include the below mentioned riders to increase your plan coverage

A Non-Linked, Non- Participating Individual Health rider (UIN:110B045V02)

Tata AIA

39 Critical Illness covered including minor stage illnessPays fixed amount on Hospitalization and on ICU admissionEnroll in Tata AIA Vitality^^ to get discount~~ on your first-year rider premium

39 Critical Illness covered including minor stage illnessPays fixed amount on Hospitalization and on ICU admissionEnroll in Tata AIA Vitality^^ to get discount~~ on your first-year rider premiumA Non-Linked, Non- Participating Individual Health rider (UIN:110B046V02)

Tata AIA

Offers protection against 40 Critical Illness including Cancer and Cardiac conditions.Extend protection to your loved ones too under the same plan.Get income tax~ benefits as per applicable tax lawsThese plans offer additional features like health check-ups and discounts on premiums for maintaining a healthy lifestyle during the policy term.

Combines term life coverage with health-related features such as critical illness coverage or hospitalization benefits to provide a more comprehensive protection plan.

Disclaimer

please provide correct credentials

Tata AIA लाइफ़ इंश्योरेंस संपूर्ण रक्षा सुप्रीम

Tata AIA लाइफ़ इंश्योरेंस

संपूर्ण रक्षा सुप्रीम

Stay up-to-date with the latest news and insights from our company by following us. Join our Twitter community today and be a part of the conversation. Click the "Follow" button to get started!

4T&C apply

This advertisement is combination of products namely, Tata AIA Smart Sampoorna Raksha Supreme (UIN: 110L179V01) and Tata AIA Vitality Protect Advance (UIN: 110N178V01)

In this policy, the investment risk in investment portfolio is borne by the policyholder.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

TATA AIA Life Insurance

Premium calculator

Individual, Non-Linked, Non-Participating, Life Insurance Savings Plan (UIN:110N152V11)

Tata AIA

*T&C apply

Term Insurance Calculator

Term Insurance Calculator

7% Digital Discount on first year premium

Increase life cover at key milestones

Save tax up to ₹46,800+

Get your Free Quote For 1 Crore Term Plan

Get your Free Quote For 1 Crore Term Plan

Tata AIA Vitality@ is a globally recognised, holistic and science-based wellness program that helps you understand and improve your health while also rewarding you. The rewards may be in the form of Discount on Premium, Cover Booster etc.

On enrolling into the Wellness Program, you can get an upfront discount## of 10% on Tata AIA Vitality Protect Advance premiums in the 1st year. The premium discount in the subsequent years may increase or decrease based on your Wellness status.

Need assistance in choosing the right insurance plan? Speak to our expert

Our experts are happy to help you!

Thank you for sharing your details.

Our representative will contact you soon.

.svg)