Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

A 10-year ULIP integrates insurance with investment opportunities for your financial growth. This helps in building wealth for long-term goals and ... Read more financially secures your family's financial future. These plans offer a flexible fund option, such as equity, debt, and balanced funds, based on your risk appetite. Staying invested for ten years may help you capitalize on compounding and managing market volatility. ULIPs provide tax2 benefits and the dual advantage of protection-cum-wealth creation together. This article explains everything you need to know about ULIP returns in 10 years. Read less

A 10-year ULIP integrates insurance with investment opportunities for your financial growth... Read more This helps in building wealth for long-term goals and financially secures your family's financial future. These plans offer a flexible fund option, such as equity, debt, and balanced funds, based on your risk appetite. Staying invested for ten years may help you capitalize on compounding and managing market volatility. ULIPs provide tax2 benefits and the dual advantage of protection-cum-wealth creation together. This article explains everything you need to know about ULIP returns in 10 years. Read less

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Premier SIP Calculator

Pay (Total)

₹11,99,016

Get Maturity Benefit

Based on assumed rate of return

₹34.57 Lakh

As per actual past performance

₹70.50 Lakh

@20.37%Additional Benefits

Life Cover (including Terminal Illness Cover): ₹21.7 Lakh

Accidental Death Cover: ₹10.9 Lakh

Accidental Total & Permanent Disability: ₹10.9 Lakh

Discounts

1% discount on 1st year premium for all payments paid through any permissible electronic mode debited through an auto-debit mandate. Maximum discount capping: ₹100 over the year.

Applicable if the policy is purchased digitally.

This discount is auto-applied and can't be removed

Buy Now

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP - Non-participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V01) and

Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually. Product option: Future Secure

A 10-year ULIP offers life coverage and investment benefits. You can invest your premiums in various market-linked5 funds like equity, debt, or hybrid options. The plan helps you accumulate a significant corpus to achieve your important long-term financial goals. Your family receives financial security through life coverage if unforeseen circumstances occur during the policy tenure. Additionally, you can select the sum assured based on your Human Life Value (HLV) and your family's needs. The policy allows fund switches to adjust your investment strategy according to changing market conditions. Market performance determines the growth of your investment and the potential returns over the period of ten years.

Let’s understand how a 10-year ULIP plan works with the help of an example.

Consider Rajesh, a 35-year-old IT professional who wants to fund his daughter's overseas education goals. He calculates that he needs approximately ₹50 Lakh in ten years for her studies abroad.

Rajesh invests ₹2 Lakh annually in a 10-year ULIP to build this education fund systematically. He allocates 70% to equity funds for growth potential and 30% to debt funds for stability. Using a ULIP calculator, Rajesh estimates his fund value will reach his target through consistent investments. He pays annual premiums and claims tax2 deductions under Section 80C of the Income Tax Act. By the time his daughter completes school, Rajesh's ULIP has grown to support her educational dreams. Additionally, the life cover helps ensure his daughter's education is funded even in the case of his untimely demise.

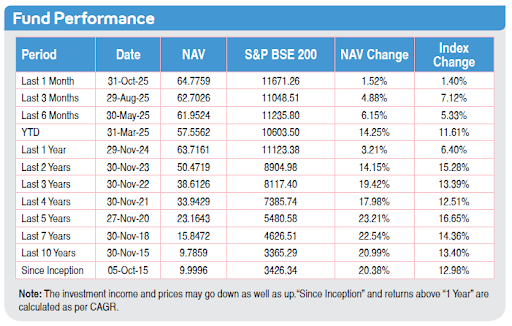

Returns as on

Here is why you should choose a 10-year ULIP policy:

The policy provides life insurance coverage to protect your family's financial future against unexpected events. Your loved ones receive the sum assured amount if you die during the policy term.

ULIPs invest in equities and debt instruments, which have the potential to yield higher returns than conventional savings. A market-linked5 investment helps your funds grow fast with the long investment tenure of ten years.

You can select an investment option and switch funds depending on your goal and market trends. This allows you to revise your strategy to enhance returns and manage risks throughout the tenure.

The premium you pay is eligible for tax2 deduction under Section 80C of the Income Tax Act 1961. Additionally, the maturity proceeds are exempted under Section 10(10D) if all the conditions are met. For all the ULIP plans, irrespective of the premium amount or policy terms, the death benefit is exempt.

Long investment periods deliver potential returns due to the compounding effect and market cycle averaging throughout the tenure. A 10-year ULIP provides sufficient time to build a substantial corpus for important life goals.

Amounts are based on a 20-year-old non-smoker male, with a 20-year premium payment term and a 30-year policy term, Tata AIA Premier SIP Future Secure plan option with 100% invested in Tata AIA Multi Cap Fund at 8% Rate of Return. Returns at 4% for investment of ₹5000/month, ₹10,000/month, ₹15,000/month and ₹20,000/month are 24 Lakh, 49 Lakh, 73 Lakh and 98 Lakh respectively.

The following are important factors that affect ULIP’s performance over ten years:

Let us examine three scenarios based on an ₹80,000 annual investment in different fund types systematically.

Equity fund returns

Annual Investment: ₹80,000

Expected Annual Return Rate: 12%

Investment Period: 10 years

Using the future value formula

FV = P × [(1+r)ⁿ - 1] / r

Future Value = 80,000 × [(1+0.12)¹⁰ - 1] / 0.12

Projected Corpus: ₹14,03,899

Debt fund returns

Annual Investment: ₹80,000

Expected Annual Return Rate: 7%

Investment Period: 10 years

Using the future value formula

FV = P × [(1+r)ⁿ - 1] / r

Future Value = 80,000 × [(1+0.07)¹⁰ - 1] / 0.07

Projected Corpus: ₹11,05,316

Balanced Fund Returns

Annual Investment: ₹80,000

Expected Annual Return Rate: 9%

Investment Period: 10 years

Using the future value formula

FV = P × [(1+r)ⁿ - 1] / r

Future Value = 80,000 × [(1+0.09)¹⁰ - 1] / 0.09

Projected Corpus: ₹12,15,434

These projections may help you understand how different fund choices significantly impact your returns after ten investment years.

Here is how 10-year ULIP policy return rates are calculated:

Your premium amount gets allocated to chosen fund units after deducting applicable policy charges and fees. You can select equity funds, debt funds, or a mix of both based on risk appetite. Fund switching is allowed during the policy term to adjust allocation according to market performance changes.

Net Asset Value is the price of one unit of a particular fund at any given time. The NAV varies each day with market performance and is determined by applying the following standard formula:

NAV = (Market Value of Assets - Liabilities) / Total Outstanding Units

Liabilities include various policy expenses, charges, and fund management fees deducted from total assets.

WThe compound annual growth rate method computes your average annual return over the ten-year investment period.

CAGR Formula = [(Current NAV / Initial NAV) ^ (1 / Number of Years) - 1] × 100

Current NAV is the fund value at the end of ten years of your investment journey. Initial NAV is the fund value on your policy purchase date when the investment started initially.

You can choose between a single premium or a regular premium according to your financial situation. You have the option to make top-up payments anytime during the tenure to increase the investment amount. Also, partial withdrawals are allowed after completion of the mandatory five-year lock-in period.

The following are some ways to maximise your ULIP returns in 10 years.

Our experts are happy to help you!

Our experts are happy to help you!

A 10-year ULIP is an effective way to build wealth while protecting your family's financial future. Combining the dual benefit of market-linked5 growth potential with life insurance coverage, it helps in meeting your long-term financial goals. The right fund selection, discipline, and periodic monitoring are all important parameters for maximising returns over the decade. Understanding how charges, market cycles, and compounding work together enables sound investment decisions for optimal outcomes. Consider your risk tolerance and financial goals before investing in a 10-year ULIP plan.

1.

Yes, you can withdraw after the 5-year lock-in period, but early withdrawals may result in reduced long-term growth.

2.

ULIP returns fluctuate with market movement. Strong markets generally boost growth, while weak phases reduce performance. Long-term holding usually smooths short-term volatility.

3.

ULIPs can support long-term needs like education or retirement, but estimating the required contribution through a ULIP calculator helps align your goals and expectations.

4.

Past ULIP results offer useful guidance; however, they cannot assure future outcomes. Regular reviews and timely fund switches may help you align the plan with your goals and risk tolerance.

5.

Some equity-oriented ULIPs have provided substantial long-term gains, but the results depend upon the fund chosen, market cycles, and regular investing.

6.

You can follow your ULIP through NAV updates, fund reports, and online dashboards. Periodic monitoring of fund allocation and charges can support better decision-making.

7.

ULIP maturity proceeds may be exempt under Section 10(10D) if policy conditions are met, as per prevailing tax2 laws and eligibility.

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP, a non-participating, unit-linked, individual life insurance savings plan (UIN: 110L174V02), and Tata AIA Health Buddy, Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually.

This advertisement is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). These products are also available for sale individually without the combination offered/ suggested.

1Illustration shows a monthly premium of ₹20,000 for Tata AIA Premier SIP for a 30-year-old male, standard life, premium payment term: 10 years, policy term: 10 years with 100% investment in Tata AIA Multi Cap Fund in Future Secure plan option. 4% and 8% are assumed rates of return. 19.87% is the 5-year return of Nifty 500 Index as of October'25. Maturity amount: ₹25,86,726 at 4% returns, ₹31,74,241 at 8% returns and ₹ 59,28,633 at 19.87% returns. The fund value calculation is done by projecting the past returns of Nifty 500 Index after adjusting for all expenses in Tata AIA Premier SIP. The above values have been calculated assuming 19.87% p.a. gross investment returns, which is the past 5-year return of Nifty 500 Index as of October'25.

2No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfillment of conditions stipulated therein. The Tax-Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

3All funds open for new business which have completed 5 years since inception are rated 4 star or 5 star by Morningstar as of August 2025.

©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

45-year computed NAV for Multi Cap Fund as of November 2025. Other funds are also available. Benchmark of this fund is S&P BSE 200.

5Market-linked returns are subject to market risks and terms & conditions of the product. The assumed rate of returns or illustrated amount may not be guaranteed and depends on market fluctuations

Linked Life Insurance products are different from traditional insurance products and are subject to risk factors.

The premium paid in Linked Life Insurance policies is subject to investment risks associated with capital markets and publicly available index. The NAV of the units may go up or down based on the performance of Fund and factors influencing the capital market/publicly available index and the insured is responsible for his/her decisions.

Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & Tata AIA Smart Sampoorna Raksha Supreme, Tata AIA Smart SIP are only the names of the Unit Linked Life Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the insurance company.

The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns.

Past performance is not indicative of future performance.

If your policy offers variable benefits, then the illustrations on this page will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. Insurance cover is available under this product.

L&C/Advt/2026/Jan/0140

Begin your investment early: Starting early provides more time to grow and capitalise on the compounding effect significantly. Early investment helps you accumulate a significant corpus even with small premium amounts over the decade.

Begin your investment early: Starting early provides more time to grow and capitalise on the compounding effect significantly. Early investment helps you accumulate a significant corpus even with small premium amounts over the decade.