Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

A 30-year ULIP policy offers a combination of life insurance coverage and investment exposure to market-linked5 funds over an extended period. ... Read more These plans allocate your premium between insurance charges and investment in equity or debt funds based on your preference. The 30-year tenure provides substantial time for wealth accumulation through compounding while maintaining financial protection for your family. Read less

A 30-year ULIP policy offers a combination of life insurance coverage and investment ... Read more exposure to market-linked5 funds over an extended period. These plans allocate your premium between insurance charges and investment in equity or debt funds based on your preference. The 30-year tenure provides substantial time for wealth accumulation through compounding while maintaining financial protection for your family. Read less

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

₹1 Crore

4% and 8% are assumed rates of return. Tata AIA Multi Cap Fund Returns since inception: 20.38% (Benchmark: 12.98%) as of Nov'25

by paying a premium of ₹21,749/month (for 5 years)

Save ₹1,202 with discounts

Select an option

Select an option

10% discount on health product premium every year Additional fund booster will be added at the end of the policy term which is a defined % of average fund value on the last business day of the last eight policy quarters (2 years)

| Policy Term (years) | Fund Booster % |

|---|---|

| 30-34 | 7% |

| 35-39 | 8% |

| 40 and above | 10% |

| Fund Name | 5 Year Returns |

Benchmark Returns |

Benchmark Name |

|---|---|---|---|

| Multi Cap Fund | 23.21% | 16.65% | S&P BSE 200 |

| Top 200 Fund | 24.08% | 16.65% | S&P BSE 200 |

| India Consumption Fund | 23.85% | 16.65% | S&P BSE 200 |

Returns as of November, 2025

Our sales representative will connect with you soon to assist further

Param Raksha Life Pro +. This advertisement is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). These products are also available for sale individually without the combination offered/suggested. This benefit illustration is the arithmetic combination and chronological listing of combined benefits of individual products. The customer is advised to refer the detailed sales brochure of respective individual products mentioned herein before concluding sale.

A 30-year ULIP is a unit-linked insurance plan that extends over three decades, integrating life insurance protection with investment opportunities. The premium payment is divided into two components: one-part funds the life cover, while the other is allocated to your selected investment funds. Policyholders can select from equity funds for growth potential, debt funds for stability, or a balanced combination depending on their risk capacity and financial objectives.

A 30-year ULIP policy works by dividing your premium between two main components: insurance and investment. The structure works in the following way:

To better understand this, let's see an example. Suppose a person invests ₹1,00,000 every year, splitting 50% for equity and the rest 50% for debt. Then after 30 years, the total amount accumulated would be about ₹1.13 crore, considering an 8% annual average return. This indicates the wealth creation through ULIP investments that are made systematically over a long term.

Note: These are illustrative calculations, and actual returns may vary depending upon market performance and the fund selected.

These are some of the reasons a long-term ULIP may be considered:

Below are some factors that may affect ULIP performance:

Fund values fluctuate with the markets. Equity funds respond to uptrends and downtrends in the stock market, while debt funds are impacted by interest rates. A 30-year tenure exposes one to multiple market cycles.

Your decision between equity, debt, or balanced funds involves the potential for returns. While equity funds carry higher growth potential with increased volatility, debt funds generally provide more stable but moderate returns.

ULIPs involve charges for premium allocation, fund management, policy administration, and mortality cover. The charges may lower the net returns over the investment period.

Regular premiums ensure the continuity of the funds' accumulation. Non-payment may lead to policy lapse or revival charges, thereby hampering investment growth.

Fund performance can be impacted by inflation, interest rates, and even changes in regulations. Economic growth supports performance for equity funds, while debt funds may perform during stable interest rate environments.

Rebalancing between funds at the right time may help optimise returns. However, switching too frequently or at inappropriate times may affect the overall performance.

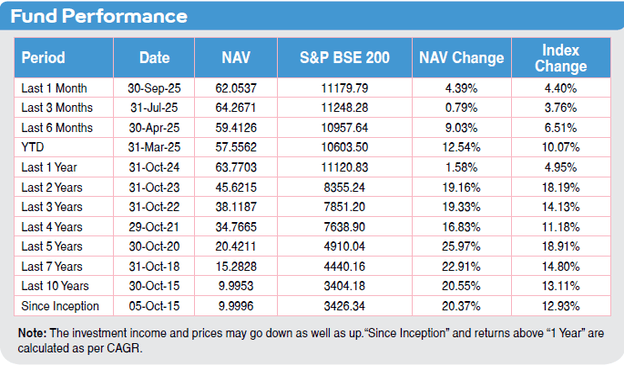

Returns as on

The following are the steps for calculating returns for a 30-year ULIP policy:

Amounts are based on a 20-year-old non-smoker male, with a 20-year premium payment term and a 30-year policy term, Tata AIA Premier SIP Future Secure plan option under the limited payment method with 100% invested in Tata AIA MultiCap fund at 8% Rate of Return.

The following approaches may help increase ULIP performance over 30 years:

A 30-year ULIP policy provides an approach to long-term investing combined with life insurance protection. The extended 30-year duration offers substantial time for investment growth through compounding while maintaining flexibility through fund switching options and goal-based planning. As market-linked5 instruments, ULIP returns are influenced by fund performance and economic conditions over the policy term. Regular evaluation of fund choices, maintaining premium payment discipline, and aligning the investment with your risk tolerance may assist in a better investment experience.

1.

The return range varies according to fund selection and market conditions. Equity-oriented funds offer higher growth potential with increased volatility, while debt funds usually provide moderate but stable returns over the investment period.

2.

The maximum ULIP returns in the last 30 years. However, it is not fixed because performance depends upon the particular fund, time period, and specific market cycles.

3.

Apart from the five-year lock-in period, partial withdrawals are normally allowed. The amount would depend on the policy terms and the fund value when a withdrawal request is made.

4.

The underlying fund's NAV is directly impacted by market conditions. The extended 30-year duration may provide an opportunity to offset short-term market volatility through multiple economic cycles; this does not eliminate market-related investment risks.

5.

Comparing projected outcomes with your financial requirements helps assess whether the investment meets your needs. Returns may be affected by the fund, time horizon of the investment, and market performance.

6.

Historical returns may provide a rough estimate, but one should not base an entire financial plan on them. The future return could vary as market conditions, economic environments, and fund performance fluctuate over time.

7.

Most ULIPs do not assure any returns since they are market-linked products. Final returns depend on the performance of selected funds and applicable charges throughout the 30-year investment period.

8.

Tax treatment would depend upon policy structure and the prevailing tax laws applicable on maturity of the contract. Maturity benefits may be exempt from tax under certain conditions, as per the applicable tax laws. Consult a tax2 advisor in cases of specific situations.

9.

Insurers may offer bonuses or loyalty rewards, but they depend on an insurer’s discretion and also depend on the policy term.

10.

Generally, ULIPs allow switching between funds, which means the investor could switch between equity, debt, and balanced funds. Hence, it is possible to adjust asset allocation if the goal of investment, or life stage, or market conditions changes during the tenure.

11.

Many ULIPs offer a fund switching feature that allows policyholders to change their investment allocation among the available fund options.

Asset Allocation: The appropriate mix of equity and debt can be decided based on age, risk tolerance, and financial goals. Younger investors may allocate higher percentages to equity, while those nearing their goal timeline may increase the debt allocation.

Asset Allocation: The appropriate mix of equity and debt can be decided based on age, risk tolerance, and financial goals. Younger investors may allocate higher percentages to equity, while those nearing their goal timeline may increase the debt allocation.