Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

A Unit Linked Insurance Plan with a 35-year tenure combines life insurance protection and market-linked5 investments in a single financial product. ... Read more Over such an extended period, policyholders have the opportunity to work toward building wealth while maintaining insurance coverage for their families. The extended investment horizon may help balance short-term market movements, and this combination of insurance and investment features makes ULIPs a consideration for individuals planning long-term objectives such as retirement or legacy creation. For those evaluating ULIP returns in 35 years, understanding how time, market behaviour, and investment strategy impact them becomes an important part of the decision-making process. Read less

A Unit Linked Insurance Plan with a 35-year tenure combines life insurance protection and ... Read more market-linked5 investments in a single financial product. Over such an extended period, policyholders have the opportunity to work toward building wealth while maintaining insurance coverage for their families. The extended investment horizon may help balance short-term market movements, and this combination of insurance and investment features makes ULIPs a consideration for individuals planning long-term objectives such as retirement or legacy creation. For those evaluating ULIP returns in 35 years, understanding how time, market behaviour, and investment strategy impact them becomes an important part of the decision-making process. Read less

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Premier SIP Calculator

Pay (Total)

₹11,99,016

Get Maturity Benefit

Based on assumed rate of return

₹34.57 Lakh

As per actual past performance

₹70.50 Lakh

@20.37%Additional Benefits

Life Cover (including Terminal Illness Cover): ₹22.8 Lakh

Accidental Death Cover: ₹11.43 Lakh

Accidental Total & Permanent Disability: ₹11.43 Lakh

Discounts

1% discount on 1st year premium for all payments paid through any permissible electronic mode debited through an auto-debit mandate. Maximum discount capping: ₹100 over the year.

Applicable if the policy is purchased digitally.

This discount is auto-applied and can't be removed

Buy Now

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP - Non-Participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V02) and Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually. Product option: Future Secure

A 35-year ULIP is essentially a financial product that serves two purposes: it provides life insurance while also investing a portion of your funds in various market-linked5 funds. When you pay your premium, part of it goes toward securing life cover for your family, and the rest gets invested according to your choice of equity, debt, or balanced funds. The policy runs for the entire 35-year period, during which your funds stay invested and grow based on how the chosen funds perform. After the initial five-year period, you can switch between different fund types, make partial withdrawals if needed, or adjust your coverage. When the policy reaches maturity, you receive the accumulated value as a lump sum.

Your premium payment doesn't entirely go into investments. The insurance company first deducts certain charges like mortality charges for the life cover, administrative costs, and fund management fees. The remaining funds then buy units in your selected fund based on that day's Net Asset Value (NAV). Think of it like buying shares; your account holds these units, and their value moves up or down with market performance.

The funds you've invested grow in two main ways: the underlying assets appreciate in value, and any dividends earned get reinvested. Equity funds might perform strongly during economic upswings, while debt funds tend to provide more stable, though typically lower, returns. Having 35 years gives your investments enough time to recover when markets go through rough patches.

Life changes, and so do financial priorities. ULIPs let you switch between different fund types. Someone in their early 30s might feel comfortable with aggressive equity investments, but as they approach their 50s, shifting toward more conservative debt funds often makes sense.

Real-Life Example

Take Priya, for instance, who started her 35-year ULIP at the age of 28 years with an annual premium of ₹ 60,000. She initially allocated 80% to equity and 20% to debt, feeling she had time to be invested through market swings. By her mid-40s, when she was closer to retirement, she gradually shifted to a 40-60 split. If her equity investments averaged around 10% returns and debt around 7% over these decades, she may have ULIP returns in the last 35 years somewhere in the range of ₹ 95 lakh to ₹ 1 crore by the age of 63, and throughout the period her family had life insurance protection.

Here’s why you should choose a 35-year ULIP policy:

Time is an important factor in investing. In 35 years, even modest ULIP returns can compound substantially. The key is consistency and patience, allowing your funds to grow through multiple market cycles.

For most people, retirement is planned and thought out rather late in life. A 35-year ULIP can act as a dedicated retirement vehicle, building up a financial cushion to complement other retirement income sources like EPF or pension plans.

Unlike individual investment products, your family gets financial protection in case something unfortunate happens to you. This coverage would continue throughout the tenure of the policy while giving peace of mind alongside wealth creation.

ULIP may be suitable from a financial planning viewpoint due to its tax treatment. The premium paid normally qualifies for a deduction, and the maturity amount could be received tax-free2 under the existing provisions; do check the current regulations.

The ability to switch funds, make partial withdrawals after the lock-in period, and adjust your strategy gives you control over your investments.

Regular premium payments create a structure that encourages disciplined investing.

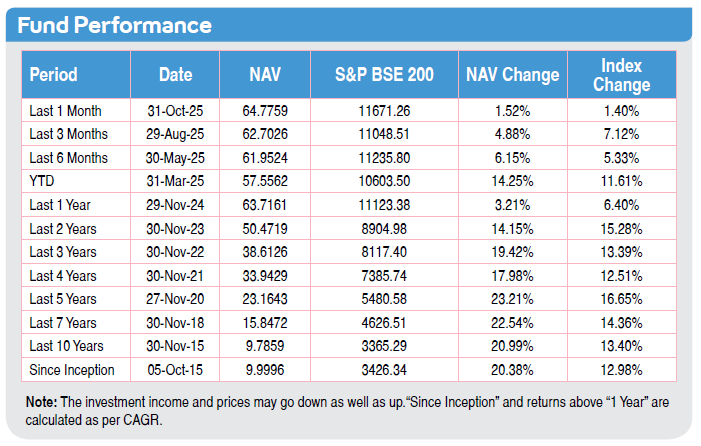

Returns as on

The following factors affect ULIP performance:

Markets and economic cycles do not follow a predictable course. In a 35-year investment time frame, you are likely to experience multiple phases-periods of robust economic expansion, market corrections, and phases of modest recovery. Factors such as the rate of growth in GDP, corporate profitability, and inflationary pressures influence the overall performance that your selected funds will produce over time.

The basic distribution of your investment between equity and debt instruments is crucial in determining long-term outcomes. While equity-focused portfolios may offer higher returns, they are also accompanied by increased market volatility. Debt investments are generally characterised by more stable but moderate growth over longer periods.

Fund managers make numerous investment decisions throughout the policy tenure, like selecting securities, determining entry and exit points, and managing portfolio risk. The competence and experience of these professionals can significantly influence your accumulated corpus over three and a half decades.

Various charges reduce the amount available for investment and subsequent growth. These include mortality charges, policy administration fees, and fund management costs, which vary across insurers and policy structures. Lower charges ensure that a larger portion of your premium remains invested and benefits from compounding.

Interruptions in premium payments or policy lapses can disrupt the compounding process considerably. Maintaining regular contributions throughout the policy term provides your investment with the optimal environment for substantial growth.

While reallocating between funds at suitable moments can enhance returns, consistently timing market movements correctly remains challenging. Poorly executed switches may result in realising losses or missing subsequent market recoveries.

Inflation gradually diminishes the purchasing power of your returns. For instance, earning 8% annually becomes less impressive when inflation runs at 6%, leaving only 2% real growth. Additionally, interest rate fluctuations affect both equity valuations and debt instrument yields.

Current tax provisions generally favour ULIPs, though regulatory frameworks can evolve over such extended periods. While existing investments often receive grandfather clause protection, it's worth noting that tax treatments applicable today may be subject to revision in the future.

Amounts are based on a 20-year-old non-smoker male, with a 20-year premium payment term and a 30-year policy term, Tata AIA Premier SIP Future Secure plan option under the limited payment method with 100% invested in Tata AIA MultiCap fund at 8% Rate of Return.

Net Asset Value serves as the foundation for all return calculations; it represents the per-unit price of your chosen fund. NAV fluctuates daily based on the performance of underlying investments, which explains the varying values shown in your periodic statements.

The number of units allotted to your account is calculated by dividing your invested amount (after deducting the applicable charges) by the prevailing NAV. For instance, in case an amount of ₹48,000 is invested at an NAV of ₹12, you will be allotted 4,000 units.

The monitoring of NAV over these years gives you a clear view of the growth of your investment. For example, if the NAV grows from ₹12 to ₹120 in 35 years, the 4,000 units would then be worth ₹4,80,000, which showcases substantial growth.

Each subsequent premium paid buys additional units at the current NAV. These then appreciate with your already acquired units, creating layers of investments that increase over a period of time.

The most straightforward calculation involves subtracting total premiums paid from the final fund value. While this shows your nominal gain in rupees, it doesn't account for the time value of money or facilitate meaningful comparisons across different investment durations.

Compound Annual Growth Rate (CAGR) provides a more standardised measure of performance. It indicates what consistent annual return would have been required to achieve your actual outcome. The calculation follows this formula: [(Final Value / Initial Investment)^(1/years) - 1] × 100. This metric enables easier comparison across different investment options.

Nominal returns alone don't help you understand the complete picture. Subtracting average inflation from your nominal returns reveals how much your purchasing power actually increased. For instance, a 9% nominal return during a period of 5% average inflation translates to approximately a 4% real return.

The key advantages of ULIP plans for 35 years include the following:

Consistent investing over three and a half decades allows even moderate contributions to accumulate into a considerable corpus. While the initial projections may seem abstract, the effect of compounding over such extended periods can yield results that exceed many investors' initial expectations.

This financial instrument addresses two distinct needs within a single framework. As your investments work toward building wealth, your family simultaneously benefits from life insurance protection. This integrated structure may suit to those seeking comprehensive financial planning solutions.

The tax structure offers efficiency at multiple stages. Premiums may qualify for deductions during the accumulation phase, while maturity benefits are often received without tax liability. This arrangement allows more of your money to remain invested rather than being diverted to taxation, though it's essential to verify provisions under current regulations.

Life circumstances often evolve in unexpected ways. ULIPs provide flexibility for such changes through features like fund switches, coverage adjustments, and strategy modifications, all without necessitating policy cancellation and fresh enrollment.

Certain situations require access to accumulated funds before the policy matures. Whether for educational expenses, medical needs, or other significant requirements, the partial withdrawal option available after five years provides financial flexibility while maintaining policy continuity.

Regular statements provide complete visibility into your holdings, unit count, current NAV, and total fund value. This transparency eliminates uncertainty and enables informed decision-making regarding any necessary adjustments.

Historical data indicates that equity investments have consistently outpaced inflation over extended periods more reliably than many alternative asset classes. This characteristic makes them particularly valuable for preserving and enhancing purchasing power across multiple decades.

Effective investment oversight requires considerable time and specialised knowledge. Having experienced professionals manage these aspects while you focus on your primary occupation and personal commitments offers substantial practical value.

Our experts are happy to help you!

Our experts are happy to help you!

1.

Returns vary considerably based on fund type and market conditions. Ensure you consult a financial advisor before making a choice.

2.

Partial withdrawals become available after five years, though they reduce your eventual corpus. Completely surrendering the policy before maturity usually involves surrender charges and potential tax2 implications.

3.

Short-term market movements affect the NAV daily. Over a 35-year horizon, investments typically move through several market cycles, which may help offset short-term volatility. Outcomes, however, remain dependent on overall market conditions.

4.

ULIP returns vary widely based on fund type and market behaviour. Some periods have been more favourable than others, but past outcomes should not be treated as indicators of future performance.

5.

ULIPs do not guarantee investment returns, as fund performance is market-linked5. The life insurance component continues as per policy terms, regardless of investment results.

6.

Under prevailing regulations, maturity proceeds may be tax-exempt2 if certain premium conditions are met, and premiums may be eligible for deductions under Section 80C. Since tax rules may change, reviewing the latest provisions is advisable.

7.

At maturity, the fund value is paid out. This is calculated by multiplying the total units accumulated by the prevailing NAV, after accounting for charges deducted over the policy term.

8.

Usually, ULIPs allow fund switches between equity, debt, and balanced options. This feature may help policyholders align their asset allocation with changing goals, risk tolerance, or market conditions.

9.

Both serve different purposes. ULIPs provide life insurance along with long-term investment features, while mutual funds offer greater flexibility and generally lower costs but do not include insurance. The suitability of either option depends on individual requirements and priorities..