Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

A ULIP is a unique life insurance which offers both protection and market-linked investment benefits. A certain part of the premium you pay goes... Read more for the life cover, and the other for investing in market-linked funds5. Investment in ULIP policies for 40 years provides sufficient time for the growth of the investment through compounding. The combined effect of compounding and strong market performance can help build a substantial corpus. With the ULIP returns in 40 years, you can support long-term goals, such as retirement or children’s education. Read less

A ULIP is a unique life insurance which offers both protectionand market-linked ...Read more investment benefits. A certain part of the premium you pay goes for the life cover, and the other for investing in market-linked funds5. Investment in ULIP policies for 40 years provides sufficient time for the growth of the investment through compounding. The combined effect of compounding and strong market performance can help build a substantial corpus. With the ULIP returns in 40 years, you can support long-term goals, such as retirement or children’s education. Read less

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Premier SIP Calculator

Pay (Total)

₹11,99,016

Get Maturity Benefit

Based on assumed rate of return

₹34.57 Lakh

As per actual past performance

₹70.50 Lakh

@20.37%Additional Benefits

Life Cover (including Terminal Illness Cover): ₹22.8 Lakh

Accidental Death Cover: ₹11.43 Lakh

Accidental Total & Permanent Disability: ₹11.43 Lakh

Discounts

1% discount on 1st year premium for all payments paid through any permissible electronic mode debited through an auto-debit mandate. Maximum discount capping: ₹100 over the year.

Applicable if the policy is purchased digitally.

This discount is auto-applied and can't be removed

Buy Now

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP - Non-Participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V02) and Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually. Product option: Future Secure

A 40-year ULIP gives you long-term life cover while also investing your money in market-linked funds5. It suits investors who want to build wealth steadily for major future goals, such as retirement or children’s education. With such a long horizon, your investment gets time to grow through compounding, while the flexibility to switch between equity, debt, and balanced funds lets you adjust your strategy as markets change. Overall, it works as a single solution that combines financial protection with the potential for significant long-term growth.

A 40-year ULIP gives you long-term life cover while also investing your money in market-linked funds5. It suits investors who want to build wealth steadily for major future goals, such as retirement or children’s education. With such a long horizon, your investment gets time to grow through compounding, while the flexibility to switch between equity, debt, and balanced funds lets you adjust your strategy as markets change. Overall, it works as a single solution that combines financial protection with the potential for significant long-term growth.

Here's how this ULIP policy works:

Here’s an example to understand 40-year ULIP policy:

Akash buys a 40-year ULIP policy at the age of 30 years. He opts to pay an annual premium. The insurer will utilise a small portion of premium to buy life insurance cover and invest the remaining corpus in equity and debt funds, depending upon Akash’s risk profile.

Akash can review market conditions and shift his investments from equity to hybrid funds in order to balance risk. If he were to pass away during the policy term, his nominee would receive the higher of the sum assured or the fund value, ensuring financial support when it’s needed most. If Akash completes the entire 40-year term, at maturity, ULIP returns in the last 40 years lead to an accumulated fund value that can be withdrawn to meet long-term goals such as retirement planning or children's education.

Here are some of the prominent reasons to choose a ULIP policy with a 40-year term:

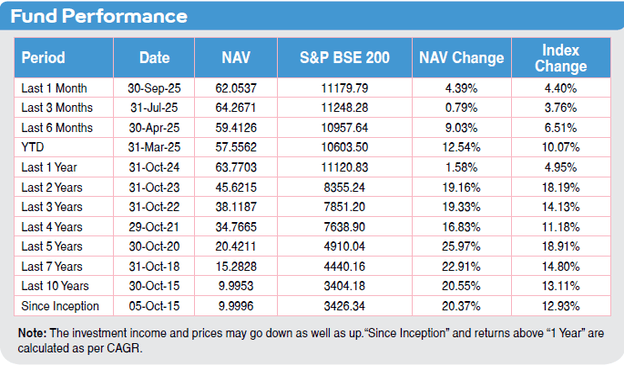

Returns as on

The following factors are the key determinants of the overall performance of ULIP:

Follow the below steps to calculate ULIP policy return:

Your ULIP’s performance is closely linked to the premium you choose and how much of it ultimately goes into investments. Paying a higher premium means a larger portion is directed into market-linked funds, which can help build more wealth over time. It’s important, however, to pick a premium amount that you can comfortably maintain throughout the full duration of the policy.

The length of your investment directly impacts returns. A 40-year ULIP plan allows compounding to work effectively and can generate substantial returns if the market performs well. Early withdrawals or surrendering the policy will reduce your returns.

NAV is the market value of the underlying assets in which your premiums are invested. It is calculated as:

NAV= (Fund’s Assets - Fund’s Liabilities) / Total Number of Units Outstanding

NAV changes daily and forms the basis for calculating your ULIP returns..

ULIP returns are often calculated using the time-weighted return, which measures the compound growth of your investment over time. This method factors in the performance of funds regardless of when premiums are paid or withdrawals are made.

The returns of your ULIP depend on how the underlying funds perform. Each fund has a specific investment strategy and objective. Market conditions, asset allocation, and fund manager decisions influence fund performance, which directly affects your ULIP returns over 40 years.

Various charges reduce the amount invested in the funds. These include:

Amounts are based on a 20-year-old non-smoker male, with a 20-year premium payment term and a 30-year policy term, Tata AIA Premier SIP Future Secure plan option with 100% invested in Tata AIA Multi Cap Fund at 8% Rate of Return. Returns at 4% for investment of ₹5000/month, ₹10,000/month, ₹15,000/month and ₹20,000/month are 24 Lakh, 49 Lakh, 73 Lakh and 98 Lakh respectively.

The main advantages of investing in ULIPs for 40 years are as follows:

The following points can help you to maximise your ULIP returns in 40 years:

Our experts are happy to help you!

Our experts are happy to help you!

A 40-year ULIP policy combines long-term investment with life cover, giving your money time to grow while keeping your family protected. Its performance depends on factors such as market trends, economic conditions, fund choices, and your overall investment approach. It is important to stay updated with market trends and review your ULIP policy regularly. If invested for the long term, steady contributions can serve as a reliable way to build wealth and strengthen your long-term financial security.

1.

The average annual return on a ULIP typically ranges from 8% to 12% over 10 years. However, returns vary with market performance and carry associated risks.

2.

Yes, you can withdraw your ULIP investment before 40 years, provided you complete the 5-year lock-in period.

3.

Equity funds tend to perform well in favourable markets but may decline during downturns, whereas debt funds offer greater stability. Long-term investing and strategic fund allocation help manage risk and enhance growth potential.

4.

Yes, generally ULIP returns in 40 years are sufficient for long-term goals such as child education, retirement goals, etc.

5.

It is not advisable to rely solely on historical ULIP returns for future financial planning, as past performance does not guarantee or reliably predict future results.

6.

There is no specific "maximum" ULIP return over 40 years, as returns are market-linked and depend on fund type, provider, charges, and market cycles.

7.

Since ULIPs are market-linked products, there is no guarantee on ULIP returns.

8.

Depending on the policy's date of issuance and the annual premium paid, there can be tax implications on ULIP returns.

9.

Bonuses, such as loyalty additions and wealth boosters, are designed to reward investors who maintain their ULIP investment for the entire 40-year term.

10.

Yes, you can adjust asset allocation within the ULIP to manage the risk.

10.

ULIPs and FDs serve different purposes: ULIPs offer market-linked growth with life insurance, suitable for long-term goals and risk-tolerant investors, while FDs provide fixed, guaranteed returns, ideal for short-term needs or conservative investors.

10.

ULIPs and PPFs have different purposes. ULIPs provide market-linked growth with life insurance for long-term, risk-taking investors, while PPF offers fixed, guaranteed returns for conservative investors seeking safety and steady, tax-free2 savings.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP, a non-participating, unit-linked, individual life insurance savings plan (UIN: 110L174V02), and Tata AIA Health Buddy, Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually

1Illustration shows a monthly premium of ₹10,000 for Tata AIA Premier SIP for a 30-year-old male, standard life, premium payment term: 5 years, policy term: 40 years with 100% investment in Tata AIA Multi Cap Fund in Future Secure plan option. 4% and 8% are assumed rates of return. 19.87% is the 5-year return of Nifty 500 Index as of October'25. Maturity amount: ₹3,24,456 at 4% returns, ₹18,91,301 at 8% returns and ₹ 11,50,91,164 at 19.87% returns. The fund value calculation is done by projecting the past returns of Nifty 500 Index after adjusting for all expenses in Tata AIA Premier SIP. The above values have been calculated assuming 19.87% p.a. gross investment returns, which is the past 5-year return of Nifty 500 Index as of October'25.

2No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfillment of conditions stipulated therein. The Tax-Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

3All funds open for new business which have completed 5 years since inception are rated 4 star or 5 star by Morningstar as of August 2025.

©2024 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

5Market-linked returns are subject to market risks and terms & conditions of the product. The assumed rate of returns or illustrated amount may not be guaranteed and depends on market fluctuations

Linked Life Insurance products are different from traditional insurance products and are subject to risk factors

The premium paid in Linked Life Insurance policies is subject to investment risks associated with capital markets and publicly available index. The NAV of the units may go up or down based on the performance of Fund and factors influencing the capital market/publicly available index and the insured is responsible for his/her decisions.

Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & Tata AIA Smart Sampoorna Raksha Supreme, Tata AIA Smart SIP are only the names of the Unit Linked Life Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns

Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the insurance company.

The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns.

Past performance is not indicative of future performance.

If your policy offers variable benefits, then the illustrations on this page will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. Insurance cover is available under this product.

L&C/Advt/2026/Jan/0138