Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

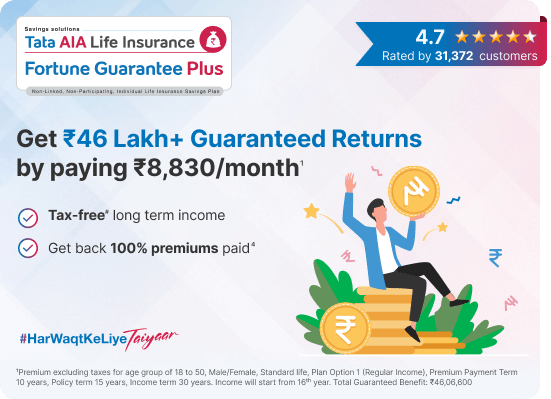

Mr. Nakul, aged 30, is a small business owner. Worried by the uncertain nature of life, he wants a steady income for himself and his family in the future. He opts for Tata AIA Fortune Guarantee Plus | Regular Income Option.

Premium Payment Term - 12 years | Policy Term - 12 years | Income Mode -Annual | Annual premium - ₹1,00,000 (Excl. GST)1

Mr. Nakul, aged 30, is a small business owner. Worried by the uncertain nature of life, he wants a steady income for himself and his family in the future. He opts for Tata AIA Fortune Guarantee Plus | Regular Income Option.

Premium Payment Term - 12 years | Policy Term - 12 years | Income Mode -Annual | Annual premium - ₹1,00,000 (Excl. GST)1

Age

Pays 1 Lakh for 12 years. Total = 12 Lakh

Gets ₹1.1 Lakh for 30 years

Guaranteed* benefit

₹43,81,200

Pays 1 Lakh for 12 years. Total = 12 Lakh

Gets ₹1.1 Lakh for 30 years

Guaranteed* benefit

₹43,81,200Total Guaranteed* Benefit = 1,11,040x30 (annual income) + 1,00,000x12 (get premiums back) = ₹43,81,200

Life Cover = ₹12.5 Lakh

*T&C Apply

Mr Rahul, aged 35, is an IT professional and is doing well at present. He wants a steady income for himself and his family in the future. He opts for Tata AIA Fortune Guarantee Plus- A savings insurance plan with Regular Income + Critical Illness Option.

Premium Payment Term - 10 years | Policy Term - 10 years | Income Mode -Annual | Annual premium - ₹1,00,000 (Excl. GST)

Mr Rahul, aged 35, is an IT professional and is doing well at present. He wants a steady income for himself and his family in the future... Read moreHe opts for Tata AIA Fortune Guarantee Plus- A savings insurance plan with Regular Income + Critical Illness Option. Premium Payment Term - 10 years | Policy Term - 10 years | Income Mode -Annual | Annual premium - ₹1,00,000 (Excl. GST) Read less

Age

Premium Payment starts ₹1 Lakh annually

Premium of ₹7 lakh is waived off from 4th year

Diagnosed with illness pays only ₹3 Lakh premium

Gets ₹83,400 for next 33 years

Guaranteed* benefit

₹29,57,870

Premium Payment starts ₹1 Lakh annually

Gets ₹83,400 for next 33 years

Guaranteed* benefit

₹29,57,870Total Guaranteed Benefit* = ₹83,400x33 years (Annual income) + ₹1,00,000x3 (Get premiums back) = ₹29,57,870

Life Cover = ₹12.5 Lakh

*T&C Apply

Select from our 2 plan options

| Plan Options | Option 1 | Option 2 | ||

| Regular Income | Regular Income with an inbuilt Critical Illness benefit | |||

| Minimum Entry Age | 1 year (subject to a minimum maturity age of 18 years) | 18 years | ||

|---|---|---|---|---|

| Maximum Entry Age |

60 years | 60 years | ||

| Minimum Age at Maturity |

18 years | 23 years | ||

| Maximum Age at Maturity |

77 years | 70 years | ||

| Income Period |

20 to 45 years (in multiples of 5 years) Policy Term + Income period is within the range of 25 years to 50 years | 30 years for 5 pay and 25 years for 10 pay | ||

| Income Mode | Annual & Monthly | |||

| Coverage | Single Life & Joint Life (Joint Life for Single Pay option only) | |||

| Minimum Premium |

|

|||

| Maximum Premium | No Limit | |||

| OPTION 1: Regular Income |

OPTION 2: Regular Income with an inbuilt Critical Illness benefit |

|---|---|

| Minimum Entry Age | |

| 1 year (subject to a minimum maturity age of 18 years) | 18 years |

| Maximum Entry Age | |

| 60 years | 60 years |

| Minimum Age at Maturity | |

| 18 years | 23 years |

| Maximum Age at Maturity | |

| 77 years | 70 years |

| Income Period | |

| 20 to 45 years (in multiples of 5 years)

Policy Term + Income period is within the range of 25 years to 50 years |

30 years for 5 pay and 25 years for 10 pay |

| Income Mode | |

| Annual & Monthly | |

| Coverage | |

| Single Life & Joint Life (Joint Life for Single Pay option only) | |

| Minimum Premium | |

Single Life & Joint Life (Joint Life for Single Pay option only)

|

|

| Maximum Premium | |

| No Limit | |

All reference to age is as on last birthday. All premiums mentioned excludes taxes.

Our experts are happy to help you!

Our experts are happy to help you!

Enhance your coverage with riders

This plan offers the following optional riders9:

A Non-Linked, Non- Participating Individual Health rider (UIN: 110B045V03)

A Non-Linked, Non- Participating Individual Health rider (UIN: 110B046V04)

A Non-Linked, Non- Participating Individual Health Rider (UIN: 110B033V04)

A Non-Linked, Non-Participating Individual Pure Risk Health Rider (UIN: 110B049V03)

13T&C apply.

1.What is a savings policy?

A savings plan is a life insurance plan that provides an avenue for savings for important life goals and a basic life cover to support your family financially. The life cover will provide financial security to your family and ensure a steady source of income in absence of the life assured so that their lifestyle is not compromised.

2.What are riders? Why do I need a rider?

Riders9 are add-on benefits that can be attached to a life insurance plan at a nominal cost. These riders offer multiple benefits such as coverage against accidental death, disability, critical & terminal illness, unforeseen medical expenses, etc.

3.What is a claim settlement ratio?

The claim settlement ratio is referred to as the number of claims that have been passed by an insurance company. It is the ratio of the number of claims settled by an insurer to the number of claims filed in a given period.

4.What is a regular income / guaranteed income insurance plan?

A regular income or guaranteed income insurance plan is a savings plan that allows you to accumulate a savings corpus over the policy term, along with a basic life cover. When the policy matures, you can choose to receive the guaranteed benefits of the plan, which is the accumulated financial corpus in the form of a regular/guaranteed income for an income period of your choice. Additionally, in case of your unfortunate demise, the family receives the death benefit.

5.Why do I need a savings plan?

A savings insurance plan provides an avenue for disciplined savings with guaranteed or non-guaranteed benefits to plan for important life goals. In addition, savings plans come with a basic life cover which ensures financial support to your loved ones in case of your absence.

6.When does a policy lapse?

When the premiums for 1 full year has not been paid within the grace period, the policy will lapse from the due date of first unpaid premium, and no benefits will be payable to the policyholder.

7.What is the difference between guaranteed income and whole life insurance?

Whole life insurance is a form of life insurance where the life cover or the policy term is up to the age of 100 years. This means that the policyholder’s family can be protected with a life cover for the policyholder’s entire lifetime. At the end of the policy term, a whole life plan may offer an accumulated corpus or the return of all the paid premiums as a survival benefit.

On the other hand, a guaranteed income plan is a savings avenue where the maturity benefits are assured or guaranteed and can be paid out as a regular income or as a lump sum, as per the policyholder’s choice. However, a guaranteed income plan may also offer the return of premiums with the maturity benefit.

In the case of whole life insurance as well as a guaranteed income plan, if the policyholder dies during the policy term, the insurance company will pay a death benefit to the appointed nominees.

8.What is the maturity benefit in a guaranteed income plan?

The maturity benefit in a guaranteed income plan is the money/funds saved over the policy term that has been paid in the form of premiums. This amount can either be paid out as a lump sum benefit or as a regular income once the policy matures.

9.Why purchase our best guaranteed return insurance plan?

With our best guaranteed return insurance plan, you can choose from the policy term and a sum assured of your choice to provide life insurance coverage to your family as per your insurance needs. To ensure that the premiums can be paid at your convenience, you can also choose a flexible premium paying term and frequency.

You can make the most of our guaranteed return insurance plan with a range of policy benefits, such as life cover, guaranteed returns, and regular savings through easy premium payments.

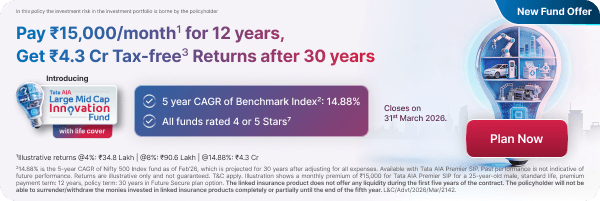

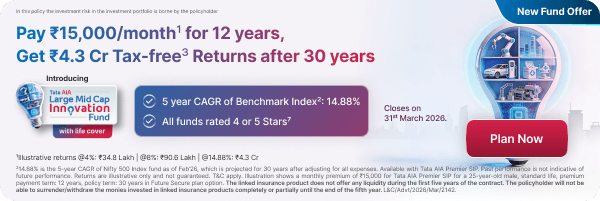

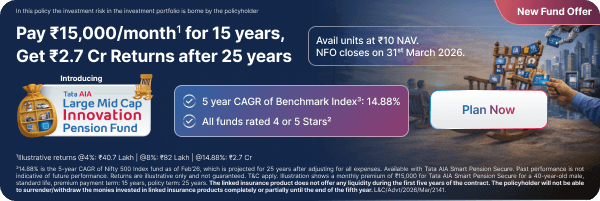

1.What are the variants of the Tata AIA Fortune Guarantee Plus plan?

The Tata AIA Fortune Guarantee Plus offers the following two variants:

●Regular Income ●Regular Income with an inbuilt Critical Illness benefit

2.Do I get any tax benefits with this plan?

Yes! You can save tax up to ₹46,8008 and avail tax benefits as per the applicable income tax laws. The premiums paid will qualify for tax benefits under section 80C of the income tax act.

3.What is the grace period for this plan?

This plan provides a grace period of 15 days for the monthly payment mode and 30 days for all other modes from the due date of subsequent premium payments.

4.Does this plan offer a Free Look period?

Yes, this plan has a free look period of 30 days from the date of issuance of the policy whether purchased electronically or otherwise.

5.Does the Tata AIA Fortune Guarantee Plus have a loan facility?

Yes, once the policy acquires a surrender value, you can apply for a policy loan for an amount that does not exceed 80% of the surrender value. The assignee of the policy will be Tata AIA Life.

6.Are guaranteed return plans tax-free?

With guaranteed2 return plans, such as Tata AIA Fortune Guarantee Plus (Non-Linked, Non-Participating, Individual Life Insurance Savings Plan (UIN: 110N158V14), you can save income tax3 up to ₹46,8008 every year.

2T&C apply

7.What is the difference between the plan variants, i.e., regular income and regular income with critical illness benefit?

There are very few differences between the two plan variants – regular income and regular income with critical illness benefit.

The main difference is that the second plan option comes with an inbuilt critical illness benefit that offers coverage against 40 critical illnesses, which the first plan option does not.

Only the Regular Pay option for premium payment is enabled under the second plan option, and the Income Period is different for both plan options – 20 to 45 years for option 1 and 30 or 25 years for option 2.

1.What is the minimum premium amount that needs to be paid for this plan?

When you purchase the Fortune Guarantee Plus by Tata AIA, the minimum premium amount to be paid (excluding taxes) is as follows:

●Single Pay (SA I) - ₹5,000 ●Single Pay (SA II): As per Minimum Sum Assured and Death Benefit Multiple (DBM) offered.

2.In which modes can I receive income from this plan?

You can choose to receive the income benefit from the plan either monthly or annually.

3.When do I receive the return of premium benefit with this plan?

The return of premium benefit will be payable at the end of the income period, irrespective of the survival of the policyholder during the income period.

4.Do I need to pay any extra premiums for the Tata AIA Fortune Guarantee Plus?

Apart from the base policy premiums, you will have to pay additional premiums only if you opt for a rider9 benefit to enhance the policy coverage.

5.What premium payment frequency options do I have under this policy?

You can pay your premiums for this policy through the Single, Annual, Half-yearly, Quarterly or Monthly modes.

6.Can I change the premium payment frequency?

The premium payment frequency is fixed at the time of policy purchase. But if you need to change the premium frequency, you can do so after the first policy year, when all the premiums for the first year are paid.

7.What is the maximum and minimum term for premium payments?

Under plan option 1, the minimum and maximum premium payment terms are:

●Single Pay (SA I) – 1 year for a policy term of 5 years ●Single Pay (SA II) – 1 year for a policy term of 5 & 10 years ●Limited Pay – 5 years for PT of 6-10 years and 12 years for PT of 13-17 years. ●Under plan option 2, the minimum and maximum premium payment terms are 5 and 10 years, respectively.

8.What if the premium payment is discontinued before and after the policy surrender?

If you discontinue the premium payment before surrendering the policy, you will get a grace period of 15/30 days (15 days for monthly mode, 30 days for all other modes) from the due date of the unpaid premium to pay the premium. The policy will be active during this time, and you can continue receiving life insurance coverage. However, the policy will lapse unless you pay your premiums after the grace period.

If you surrender your policy, the application will be reviewed by Tata AIA Life Insurance company, and once the surrender is accepted, you need not pay the policy premiums anymore.

1.Can I change the plan option once chosen?

No. You can choose one of the two plan options – Regular Income or Regular Income with inbuilt Critical Illness benefit – only at the time of purchasing this savings plan and cannot make any changes after.

2.Which riders can I purchase with the Tata AIA Fortune Guarantee Plus plan?

With the Tata AIA Fortune Guarantee Plus plan, you can purchase the following riders9.

●Tata AIA Vitality Health - A Non-Linked, Non- Participating Individual Health rider (UIN: 110B045V03) ●Tata AIA Vitality Protect - A Non-Linked, Non- Participating Individual Health rider (UIN: 110B046V04) ●Tata AIA Non-Linked Comprehensive Protection Rider - A Non-Linked, Non- Participating Individual Health Rider (UIN:110B033V04) ●Tata AIA Benefit Protection Rider - A Non-Linked, Non-Participating Individual Pure Risk Health Rider (UIN: 110B049V03)

3.Does this plan provide an option for Joint Life Policy?

Yes, with the Regular Income variant of the Tata AIA Fortune Guarantee Plus plan, you can choose Joint Life Policy under the Single Pay mode for premium payments option.

4.What is the Income Period under this plan?

You can receive regular income under this plan during the Income Period starting from 20 years for as long as 45 years, as selected by you.

5.Does this plan offer a waiver of premium benefit?

Yes, if you choose the Regular Income with In-built Critical Illness benefit, the waiver of premium benefit will be applicable. During the policy term and before maturity, if you are diagnosed with a critical illness and the pay-out for the contingency has been made, the plan will continue to be in effect, and all future premiums will be waived off.

6.Does the plan provide death benefits along with maturity benefits?

No! if the insured passes away during the policy term, the nominee can file a death claim and receive the benefits. However, if the insured survives the policy term, they will receive the financial corpus accumulated under the savings policy as a maturity benefit.

1.What are the documents required for a claim settlement?

Please click on here to know the list of documents needed for the claim intimation and settlement process

2.How can I raise a claim under this savings policy?

To raise a claim, you can choose any of the following channels to reach out to us.●Email us at: customercare@tataaia.com ●Call our helpline number - 1860-266-9966 (local charges apply) ●Walk into any of the Tata AIA Life Insurance Company branch offices ●Write directly to us at:

The Claims Department,

Tata AIA Life Insurance Company Limited

B- Wing, 9th Floor,

I-Think Techno Campus,

Behind TCS, Pokhran Road No.2,

Close to Eastern Express Highway,

Thane (West) 400 607.

IRDA Regn. No. 110

3.How will the claim be processed if the nominee is outside of India?

If the nominee is outside of India and the claim needs to be filed, then the nominee can file the claim online by uploading the attested copies of the required documents online or through email. If the nominee wishes to file the claim offline, then they can courier their documents to their representative in India, who can visit our office and initiate the process.

4.Does the claim have to be filed at the same Tata AIA Life Insurance branch where the policy was purchased?

No, the claim can be filed at any Tata AIA Life Insurance branch, as per your/the nominee’s convenience. You can locate our office branches and visit the one nearest to you for the claim initiation.

5.Can I file a Critical Illness claim under this plan?

Yes, if you have chosen the Regular Income with In-built Critical Illness Benefit option under this plan, then you can file a claim with us if and when you are diagnosed with a critical illness that is listed in the policy.