Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

₹1.5 Cr Life Cover starts at ₹678/month1b

17.65% 5-year Tax-free1a returns1f

Don’t let Cancer Cancel your Income Flow

Life cover included.1b20 year old female (Standard Life, Non-Smoker), regular pay, 20 year policy term. 1f5 year returns of Tata AIA Multi Cap Fund as of Apr’26. Benchmark: 12.01%. Past performance is not indicative of future performance. 1gT&C apply.

L&C/Advt/2026/Jul/4466

Help me to

I want to

L&C/Advt/2026/Jul/4465

Life insurance is a legally binding contract between you (the policyholder) and a life insurance company that provides financial protection to your loved ones. In return for paying your premiums on time, the insurer promises to pay a pre-agreed amount, known as the sum assured or life cover... Read more , to your nominee if you pass away during the policy term.

Many life insurance plans also offer benefits for critical or terminal illnesses, and you can add optional accident or disability cover for extra protection. To get accurate life insurance quotes, you must share your health and lifestyle details honestly and choose between a single premium or regular premiums. This helps you find the right life insurance plan to support your family’s long-term financial stability. Read less

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Your premium calculation is in progress

Share your needs and get

Non-Linked, Non-Participating, pure risk, Individual Life Insurance Product (UIN:110N176V11)

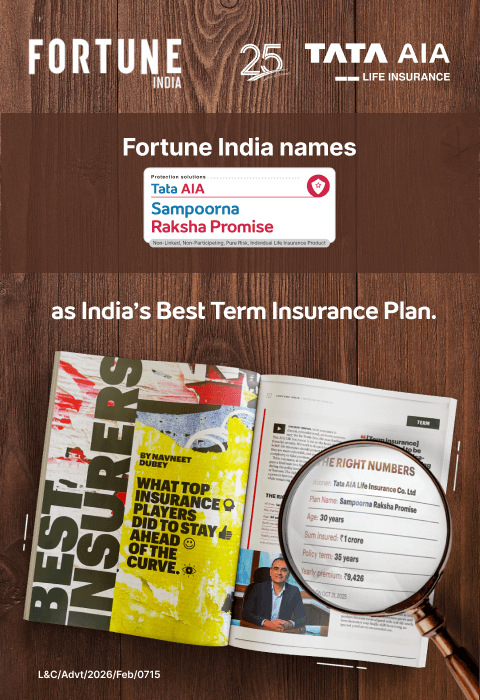

Tata AIA Sampoorna Raksha Promise

Get ₹1 Crore Life cover @ ₹826/month1

Age: 25

Cover till age: 60 yrs

Payment duration: 35 yrs

99.45%

Individual Death Claim

Settlement Ratio15

pay later option

Defer premium

by

12 months3

Instant Payout

on terminal illness

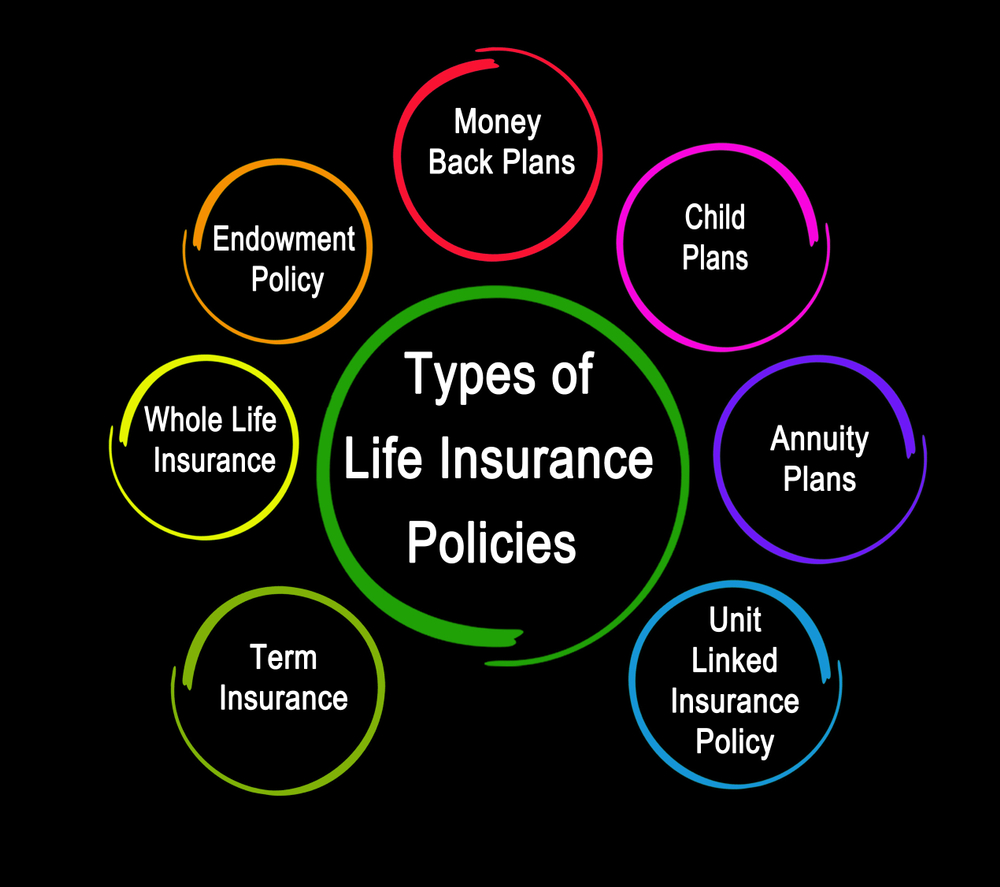

Life insurance comes with many choices, each designed for different financial needs. Some focus on protection, while others... Read more combine savings or future security. To help you decide what fits best, here are the main types of life insurance plans you should know about:

1. Term Plan

2. ULIPs

3. Endowment Policy

4. Money Back Policy

5. Retirement Plans

6. Child Plans

7. Participating Life Insurance Plans

8. Capital Guarantee Plans

9. Whole Life Insurance

10. Annuity Plans Read less

A term insurance plan is the basic type of life insurance that provides financial protection for a specific time period, called the policy term and involves a fixed premium. A term insurance plan protects your family in your absence. With this type of life insurance, your family can cover expenses such as a child's fees, home loans, groceries, and more.

Benefits:

In this policy, the investment risk in investment portfolio is borne by the policyholder.

Unit Linked Insurance Plans (ULIPs) combine life insurance and investment opportunities. Besides providing life insurance cover for your loved ones, it allows you to invest a part of your premium payments in market-linked3b funds for wealth creation over time. With ULIPs, you have the ability to switch funds and take advantage of tax benefits3a on your premiums and maturity proceeds.

Based on your risk appetite, you can choose to invest in Equity, Debt, and a balanced fund option. Also, to maximise your returns from ULIP policy, you can move your investment between different funds.

Benefits:

Endowment policies provide guaranteed3c returns and life insurance protection. With an endowment plan, you can enjoy comprehensive coverage while saving regularly. Once the policy matures, the policyholder receives a lump sum. Death benefits will be payable to your nominee in the event of an unfortunate event during the policy term.

Benefits:

Money back policies are endowment assurance plans providing both life insurance and savings. In this plan, you get life insurance coverage and regular returns during the policy's term. This plan can help you save for a dream house, your child's future, and more.

Benefits:

A retirement plan is designed to ensure that individuals receive a steady income or lump sum after retirement by saving and investing funds during their working years. Having these plans gives you security and covers expenses when you don't have regular income.

With Tata AIA's retirement and pension plans, you can enjoy financial security during your golden years. These plans offer guaranteed3d income as well as flexibility to meet retirement needs. There are two types of retirement plans: one that offers fixed lifetime guaranteed income while the other provides market-linked3b growth to meet your growing needs at the time of retirement.

Benefits of fixed income retirement plan:

Benefits of market-linked3b retirement plan:

Child savings plans help you save for your child’s future needs, be it education or wedding. It also supports them financially in case of an unfortunate event where the insured parent passes away during the policy term.

Benefits:

These plans allow policyholders to participate in the profits of the company, typically through bonus and dividends. These payouts are in addition to the standard policy benefits and are optional as they depend on company’s performance.

Benefits:

Capital Guarantee Solution is a type of investment plan that combines the benefits of market-linked returns3b with the security of capital protection. The market-linked aspect provides opportunity for wealth creation with capital guarantee ensures that the initial investment is protected, which means policyholder will atleast receive the principal amount, irrespective of market performance.

Benefits:

As per definition, a whole life insurance policy provides lifelong protection. Most insurance policies offer life coverage up to 100 years3h of age. It is also referred to as permanent life insurance, as it provides financial protection for your family if you pass away. You can ensure your loved ones' financial security with this plan.

Benefits:

Annuity plans provide you with a steady, reliable income after retirement, helping you secure your financial future. With Tata AIA, you can choose between immediate and deferred annuities. You can choose to make single or regular premium payments under the policy. Upon retirement, the plan will pay out an annuity based on the mode you select.

Benefits:

Select the plan that fits your goal.

Participate in these interesting quizzes to reveal the plan that suits you the best.

Awards & Recognition

Our experts are happy to help you!

Our experts are happy to help you!

L&C/Advt/2026/Jul/4251

4eT&C apply.

L&C/Advt/2026/Jul/4147

Know about Life Insurance

Protect your loved one’s future and meet long-term goals with the right life insurance tailored to your needs.

Life insurance is a contract between two parties - an individual (the insured or policyholder) and a life insurance company (the insurer or insurance provider).

The insurance provider assures the policyholder of financial coverage for their family until the end of the policy tenure. In case of the individual’s demise, the financial protection by the insurer is extended to the insured’s family in the form of a lump sum payout or monthly income.

In the case of policies where a maturity benefit is payable, the policyholder can claim the benefits if they survive until the end of the policy tenure. These benefits, too, can be paid out as a lump sum or as regular income.

To keep the life insurance cover active, the insured pays a premium to the insurer on a monthly, quarterly, half-yearly, or annual basis. The premium amount payable is determined on the basis of various factors, including the life insurance coverage.

Life insurance plans provide financial protection to your family in case of your unfortunate and untimely death during the policy term. In return for regular premium payments, the insurance company commits to pay a fixed amount to your nominee in case of death, known as the sum assured.

For example, Parul buys a life insurance policy with a sum assured of ₹1 Crore for 20 years and pays an annual premium of ₹8,000. If the person passes away within those 20 years, the nominee receives ₹1 Crore from the insurer. This amount can help cover household expenses, pay off loans, or secure the family’s future.

If Parul survives the policy term and has chosen a plan with maturity benefits (like an endowment or money-back plan), a lump sum amount is paid at the end of the term.

Let’s understand common types of life insurance and how it works with the help of an example:

1. Term Insurance

Term insurance is a pure protection plan. It provides life cover for a specific period. If the policyholder passes away during the term, the nominee receives the sum assured. No maturity benefit is provided if the policyholder survives, unless a Return of Premium option is chosen.

Example:

Ravi buys a 30-year term insurance policy with a sum assured of ₹1 Crore. He pays an annual premium of ₹10,000. If he passes away within 30 years, the nominee receives ₹1 Crore. If he survives the term, there is no payout, unless he opted for a term plan with return of premium option.

2. Endowment Plan

An endowment plan offers life cover along with savings. The policyholder receives a lump sum amount on maturity if they survive the policy term. If they pass away during the term, the sum assured is paid to the nominee.

Example:

Neha purchases a 20-year endowment plan with a sum assured of ₹30 Lakh. She pays regular premiums during the policy term. If she passes away within 20 years, the nominee receives ₹30 Lakh. If she survives, she will receive a maturity benefit.

3. Money-Back Plan

A money-back plan provides periodic payouts during the policy term along with life cover. The policyholder receives a percentage of the sum assured at regular intervals. The remaining amount and any bonuses are paid on maturity or to the nominee in case of death.

Example:

Rahul buys a 10-year money-back plan with a 25-year income period and a sum assured of ₹15 Lakh. He shall receive a fixed income every year from the 11th year till the 35th year. If he passes away during the policy term, the nominee receives the sum assured.

4. Unit Linked Insurance Plan (ULIP)

ULIP combines life cover with investment. A part of the premium is invested in market-linked funds (equity or debt), and part is invested in life cover. The payout depends on market performance and the sum assured.

Example:

Deepak buys a 15-year ULIP with a sum assured of ₹25 Lakh. He chose to invest in a mix of equity and debt funds. If he passes away during the policy term, the nominee receives ₹25 Lakh or the prevailing fund value, whichever is higher. If he survives, he will receive the fund value based on market performance.

Here are the key advantages of a life insurance:

A life insurance plan ensures that your family will be financially secure in your absence. The life insurance coverage pays out the sum assured to your family or beneficiary if you meet an untimely demise during the policy term.

In the case of savings plans or Unit-Linked Insurance Plans, you can invest in the policy through your premium payment over the long term. This financial corpus is paid out as the maturity benefit if you outlive the policy term.

Savings plans or retirement savings plans offer guaranteed and assured returns on maturity. You can save your money over the years as you pay your premiums. On maturity, this amount can be availed of either as a lump sum or as a regular income.

Along with financial protection, life insurance offers multiple tax benefits5a. Premiums paid towards individual life insurance policies attract 0% GST. Besides this, under Section 123, Schedule XV (erstwhile Section 80C) of the Income Tax Act 2025, you can claim a tax deduction of up to ₹1.5 Lakh on the premiums paid. In addition, death benefit and maturity benefits/bonuses/loyalty additions are tax-exempt (subject to policy conditions) Section 11, Schedule II (erstwhile Section10(10D)).

If you plan to get life insurance, purchasing the policy at a younger age ensures lower premiums, owing to lower health risks. The premium amount is higher if you buy life insurance later at an older age.

Some term insurance plans offer long coverage, with some plans offering coverage up to 100 years of age5b. With this, you can ensure that you and your family are protected for your whole life.

Life insurance is important for everyone, irrespective of age, profession, and lifestyle. These are the broad categories of individuals who should have life insurance:

At a young age, when you just begin working, you can avail lower premiums. Salaried individuals with life insurance can provide extensive financial coverage for their loved ones with affordable premiums that don’t affect their other expenses.

Married couples tend to have greater financial responsibilities, such as loans for buying a new home, car, or household items. A life insurance policy with joint coverage offers protection to both partners under a single plan for better management.

Life insurance safeguards a family’s financial future if a working parent passes away unexpectedly. It ensures income for dependents, covering essentials like education, housing, and daily expenses and also helps clear any outstanding debts.

Life insurance is important for stay-at-home moms and homemakers. In case of the death of the lady of the house, the life insurance coverage should be able to help the rest of the family sustain themselves and find help to manage the home.

During your retirement years, a life insurance plan can help replace your salary. Here, retirement insurance plans can offer regular income, which makes it easier for you to take care of yourself and your family.

Starting a business venture can utilise your savings and you may also need to take out a loan. Life insurance can help you secure your business and your family’s needs so that any unpaid debts do not burden them in your absence. Additionally, the Married Women’s Property Act (MWPA) in term insurance ensures that payouts go to your intended nominee and is safeguarded from creditors.

Here’s why NRIs can buy life insurance in India.

In comparison to other countries, the overall cost of life insurance is less. NRIs can find cost-effective policies with a reputed insurer in India. Moreover, they can enjoy the same benefits.

NRIs can avail medical checkups and tests over video calls or phone calls; there is no need to make in-person visits each time. IRDAI-approved third-party facilitators in other countries provide this facility for quick and convenient policy approvals.

NRIs have access to customer support 24*7 across the globe. They can get all the required assistance, including claim settlement, anytime and anywhere, from any location.

NRIs have an option to choose the premium frequency as per their convenience – monthly, quarterly, half-yearly, annually or single-pay.

NRIs can bundle their life insurance plans with optional riders5c to make their cover more comprehensive with accidental support, critical illness cover, waiver of premium, etc

The information, provided herein, may not be treated as a solicitation request in any manner. Any decision to buy online insurance by NRIs is completely his/her choice. The insurer is permitted to solicit insurance in India and settles claim in INR only.

Calculating your life insurance coverage can be a simple process once you know more about it. Here is what you need to consider when estimating the life insurance coverage needed:

Life insurance can help cover major financial events in your life. Hence, even after you pass away, your family should be able to meet all their financial goals and fulfil their dreams. Also, decide on a coverage that will handle their smallest needs.

Your current income will decide the life insurance coverage your family needs. The coverage should be at least 10 to 20 times your annual income, depending on the financial targets. Your financial capacity is also important when it comes to making reasonable premium payments.

If you are the sole earning member of your family, your income supports your family. When you cannot provide for them, your life insurance should offer financial assistance to them at least equal to your monthly income.

Unpaid loans can reduce the life insurance coverage. Hence, it is better to pay them off as early as possible. But in the event of your death, life insurance can ensure that your family does not suffer due to the burden of these unpaid debts.

It is always preferable to set aside some life insurance coverage for future medical emergencies for your family. This will enable them to get the quality healthcare required in your absence. Also, consider future inflation rates when considering this amount.

Your life insurance cover should meet your long-term financial requirements. As you enter a new life stage, such as marriage or childbirth, it should provide adequate support in case of any unfortunate events.

These are some reasons why life insurance is a must:

A life insurance plan helps create a safety net for your loved ones. In the event of your untimely death, the sum assured can help your family manage living expenses, maintain their lifestyle, and achieve long-term financial stability.

Moreover, you can opt for a savings-oriented plan, such as an endowment plan or ULIP. It helps systematically build a corpus that can support future financial goals like buying a house or planning for retirement.

Every parent aspires to provide their child the best education and a secure future. Life insurance, particularly child education plans or savings plans, ensures that even if something happens to you or your spouse, your child’s educational needs remain protected.

The payout from a life insurance policy can fund your child’s education, extracurricular activities, and other major expenses. This provides peace of mind as their future is not compromised by life’s uncertainties.

Many families rely on loans for home purchase, education, or business needs. In the absence of the primary earner, these financial liabilities can become a major burden for the family.

Life insurance helps prevent such situations by ensuring that outstanding debts like home loans, personal loans, or education loans can be paid off using the sum assured. This keeps your family protected from additional stress and prevents legal or financial complications arising from unpaid debts.

While you may be planning for your retirement through savings or pension plans, an unexpected death can leave your spouse vulnerable, especially if they depend on your income.

With life insurance, you can ensure that your spouse has access to a retirement corpus, even in your absence. The sum assured or maturity benefits from certain plans can help them meet living expenses, healthcare costs, and other retirement needs, maintaining their financial independence.

Apart from protection, life insurance also offers tax advantages. Premiums paid towards life insurance policies qualify for tax5a deductions under Section 123, Schedule XV (erstwhile Section 80C) of the Income Tax Act 2025, up to ₹1.5 Lakh in a financial year.

Additionally, the death benefit and maturity payouts from eligible life insurance plans are tax-free under Section 11, Schedule II (erstwhile Section10(10D)). This means your family receives the entire sum assured or maturity amount without any tax deductions, creating a tax-efficient financial legacy for their future security.

The following factors can affect your life insurance premiums:

Sum assured determines the premium amounts as it will be higher if you choose a higher life cover. However, this does not mean you should opt for inadequate life insurance coverage. Select a coverage amount to help you pay manageable premiums.

Many people buy life insurance when they start working. By purchasing a policy at a young age, you can ensure affordable premium payments. Buying life insurance at an older age means higher premiums.

Life insurance premiums vary as per your gender, as men and women tend to have different health risks at different stages of their lives. For instance, women have higher longevity due to lower health risks and hence pay lower premiums for term plans.

Your medical history or any previous illnesses in your family can influence your premiums. If you still have any health conditions due to any past illnesses, it is likely that you will be paying a higher premium than someone with no medical history. Note that correct disclosure is mandatory at the time of application. Claims may get rejected in case incorrect medical history is shared during application.

People with healthy lifestyles tend to have healthier bodies and fewer illnesses. This means their life insurance premiums are also lower. But if you have smoking or drinking habits, your life insurance provider will charge a higher premium rate for you.

If you have an in-office job involving no physical risk, this factor will be considered for your premium calculation. However, your premiums will be higher if you work in high-risk jobs like mining, construction, etc.

Online and offline life insurance differ in the features they offer you. Here’s how:

Feature |

Online |

Offline |

Cost benefits - Exclusive discounts available during online purchases |

Yes |

No |

Easy comparison - Compare, buy and manage plans |

Yes |

No |

Transparency - Direct access to policy details/terms and calculators |

Yes |

No |

Ease of access - Purchase instantly from the comfort of your home |

Yes |

Yes |

Flexible planning - Tailor your plan to match individual preferences |

Yes |

Yes |

Certified support availability - IRDAI-approved assistance |

Yes |

Yes |

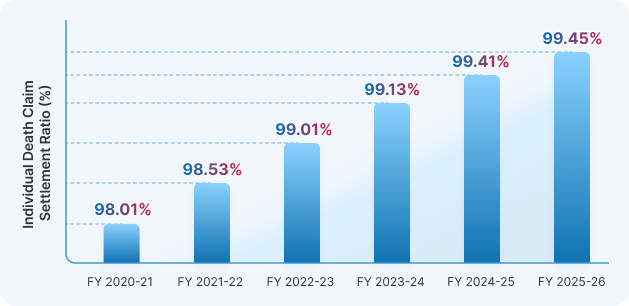

Tata AIA Life Insurance provides a stable record with 99.45% of Individual Death Claim Settlement Ratio in FY25-265d. This assures policyholders and supports their families without delay and reflects Tata AIA’s commitment to standing by customers when it matters most.

Here’s the CSR5e for the past few years:

Our Express Claim5f Service allows beneficiaries to submit claim intimation for immediate processing, helping deliver claim payouts within just four hours. This ensures faster financial support for families during critical times. 5fT&C apply.

To purchase a life insurance policy smoothly, you need to submit certain basic documents for identity, address, and financial verification.

Aadhaar card, PAN card, passport, voter ID, or driving licence.

Aadhaar card, passport, utility bill, bank statement, or rent agreement.

Birth certificate, PAN card, passport, or school leaving certificate.

Salary slips (last 3 months), Form 16, Income Tax Returns (ITR), or bank statements (last 6 months).

Required in some cases based on age, sum assured, or personal medical history.

Recent photographs as per insurer requirements.

Mandatory for high-value policies as per tax regulations.

Choosing the right life insurance plan requires careful evaluation of your financial goals, responsibilities, and long-term needs.

Consider liabilities, future goals, family expenses, and income replacement needs.

Ideally, choose a sum assured that is 10-15 times your annual income.

Select a tenure that covers your earning years or major financial responsibilities.

Evaluate affordability while ensuring sufficient coverage.

Choose an insurer with a strong claim settlement record.

Look for add-on riders5c like critical illness or accidental death benefit.

Carefully read waiting periods, exclusions, and conditions.

Buying life insurance is a simple process when you follow the correct steps and provide accurate information.

Determine coverage amount and policy type.

Review features, benefits, and premiums.

Provide accurate personal, financial, and medical details.

Upload or provide necessary KYC and income proofs.

Undergo medical tests as advised by the insurer.

Choose payment frequency (monthly, quarterly, annual).

After verification, the insurer issues the policy document.

Life insurance plans offer flexible payout options so that nominees can receive the claim amount in a way that best suits their financial needs.

The entire sum assured is paid at once to the nominee.

The nominee receives monthly or yearly income for a fixed period.

A portion is paid immediately, and the remaining amount is paid as periodic income.

The income payout increases annually at a fixed rate.

The claim amount remains with the insurer and is paid in instalments over time.

You can follow these simple steps to file a claim:

Claim Intimation

If you want to file a claim with us, you can choose any of the options below:

The Claims Department,

Tata AIA Life Insurance Company Limited,

15th Floor, Centaurus, Hiranandani Business Part,

Hiranandani Estate, Thane West, Maharashtra

Pin code - 400607

IRDA Regn. No. 110

Alternatively, you can also write to Tata AIA Life Insurance to inform us about the claim or call us. The written claim intimation should contain:

Documents Required

A few essential documents are needed to file the claim. They are:

Additional documents may be requested on a case-by-case basis submission of documents.

The claims process can only begin once all necessary documents have been submitted. When filing the claim online, upload soft copies of the documents. For offline submission, visit any of our office branches.

Claim Settlement

As per IRDAI regulations, the claim settlement timeline is 15 days from receipt of claim intimation along with mandatory documents.. However, in case of further investigations for the claim settlement, this regulatory timeline can be extended up to 45 days from the day of the claim intimation.

Though life insurance covers natural deaths and accidental deaths, here are some of the common causes of death that cannot be covered under life insurance:

Claim shall not be honoured if it is found that policy benefit is being obtained through fraud, misrepresentation or suppression of any material fact. Hence, correctly disclose all details pertaining to health, occupation, income, lifestyle habits, existing insurance etc. during policy purchase.

Inform your insurer about any pre-existing condition during the policy purchase. The benefits can only be paid out if this information is already available with the insurer.

Life insurance will not cover your death caused while involved in criminal activities.

Understanding common life insurance terms helps you make informed decisions and avoid confusion while choosing a policy. Below are the key terms explained with simple examples:

The guaranteed amount paid to the nominee if the insured person passes away during the policy term.

Example: If your policy has a sum assured of ₹50 Lakh, your nominee will receive ₹50 Lakh on your death during the policy term.

The amount you pay to keep the life insurance policy active. It can be paid monthly, quarterly, or annually.

Example: If your annual premium is ₹12,000, you must pay this amount for the defined term to maintain coverage.

The duration for which you pay the premium for your policy. It can be lesser or same as the Policy Term.

Example: If you have taken a ₹1 Cr term plan with a PPT of 10 years and PT of 30 years, it means that you need to pay premium for the 1st 10 years while your policy will continue for 30 years.

The duration for which the life insurance coverage remains active.

Example: If you buy a 30-year term plan at age 30, the coverage continues until you turn 60.

The person appointed to receive the policy benefits in case of the policyholder’s death.

Example: You can nominate your spouse or child to receive the claim amount.

The amount paid to the policyholder if they survive the policy term (applicable in endowment, money-back or return of premium plans).

Example: If you complete a 20-year endowment plan, you receive the maturity amount at the end of 20 years.

The payout made to the nominee if the insured person dies during the policy term.

Example: In a term plan, the full sum assured is paid as the death benefit.

Additional benefits that can be added to the base policy for extra protection. These riders28 are optional and you may choose basis your requirement.

Example: A critical illness rider pays a lump sum if you are diagnosed with a covered illness.

The amount paid if you voluntarily terminate certain life insurance policies before maturity.

Example: If you surrender a policy after 5 years, you may receive a reduced payout based on policy terms.

Extra time allowed to pay the premium after the due date without losing coverage.

Example: If your premium due date is 1st June, you may get up to 30 days to pay without policy lapse.

The percentage of claims settled by an insurer in a financial year.

Example: A claim settlement ratio of 98% means the insurer settled 98 out of 100 claims received.

A limited period after policy purchase during which you can cancel the policy without penalty.

Example: If you change your mind within 15 days of receiving the policy document, you can request cancellation.

A policy that continues with reduced benefits if you stop paying premiums after a specified period.

Example: If you stop paying premiums after 3 years, your coverage may continue at a lower sum assured.

The percentage of claims settled by the insurer in a year.

Example: A claim settlement ratio of 98% means that the insurer has settled 98 out of 100 claims received.

L&C/Advt/2026/Jul/4262

Frequently Asked Questions (FAQs) about Life Insurance

Life insurance ensures financial security for your family in case of your untimely death. It helps them maintain their lifestyle and meet essential expenses without facing financial hardships.

Life insurance policies can generally be purchased by individuals who are of legal age (usually 18) and able to enter legal contracts.

Yes, life insurance can be purchased online. Tata AIA offers a simple digital process where you can compare plans, get quotes, submit documents, and buy the policy from the comfort of your home. Additionally, multiple plans have additional discounts for online purchase.

Yes, when buying life insurance, you can usually choose both the policy term and the premium payment term. Generally, insurers offer flexible options, allowing you to select a term that suits your financial goals and convenience.

The right age to buy life insurance is in your 20s and 30s, when premiums are affordable and you're likely to be in good health, so you can get better coverage.

Life insurance payouts are generally not taxable in India. Death benefits are completely tax-free6a under Section 11, Schedule II (erstwhile Section10(10D)) of the Income Tax Act 2025. Additionally, maturity benefits are tax-free6a if certain conditions are met.

Life insurance premiums are payments you make to an insurance company on a regular basis to make sure your beneficiaries receive a payout upon your death or policy maturity, as applicable.

Life insurance claims can be rejected due to incomplete or false information, non-payment of premiums, involvement in illegal activities, policy exclusions, or violation of policy terms.

Yes, senior citizens can benefit from life insurance. It helps cover final expenses after retirement, repay debts, and provide financial support to loved ones. Also, if they have dependants, then a term plan will help in legacy planning.

Survival benefits depend on the policy type. Endowment, money-back plans, and ULIPs offer survival benefits, offering part of the sum assured during the term. Term insurance usually does not provide survival benefits unless it includes a return of premium option.

CSR (Claim Settlement Ratio) indicates the percentage of claims settled by an insurer every year. Tata AIA Life Insurance has maintained a consistently high CSR over the year. Its Individual Death Claim Settlement Ratio is 99.45% for FY 2025-266b.

Tata AIA Life Insurance has protected over 9.8 million (98 Lakh+) families6c across India. This shows the strong trust people have in Tata AIA for securing their family's financial future.

Tata AIA has a 99.45% Claim Settlement Ratio6b, offers fast claims within 4 hours6d, and provides a wide range of life insurance plans covering protection, savings, ULIPs, retirement, and child education needs.

6bIndividual Death Claim Settlement Ratio. 6dT&C apply.

Tata AIA offers various life insurance plans, such as term, whole life, savings plans, ULIPs, child education plans, retirement plans, and group plans to meet protection, investment, and retirement needs of customers.

Yes, Tata AIA premiums qualify for tax6a benefits under Section 11 Schedule II, Section 123 Schedule XV, Section 126 (erstwhile Section 80C, 80D,10(10D)), 115BAC and other applicable provisions of the Income Tax Act 2025.

Tata AIA offers a wide range of plans, a strong claim settlement ratio, quick claim processing, and options that cover protection, savings, investment, retirement, and child education needs.

You need term insurance to protect your family financially in case of your untimely death. It ensures they can manage daily expenses, repay debts, and meet future needs without financial stress.

Yes, term insurance is generally more affordable than other life insurance policies. It offers high life cover at low premiums because it provides only pure protection without any savings or investment component.

Term insurance is available for individuals aged 18 to 65. However, your 20s are considered the right time to buy it, as you can secure financial protection for your family at lower premiums.

Yes, you can have multiple term insurance policies. There’s no legal limit, but ensure they suit your financial goals and you can manage the premiums and policy details effectively.

Savings plans are life insurance policies that help you systematically save money while providing life cover.

Yes, there are different types of savings plans that you can choose from as per your needs:

● Money-back plans

● Endowment plans

● Guaranteed returns plan

Yes, you can simply log in on your insurance provider’s official website to access your savings policy and choose a digital payment channel to pay your premiums online in a secure manner.

Depending on your choice of savings policy, you can choose any amount for your savings corpus as per your goals. You can determine the highest savings limit. The life insurance sum assured can also be decided by you. However, while there is a minimum limit to the sum assured, the maximum limit will require your insurance provider’s approval.

You can invest in a ULIP to grow your wealth in the long-term. By investing regularly, you can benefit from the market-linked returns6e through the years and, at maturity, receive the fund value on your investment.

There are multiple funds to choose from when you invest in a ULIP. You can opt for a few or all the funds to invest in. This can help you diversify your ULIP portfolio. The type of funds will vary as per the ULIP you choose.

Yes, ULIP policies allow you to switch between funds if you are not satisfied with their performance. A certain number of fund switches are permitted free of cost each year.

One ULIP can suffice for your wealth creation goals if you plan your investment. However, over the years, if you want to invest in new funds, you can opt for a second ULIP plan. It is advisable not to go overboard with many ULIPs as these are market-linked plans and carry investment risk.

You should start planning for retirement from the day you get your first salary. Investing in instruments that beat inflation helps secure funds needed to maintain a good lifestyle after retirement.

Yes, many retirement plans, especially annuity plans, offer a regular income for life, often in exchange for a lump sum. Pension plans also provide steady income through savings or annuity purchases after retirement.

Yes, many retirement plans include life insurance, offering both retirement savings and a death benefit for beneficiaries.

You only pay the premiums towards your retirement plan and buy the annuity on your retirement. There is no need to pay a separate premium for the life insurance component if your retirement plan offers life insurance benefits.

Start planning for a child education insurance plan when your child is an infant. A child education plan aims to cover your child’s future education expenses. Once the policy matures, you can fund your child’s college education through the child investment plan.

Yes, child investment plans include life insurance benefits that secure the child’s financial future if a parent passes away. A beneficiary can be appointed to manage funds until the child turns 18.

Considering all the future educational expenses, tuition fees and course fees, determine an amount that will help meet all these costs. Also, consider the future rate of inflation so that there is no shortage of funds when it comes to fulfilling your child’s goals and dreams.

Yes, there are different types of child investment plans. Some can be market-linked plans, while others are low-risk savings plans. You can decide what type of policy you want to invest in for your child’s future.

L&C/Advt/2026/Jul/4249

Last updated on 30 Jul 2026

Disclaimers

L&C/Advt/2026/Jul/4466

L&C/Advt/2026/Jul/4465

L&C/Advt/2026/Jul/4251

L&C/Advt/2026/Jul/4147

L&C/Advt/2026/Jul/4262

L&C/Advt/2026/Jul/4249