FOR EXISTING POLICY

FOR EXISTING POLICY

Call us

Call us

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Tata AIA

Up to 18.5% discount (1st year)** | 99.13% Individual Death Claim Settlement Ratio6

Are you an NRI?

Tata AIA

Get guaranteed11 income and save tax~ up to Rs 46,800++ | 11T&C apply

Are you an NRI?

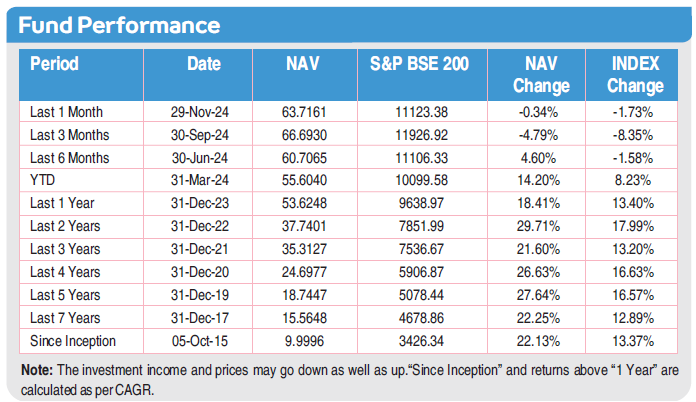

In this policy, the investment risk in investment portfolio is borne by the policy holder. The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year. 5Data as of December 31, 2024. Past performance is not indicative of future performance. • Fund Benchmark: Multi Cap Fund – S&P BSE 200 | SFIN: Multi Cap Fund – ULIF 060 15/07/14 MCF 110 | Inception Dates: Multi Cap Fund: 05 Oct 2015.

This advertisement is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Vitality Protect Advance - A Non-Linked, Non- Participating Individual Health Product (UIN: 110N178V01).

Multi Cap fund delivered 27.64% Returns (Benchmark:16.57%)5

Are you an NRI?

Tata AIA

Retirement is the time to live every moment fikar-free, which is only possible when you have a sound financial plan.

Are you an NRI?

Tata AIA

Up to 18.5% discount (1st year)** | 99.13% Individual Death Claim Settlement Ratio6

Are you an NRI?

Tata AIA

Get guaranteed11 income and save tax~ up to Rs 46,800++

Are you an NRI?

In this policy, the investment risk in investment portfolio is borne by the policy holder. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year. 5Data as of December 31, 2024. Past performance is not indicative of future performance. • Fund Benchmark: Multi Cap Fund – S&P BSE 200 | SFIN: Multi Cap Fund – ULIF 060 15/07/14 MCF 110 | Inception Dates: Multi Cap Fund: 05 Oct 2015

This advertisement is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Vitality Protect Advance - A Non-Linked, Non- Participating Individual Health Product (UIN: 110N178V01).

Multi Cap fund delivered 27.64% Returns (Benchmark:16.57%)5

Are you an NRI?

Tata AIA

Retirement is the time to live every moment fikar-free, which is only possible when you have a sound financial plan.

Are you an NRI?

Life Insurance is a formal agreement between you and an insurance company. Here, the company agrees to provide a specified "sum to" Read more designated beneficiaries upon the insured person's passing. The policyholder needs to pay regular premiums to maintain coverage. In exchange for these premium payments, the policyholder secures protection for their family.

Some policies may provide additional benefits, such as payments in case of serious illness or potential returns at the end of your contract term. These policies help secure your family by providing required finances during difficult times and allow them to stay financially stable once you pass away.Read Less

Life Insurance is a formal agreement between you and an insurance company. Here, the company agrees to provide a specified "sum to" Read more designated beneficiaries upon the insured person's passing. The policyholder needs to pay regular premiums to maintain coverage. In exchange for these premium payments, the policyholder secures protection for their family.

Some policies may provide additional benefits, such as payments in case of serious illness or potential returns at the end of your contract term. These policies help secure your family by providing required finances during difficult times and allow them to stay financially stable once you pass away.Read Less

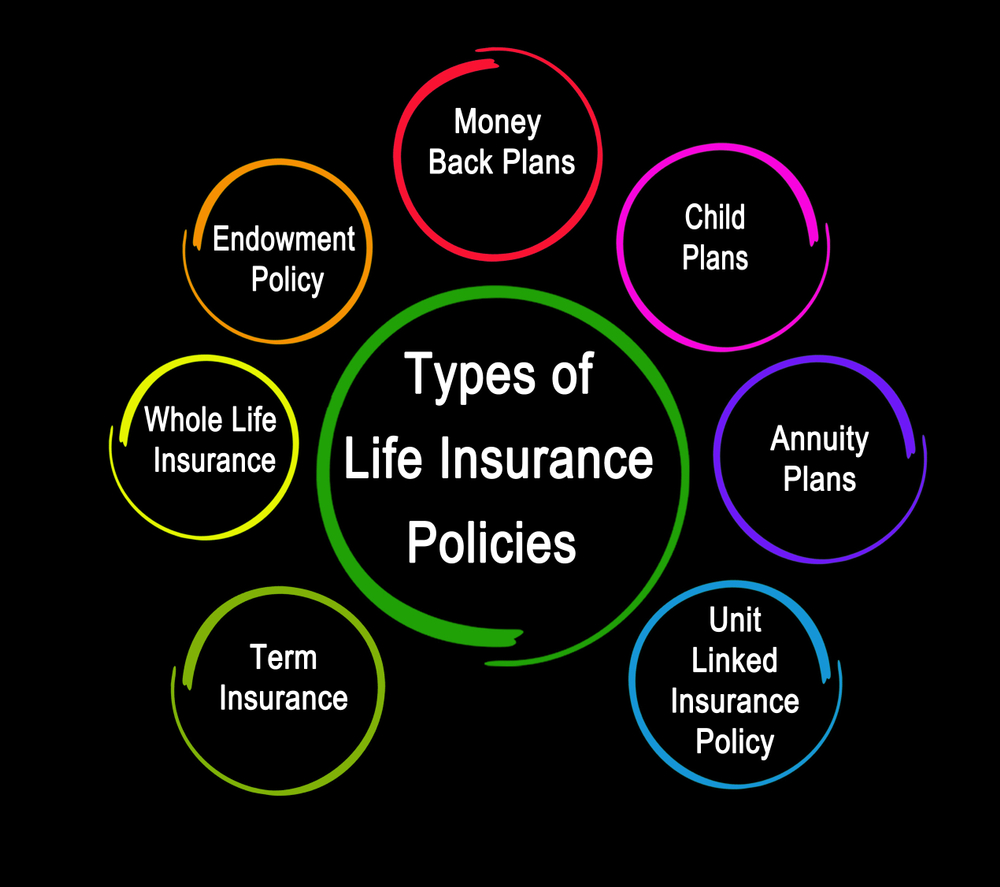

Types of Life Insurance

View all plansA term insurance plan helps you secure the future of your loved ones and shields your family from uncertainties in life. With a term insurance plan, one can get a large life cover (Sum Assured) at a lower premium. In case of an unfortunate event such as the death of the life assured in your family, the nominee is paid the sum assured as pre-defined in the policy.

Provides Life Cover against uncertainties of Life

Get Tax Benefits~ as per applicable tax laws

Savings plans are insurance plans that combine the benefits of protection and savings. Savings plans allow you to save money over the policy term while simultaneously offering you the benefits of protection. This means you get to give your family the gift of financial security to live a fikar-free life.

With a savings plan, you can get guaranteed^^ returns as a maturity benefit pay-out. This will help you accomplish your financial goals with the benefit of life insurance policy. ^^T&C apply

You can increase the coverage of your policy by adding additional riders to get the complete policy coverage.

In this policy, the investment risk in investment portfolio is borne by the policyholder.

ULIPs (Unit Linked Insurance Plans) offer the benefit of life cover along with market-linked returns5. You can accomplish your dream goal such as buying a house, saving for child’s education or early retirement. Basis your risk appetite, you can choose to invest in High, Medium, and Low-risk investment options and pay ULIP policy premiums easily.

Get Tax benefits~ as per applicable

tax laws

Basis your risk appetite, you can choose

to invest in Equity, Debt, and balanced fund

options. Also, to maximize your returns from

ULIP policy, you can move your investment

between different funds.

Tata AIA Retirement plans are insurance plans that are tailor-made to give you financial independence during the golden years of your life. These policies help you secure your future, fulfil your family dreams and financial goals, and live a worry-free life after you have retired.

Live a worry-free life with investments that provide you a regular income. A well-diversified financial portfolio will give you higher returns during your retirement.

You may be at the peak of your professional life right now. But after a long and successful career, you will no doubt look forward to a comfortable post-retirement life with financial stability. Tata AIA retirement plans can help you realize this your financial ambition.$T&C apply

A term insurance plan helps you secure the future of your loved ones and shields your family from uncertainties in life. With a term insurance plan, one can get a large life cover (Sum Assured) at a lower premium. In case of an unfortunate event such as the death of the life assured in your family, the nominee is paid the sum assured as pre-defined in the policy.

Provides Life Cover against uncertainties of Life

Get Tax Benefits~ as per applicable tax laws

Savings plans are insurance plans that combine the benefits of protection and savings. Savings plans allow you to save money over the policy term while simultaneously offering you the benefits of protection. This means you get to give your family the gift of financial security to live a fikar-free life.

With a savings plan, you can get guaranteed^^ returns as a maturity benefit pay-out. This will help you accomplish your financial goals with the benefit of life insurance policy. ^^T&C apply

You can increase the coverage of your policy by adding additional riders to get the complete policy coverage.

In this policy, the investment risk in investment portfolio is borne by the policyholder.

ULIPs (Unit Linked Insurance Plans) are life insurance plans that offer the benefit of life cover along with market-linked returns5. You can accomplish your dream goal such as buying a house, saving for child’s education or early retirement. Basis your risk appetite, you can choose to invest in High, Medium, and Low-risk investment options and pay ULIP policy premiums easily.

Get Tax benefits~ as per applicable tax laws

Basis your risk appetite, you can choose to invest in Equity, Debt, and balanced fund options. Also, to maximize your returns from ULIP policy, you can move your investment between different funds.

Tata AIA Retirement plans are insurance plans that are tailor-made to give you financial independence during the golden years of your life. These policies help you secure your future, fulfil your family dreams and financial goals, and live a worry-free life after you have retired.

Live a worry-free life with investments that provide you a regular income. A well-diversified financial portfolio will give you higher returns during your retirement.

You may be at the peak of your professional life right now. But after a long and successful career, you will no doubt look forward to a comfortable post-retirement life with financial stability. Tata AIA retirement plans can help you realize this your financial ambition.$T&C apply

Our experts are happy to help you!

What is Life Insurance?

Life insurance is a contract between two parties - an individual (the insured or policyholder) and a life insurance company (the insurer or insurance provider).

The insurance provider assures the policyholder of financial coverage for their family until the end of the policy tenure. In case of the individual’s demise, the financial protection by the insurer is extended to the insured’s family in the form of a lump sum payout or monthly income.

In the case of policies where a maturity benefit is payable, the policyholder can claim the benefits if they survive until the end of the policy tenure. These benefits, too, can be paid out as a lump sum or as regular income.

To keep the life insurance cover active, the insured pays a premium to the insurer on a monthly, quarterly, half-yearly, or annual basis. The premium amount payable is determined on the basis of various factors, including the life insurance coverage.

How does Life Insurance Work?

Life insurance secures the financial needs of your family and ensures their well-being in case of your untimely demise.

To keep the life insurance coverage active, you need to make the premium payments towards the policy as per the selected. However, there are different types of life insurance policies, and they all serve different purposes.

Term insurance is the simplest form of life insurance. Under a term plan, your family will be protected by a pure life cover and will receive death benefits in case of your death. After the benefits are paid out, the life cover will be terminated.

Life insurance policies like savings plans comprise long-term savings as well as life insurance. With a money-back plan, endowment plan, or guaranteed returns plan, a maturity benefit is payable when the policy matures. However, this is subject to your survival until then.

Similarly, Unit-Linked Insurance Plans combine life insurance with investment. You can choose a ULIP as per your risk appetite and investment goals. During the policy term, you invest in the funds under the policy, and on maturity, you can earn market-linked returns5 from your investment.

A life insurance plan allows you to choose from flexible policy terms, premium paying terms, and a mode, as per your needs and convenience. The policy term determines how many years your life insurance plan will offer coverage to your family. The premium paying term can be chosen for the number of years you want to pay your premiums. You can also pay a one-time lump sum as the premium if you want to avoid paying monthly/yearly premiums.

Life insurance does not always cover deaths caused due to specific illnesses, injuries, and accidents. These riders cover a range of unforeseen risks like hospitalisation costs, critical illnesses, accidental death and disability, and more. The riders come at an additional but nominal cost and cannot be purchased unless you have a valid life insurance policy.

There are also some exceptions and exclusions under life insurance. Before purchasing a life insurance policy, it is advisable to understand these exclusions so that you can get the most out of your life insurance policy.

Get personalized guidance to choose the best-fit insurance plan for your specific needs.

Get personalized guidance to choose the best-fit insurance plan for your specific needs.

Here are the important reasons why you must have life insurance:

A life insurance plan ensures that your family will be financially secure in your absence. The life insurance coverage pays out the sum assured to your family or beneficiary if you meet an untimely demise during the policy term.

In the case of savings plans or Unit-Linked Insurance Plans, you can invest in the policy through your premium payment over the long term. This financial corpus is paid out as the maturity benefit if you outlive the policy term.

Savings plans or retirement savings plans offer guaranteed and assured returns on maturity. You can save your money over the years as you pay your premiums. On maturity, this amount can be availed of either as a lump sum or as a regular income.

Under Section 80C of the Income Tax Act, you can claim a tax deduction of up to ₹ 1.5 Lakh on the paid premiums. The death benefits and maturity benefits/bonuses/loyalty additions (subject to policy conditions) are tax-exempt under Section 10(10D).

If you plan to get life insurance, purchasing the policy at a younger age ensures lower premiums, owing to lower health risks. The premium amount is higher if you buy life insurance later at an older age.

Some term insurance plans offer a long coverage, with some plans offer cover up to 100 years of age. With this, you can ensure that you and your family are protected for your whole life.

Need help to choose the right plan?

Need help to choose the right plan?

I have a query on my policy

Log In

I want to buy a new policy online

Pay Premium Online

If you are an existing policy holder,

you can quickly pay your premium online here!

Life insurance is important for everyone, irrespective of age, profession, and lifestyle. These are the broad categories of individuals who should have life insurance:

Calculating your life insurance coverage can be a detailed but simple process once you know more about it. Here is what you need to consider when computing the life insurance coverage needed:

Life insurance can help cover major financial events in your life. Hence, even when you are not around, your family should be able to meet all their goals and fulfil their dreams. Also decide on a coverage that will handle their smallest needs.

Your current income will decide the life insurance coverage your family needs. The coverage should be at least 10 to 20 times your annual income. Your financial capacity is also important when it comes to making reasonable premium payments.

If you are the sole earning member of your family, your income supports your family. When you cannot provide for them, your life insurance should offer financial assistance to them at least equal to your monthly income.

Unpaid loans can eat into life insurance coverage. Hence, it is better to pay them off as early as possible. But in the event of your death, life insurance can ensure that your family does not suffer under the burden of these unpaid debts.

It is always prudent to set aside some life insurance coverage for future medical emergencies for your family. This will enable them to get the quality healthcare required in your absence. Also, consider future inflation rates when considering this amount.

Your life insurance cover should meet your long-term financial requirements. With change in life stage such as marriage or childbirth it should provide adequate support in case of any unfortunate events.

These are some reasons why life insurance is a must:

Long-term financial stability

Your life insurance plan helps create a financial corpus for your family’s future financial security. With a savings plan, you can plan early and save enough for the future to meet your financial goals.

Secure your child's future

Be it a child education plan or a savings plan, life insurance can help you secure your child’s future needs. And in case of your death or your spouse’s death, your child will still be able to realise their dreams.

Financial liabilities

Loan repayments can be a hassle, and non-repayment can lead to bad credit and increase the chances of earning a penalty fee. In your absence, you can keep your family away from the risk of unpaid debts with a life insurance plan.

Spouse’s retirement

A planned retirement helps you meet various needs. But in your absence, your spouse should not be deprived of a retirement plan in your absence. With life insurance, you can secure a retirement corpus for their future needs.

Tax benefits

You can claim tax deductions under Section 80C of the Income Tax Act on your policy premiums. And since the death benefits, too, are tax-exempt under Section 10(10D), your family can inherit a tax-free legacy for their security.

The following factors can affect your life insurance premiums:

The sum assured

Your age

Your gender

Medical history

Lifestyle habits

Your occupation

You can follow these simple steps to file a claim:

Claim intimation

Write to Tata AIA Life Insurance to inform us about the claim or call us. The written claim intimation should contain:

the policy number

the insured’s name

the date and place of death

the cause of death

the claimant's name

Alternatively, you can also file the claim offline, at any of our office branches.

Documents required

A few essential documents are needed to file the claim. They are:

The claimant's statement

original policy document

death certificate

police FIR

post-mortem exam report in case of an accidental death

certificate and records from the hospital

advance discharge form

There may be a requirement for additional documents.

Submission of documents

The claims process can only begin once all necessary documents have been submitted. When filing the claim online, upload soft copies of the documents. For offline submission, visit any of our office branches.

Claim settlement

As per IRDAI regulations, the claim settlement timeline is 30 days from receiving all the documents, including any clarifications from our end. However, in case of further investigations for the claim settlement, this regulatory timeline can be extended up to 90 days from the day of the claim intimation.

Though life insurance covers natural deaths and accidental deaths, here are some of the common causes of death that cannot be covered under life insurance:

Life insurance will not cover your death caused by your involvement in illegal or criminal activities. Also, death caused by high-risk sports will not be covered.

Inform your insurer about any pre-existing condition during the policy purchase. The benefits can only be paid out if this information is already available with the insurer.

The use and overdose of drugs and alcohol can lead to death. But your life insurance policy cannot cover this type of death.

Life insurance cannot cover damages to the insured’s life arising from natural disasters or calamities.

We combine Tata Group’s unrivalled brand strength and leadership position in India, and AIA’s expertise and presence in 18 markets across the Asia-Pacific region. As pre-eminent protection providers, we offer customized solutions that enable consumers to protect the smiles of their loved ones family members.

Voice of Happy Customers

Why should you have life insurance?

Having life insurance serves many purposes. If you need pure life cover, you can get a term insurance plan and secure your family against financial insecurities. With a savings plan or money-back plan, you can save money over the long term and fulfil your future financial goals. Or you can choose wealth generation + life cover and earn market-linked returns through a Unit-Linked Insurance Plan.

When can you purchase a life insurance policy?

You can purchase life insurance at any stage of your life when you need to offer life insurance coverage to your family and fulfil your financial commitments.

However, if you buy life insurance at a younger age, you can pay lower premiums. Conversely, buying life insurance at an older age means higher premiums.

The maximum age limit up to which you can buy life insurance is 65 years.

Can life insurance be purchased online?

Yes, you can buy life insurance online. You can purchase a policy of your choice by browsing any Tata AIA Life Insurance plans online. Alternatively, you can also get in touch with us to know more about your policy choice.

Can I choose the policy term and premium payment term when buying life insurance?

Yes, you can choose a policy term and premium paying term per your preference before buying life insurance. This can help you pay your policy premiums at your convenience.

What is a life insurance premium?

A life insurance premium is the amount of money that you pay regularly (monthly, quarterly, annually) for a set tenure so that your life insurance policy remains active. In case something happens to you, your loved ones will be financially protected with the death benefit. The amount you pay depends on your age, health, and the type of policy you choose.

Do I get survival benefits under my life insurance policy?

Whether you receive survival benefits depends on your specific life insurance policy. These benefits are not offered in all plans. Review your policy documents or contact your insurer to determine if your plan includes survival benefits.

Why do you need term insurance?

Different policyholders need term insurance for individual reasons. Term insurance is primarily used to secure your family’s financial future in your absence. However, you can also use a term plan with adequate coverage for many other reasons if you meet your demise within the policy term.

The sum assured can protect your family from unpaid loans and debts, create a retirement fund for your spouse, set up a charitable trust fund for your family or underprivileged children, and so on.

Is term insurance more affordable than other life insurance policies?

Yes, term insurance is more affordable than other forms of life insurance. This is because term plans only offer a pure life cover which can be as extensive as your needs. In the event of your untimely demise during the policy term, the policy will offer your beneficiary/family a death benefit sum assured and then the policy will cease to offer any benefits. Since there are no other components under term insurance, the premiums are also quite low.

Which is the best age to buy a term insurance plan?

You can have a term insurance policy at any age if you need life insurance for yourself and your family. However, buying a term plan when young can ensure lower premium payments due to the lower health risks related to youth.

Getting a term insurance plan early also means a longer policy tenure and more years of life insurance coverage for your family’s protection.

Can I have more than one term policy?

Yes, you can have more than one term insurance policy. However, it is advisable to have one policy with adequate life insurance coverage than multiple policies. This is because the premium payments for two or three policies can become a financial burden over the years.

Moreover, keeping track of so many premium payment due dates is a hassle. However, with one term plan and probably a few essential, optional riders, you can provide comprehensive protection to your family.

What are savings plans?

Savings plans are a form of life insurance that helps you save money over the long term while securing your family with a life cover. You can get the savings corpus as a maturity benefit when the policy matures if you outlive the policy term. This corpus can help you fulfil your future financial commitments and goals.

On the other hand, in case of your death during the policy term, your family will receive the death benefit from the life cover. This sum assured will keep them financially secure in your absence.

Are there different types of savings plans?

Yes, there are different types of savings plans that you can choose from as per your needs:

Can I pay my premiums online toward my life insurance savings plan?

Yes, you can simply log in on your insurance provider’s official website to access your savings policy and choose a digital payment channel to pay your premiums online in a secure manner.

What is the highest limit I can choose for my savings?

Depending on your choice of savings policy, you can choose any amount for your savings corpus per your goals. You can determine the highest savings limit. The life insurance sum assured can also be decided by you. However, while there is a minimum limit to the sum assured, the maximum limit will require your insurance provider’s approval.

Why should one invest in a Unit-Linked Insurance Plan?

You can invest in a ULIP to grow your wealth long-term. By investing regularly, you can benefit from the market-linked returns5 through the years and, at maturity, receive the fund value on your investment.

Can I opt for more than one fund in a ULIP?

There are multiple funds to choose from when you invest in a ULIP. You can opt for a few or all the funds to invest in. This can help you diversify your ULIP portfolio. The type of funds will vary as per the ULIP you choose.

Is it possible to switch between funds?

If you are not satisfied with the performance of certain funds, you are allowed to make a certain number of free fund switches during the year. You can move your money to other funds available under the ULIP policy to improve your fund performance.

How many ULIPs are needed for wealth creation?

One ULIP can suffice for your wealth creation goals if you plan your investment. However, over the years, if you want to invest in new funds, you can opt for a second ULIP plan. It is advisable not to go overboard with many ULIPs as these are market-linked plans and carry investment risk.

When should I plan my retirement?

Retirement planning should start at least 10-20 years before your retirement. This will enable you to accumulate and save enough funds for all your post-retirement needs.

Can I get a regular income with a retirement plan?

Yes, you can opt for a retirement plan that offers regular income. Once you retire, you can buy an annuity plan with the investment. This annuity plan will pay out a monthly income to you. This can help you fulfil all your essential needs and meet any planned future goals after retirement.

Do retirement plans offer life insurance?

If you select a life insurance retirement plan, you can get a life cover for your family. Hence, in case of your death after retirement, your family can still be secured with the sum assured from life insurance.

Do I need to pay separate premiums for life insurance?

You only pay the premiums towards your retirement plan and buy the annuity on your retirement. There is no need to pay a separate premium for the life insurance component if your retirement plan offers life insurance benefits.

When should I get a child education insurance plan?

Start planning for a child education insurance plan when your child is an infant. A child education plan aims to cover your child’s future education expenses. Once the policy matures, you can fund your child’s college education through the child investment plan.

Does a child investment plan offer life insurance?

Yes, a child investment plan offers life insurance benefits. If the insured parent or both parents pass away, the death benefits will ensure the child’s financial future is secure. If the child is a minor at the time of their parents’ death, a beneficiary should be appointed in advance, who can manage the funds on behalf of the child until they reach 18 years of age.

How much should I invest in a child insurance plan?

Considering all the future educational expenses, tuition fees and course fees, determine an amount that will help meet all these costs. Also, consider the future rate of inflation so that there is no shortage of funds when it comes to fulfilling your child’s goals and dreams.

Are there different child investment plans?

Yes, there are different types of child investment plans. Some can be market-linked plans, while others are low-risk savings plans. You can decide what type of policy you want to invest in for your child’s future.

Disclaimers

For ULIP products