Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Share

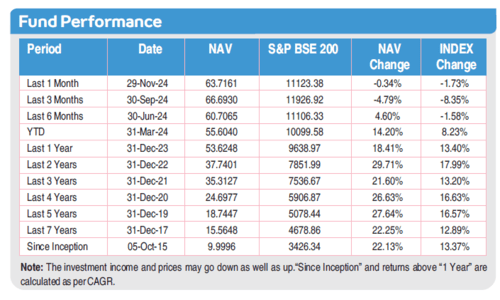

A 10-year ULIP offers life coverage and investment benefits. You can invest your premiums in various market-linked2 funds like equity, debt, or hybrid options. The plan helps you accumulate a significant corpus to achieve your important long-term financial goals. Your family receives financial security through life coverage if unforeseen circumstances occur during the policy tenure. Additionally, you can select the sum assured based on your Human Life Value (HLV) and your family’s needs. The policy allows fund switches to adjust your investment strategy according to changing market conditions. Market performance determines the growth of your investment and the potential returns over the period of ten years.

Let’s understand how a 10-year ULIP plan works with the help of an example.

Consider Rajesh, a 35-year-old IT professional who wants to fund his daughter’s overseas education goals. He calculates that he needs approximately ₹50 Lakh in ten years for her studies abroad.

Rajesh invests ₹2 Lakh annually in a 10-year ULIP to build this education fund systematically. He allocates 70% to equity funds for growth potential and 30% to debt funds for stability. Using a ULIP calculator, Rajesh estimates his fund value will reach his target through consistent investments. He pays annual premiums and claims tax3 deductions under Section 80C of the Income Tax Act. By the time his daughter completes school, Rajesh’s ULIP has grown to support her educational dreams. Additionally, the life cover helps ensure his daughter’s education is funded even in the case of his untimely demise.

A 10-year ULIP policy supports both protection and investment goals by combining disciplined savings with market-linked2 growth opportunities.

Life coverage protection

A ULIP policy provides life insurance coverage along with investment benefits. In case of an unforeseen event, the nominee receives the policy benefits, ensuring financial support for dependents during uncertain situations.

Market-linked growth

ULIPs invest in market instruments2 such as equity and debt funds. Over a 10-year period, these investments have the potential to grow based on market performance, helping policyholders build a financial corpus gradually.

Investment flexibility

ULIPs offer flexibility to switch between different fund options based on changing financial goals or market conditions. This allows policyholders to adjust their investment strategy without affecting the overall policy structure.

Tax advantages

The premium you pay is eligible for tax deduction under Section 80C of the Income Tax3 Act 1961. Additionally, the maturity proceeds are exempted under Section 10(10D) if all the conditions are met. For all the ULIP plans, irrespective of the premium amount or policy terms, the death benefit is exempt.

Long-term wealth building

Long investment periods deliver potential returns due to the compounding effect and market cycle averaging throughout the tenure. A 10-year ULIP provides sufficient time to build a substantial corpus for important life goals.

Invest more, get more!

Invest ₹5,000/month and get ₹56 Lakh. Invest ₹10,000/month and get ₹1.13 Crore. Invest ₹15,000/month and get ₹1.69 Crore. Invest ₹20,000/month and get ₹2.27 Crore.

The following are important factors that affect ULIP performance over ten years:

Market cycles and performance

Market movements in the equity and debt segments directly impact your ULIP returns throughout the entire investment tenure. Strong market performance leads to high returns, while downturns can temporarily reduce your investment value negatively. However, ten years often provide enough time to average out short-term market volatility and deliver growth.

Your fund choices

Equity funds offer higher growth potential but come with increased risk and market volatility exposure. Debt funds provide stability and moderate returns with lower risk, which may be suitable for conservative investors. Balanced funds combine both asset types to offer growth along with reasonable stability for returns.

Policy charges

Premium allocation charges, fund management fees, and mortality charges reduce your overall investment returns over time. These costs are high in early policy years but become less as your corpus grows. Understanding the charge structure may help you select plans with reasonable fees.

Fund switching strategy

Switching funds helps in optimizing your return from ULIP in various market conditions and life stages. You may rebalance between equity and debt if your goals, risk appetite, or market changes substantially. Regular portfolio review and timely switches may help you protect your gains and manage risk throughout the investment journey.

Compounding and discipline

Staying invested for the complete term allows compounding to multiply your wealth over the decade significantly. Consistent premium payments and patience through market ups and downs can enhance your final corpus value effectively. Even moderate returns grow substantially when reinvested year after year for ten complete investment years.

Tata AIA Life Insurance has an Individual Death Claim Settlement Ratio (CSR) of 99.14% for the financial year 2024-25. This reflects the company’s commitment to timely claim settlements when your family needs it most.

| CAGR | Interest Earned (in ₹) | Actual Value of Investment (in ₹) | Investment Type | Risk Level |

|---|---|---|---|---|

8% | ₹ 11,58,925 | ₹ 21,58,925 | Debt Funds | Low |

10% | ₹ 15,93,742 | ₹ 25,93,742 | Balanced Funds | Moderate |

12% | ₹ 21,05,848 | ₹ 31,05,848 | Equity Funds | High |

Note: The above figures are based on assumed growth rates for illustration purposes only. Actual ULIP returns may vary depending on market performance, fund selection, premium consistency, and applicable policy charges and are not guaranteed1. Investors may use these estimates as a reference for planning financial goals, reviewing their portfolio periodically, and maintaining disciplined, goal-based investing over the long term.

Here is how 10-year ULIP policy return rates are calculated:

Step 1: Premium allocation to funds

Your premium amount gets allocated to chosen fund units after deducting applicable policy charges and fees. You can select equity funds, debt funds, or a mix of both based on risk appetite. Fund switching is allowed during the policy term to adjust allocation according to market performance changes.

Step 2: Daily NAV calculation

Net Asset Value is the price of one unit of a particular fund at any given time. The NAV varies each day with market performance and is determined by: NAV = (Market Value of Assets - Liabilities) / Total Outstanding Units. Liabilities include various policy expenses, charges, and fund management fees deducted from total assets.

Step 3: Return calculation using CAGR

The compound annual growth rate method computes your average annual return over the ten-year investment period. CAGR Formula = [(Current NAV / Initial NAV) ^ (1 / Number of Years) - 1] × 100. Current NAV is the fund value at the end of ten years. Initial NAV is the fund value on your policy purchase date.

Step 4: ULIP policy flexibility

You can choose between a single premium or a regular premium according to your financial situation. You have the option to make top-up payments anytime during the tenure to increase the investment amount. Also, partial withdrawals are allowed after completion of the mandatory five-year lock-in period.

The following are some ways to maximise your ULIP returns in last 10 years.

Begin your investment early: Starting early provides more time to grow and capitalise on the compounding effect significantly. Early investment helps you accumulate a significant corpus even with small premium amounts over the decade.

Select appropriate funds: Choose funds based on your risk tolerance and long-term financial goal. Investors with high-risk tolerance may opt for equity funds, while conservative investors may choose debt or balanced fund options.

Review and rebalance regularly: Monitor your fund performance regularly and switch between options when market conditions change or goals evolve. Timely fund switching helps you protect capital during market downturns.

Understand policy charges: Compare different ULIP plans and select one with reasonable and transparent fees. Lower charges mean more of your premium gets invested, resulting in potentially higher final 10 years ULIP returns.

Maintain long-term discipline: Stay invested for the complete ten-year period to benefit from compounding. Withdrawing early reduces your returns and disrupts the wealth creation process significantly over the investment period.

Want to buy a new plan? Our experts are happy to help you!

A 10-year ULIP is an effective way to build wealth while protecting your family’s financial future. Combining the dual benefit of market-linked2 growth potential with life insurance coverage, it helps in meeting your long-term financial goals. The right fund selection, discipline, and periodic monitoring are all important parameters for maximising returns over the decade. Understanding how charges, market cycles, and compounding work together enables sound investment decisions for optimal outcomes. Consider your risk tolerance and financial goals before investing in a 10-year ULIP plan.

A joint venture between Tata Sons Pvt. Ltd. and AIA Group Ltd. (AIA), Tata AIA Life Insurance is one of the leading life insurance providers in India. We post everything you need to know about life insurance, tax savings and a variety of lateral topics such as savings and investments in this space. You can access and read a host of different blogs, articles and pages at the Tata AIA Life Insurance Knowledge Center or get in touch with us with any queries or questions!

Key Takeaways

Need assistance in choosing the right insurance plan?

Get Flexibility to Choose from 10+ Fund Options with our ULIP

Our experts are happy to help you!

1.

Yes, you can withdraw after the 5-year lock-in period, but early withdrawals may result in reduced long-term growth.

2.

ULIP returns fluctuate with market movement. Strong markets generally boost growth, while weak phases reduce performance. Long-term holding usually smooths short-term volatility.

3.

ULIPs can support long-term needs like education or retirement, but estimating the required contribution through a ULIP calculator helps align your goals and expectations.

4.

Past ULIP results offer useful guidance; however, they cannot assure future outcomes. Regular reviews and timely fund switches may help you align the plan with your goals and risk tolerance.

5.

Some equity-oriented ULIPs have provided substantial long-term gains, but the results depend upon the fund chosen, market cycles, and regular investing.

6.

You can follow your ULIP through NAV updates, fund reports, and online dashboards. Periodic monitoring of fund allocation and charges can support better decision-making.

7.

ULIP maturity proceeds may be exempt under Section 10(10D) if policy conditions are met, as per prevailing tax3 laws and eligibility.