Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

A 10-year investment plan is a structured way to build wealth over a 10 year time frame. This time frame suits people who want steady growth while... Read more keeping some funds available for medium-term goals. Common goals include a child’s higher studies, a home down payment, retirement savings, or a safety fund for future needs. Investors can choose a suitable 10 based on personal goals and risk appetite. Read Less

Buy Your Investment Plan

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Success

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Failure

Your details could not be saved.

Please try again.

A 10 years investment plan involves investing funds in selected financial instruments for a fixed period of ten years with the objective of generating returns. Common options include mutual funds, insurance-linked plans, fixed deposits, equity-linked savings schemes, and government-backed savings products. This duration falls between short-term investments and very long-term commitments. It provides sufficient time for investments to manage market fluctuations while keeping financial goals practical and within an achievable time frame.

Example:

Rajesh, age 35, plans funds for his daughter’s college course after ten years. He invests ₹15,000 each month in a balanced mutual fund with an assumed annual return near 10%. His total contribution of ₹18 lakh could grow close to ₹30.7 lakh by the end of the period. This covers rising education costs while ensuring the investment value grows over time.

A 10-year investment plan works on a simple investment approach. You invest money once or in regular intervals, and it is allocated across suitable options like mutual funds, bonds, equities, or a mix of these, depending on your goals and risk profile.

The returns earned are reinvested. This allows compounding to work and helps your investment grow over time. Staying invested for the full 10 years is important, as it reduces the impact of short-term market movements.

Regular investing also helps bring discipline. It smoothens market ups and downs and supports long-term wealth creation. In the end, the accumulated value can be used to meet your financial goal or reinvested further, based on your needs at that time.

You should opt for a 10 year investment plan as it offers the following benefits.

A ten-year period gives enough time for market recovery after short downturns while keeping financial goals within a defined timeline. Investors stay focused without feeling bound to very long commitments. This balance supports steady growth without creating pressure for quick results.

Certain investment plans provide tax deductions on contributions or tax-free2 maturity value. These savings reduce yearly tax burden while keeping more funds invested, which supports a higher accumulated value over the full holding period. Tax planning also brings better clarity in long-term cash flow planning.

Fixed monthly or yearly contributions build a steady savings pattern. This routine reduces unnecessary spending and builds consistency. This supports better financial discipline across changing income levels and lifestyle demands. Over time, this habit strengthens financial confidence and control.

Many investment plans permit partial withdrawals or loan facilities against accumulated value. This feature allows access to funds during urgent situations without affecting the entire investment journey or closing the plan early. It supports peace of mind during uncertain financial periods.

The ten-year period allows higher growth exposure in early years, followed by a gradual movement toward stable assets closer to maturity. This balance protects gains while still supporting reasonable growth potential. It also reduces stress caused by short market swings.

A decade is long enough to build meaningful funds while still keeping the goal clearly visible. This clarity supports motivation, progress tracking, and timely adjustments based on income changes or life priorities. It keeps financial planning structured and purposeful.

Medium-term holding reduces the impact of short market swings. Returns tend to smooth out across market cycles, supporting steady accumulation. It also helps avoid reacting to short-term price movements. This supports building confidence in decisions for long-term planning.

Ten years allows better forecasting of income flow, expenses, plus future funding needs. This clarity supports structured budgeting while aligning investments with family responsibilities and long-term financial commitments. It also supports better coordination between savings and lifestyle planning.

The rate of returns a 10-year investment plan depends on several factors. They include type of product selected, market movement, interest rate levels, and the behaviour of underlying assets. Since the funds stay invested for a long period, compounding plays a key role, where returns get reinvested and continue to build value over time. Fixed-income options, such as fixed deposits, follow predetermined interest rates, while market-linked investments depend on price movement and overall market performance. Periodic review of the investment helps maintain alignment with financial goals and changing market conditions.

Here's how you can choose the best investment plan for 10 years.

A 10-year investment plan supports medium-term financial goals through steady saving and proper asset selection. The ten years duration gives compounding enough time to enhance. Consistent contributions, periodic review, and sensible risk balance help build a healthy corpus for important life goals. Clear goal setting and disciplined monitoring further support stable progress throughout the investment period.

1.

The best 10 years investment plan depends on personal goals, risk comfort, tax planning needs, and expected liquidity. Different options include mutual funds, fixed deposits, or savings plans.

2.

Consider financial goals, income stability, risk comfort, tax impact, liquidity needs, existing commitments, and investment horizon before selecting a suitable investment option.

3.

Returns may vary based on market conditions, asset type, and allocation, while longer holding periods may reduce short-term fluctuations.

4.

A ten-year time frame supports medium-term goals, encourages regular saving habits, allows compounding, and offers a balance between growth potential and accessibility.

5.

Tax treatment varies by product type, contribution limits, holding rules, and prevailing tax laws, which may influence net returns.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Premier SIP is designed for combination of Benefits of two individual and separate products named (1) Tata AIA Life Insurance Tata AIA Smart SIP - Non-participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V02) and (2) Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V02). Product option: Future Secure These products are also available for sale individually without the combination offered/suggested.

Param Raksha Life Pro+ is designed for combination of Benefits of two individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V02). These products are also available for sale individually without the combination offered/suggested.

If your policy offers variable benefits, then the illustrations on this page will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

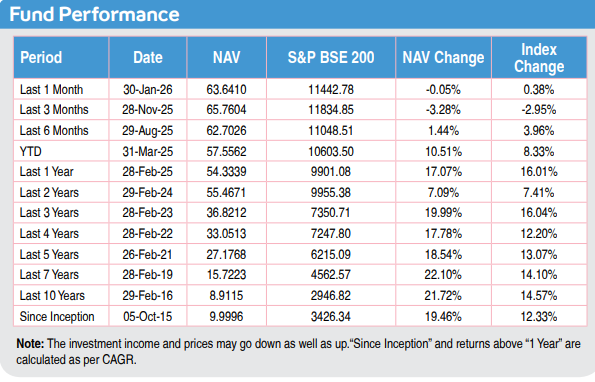

1Illustration shows monthly premium of ₹10,000 for Tata AIA Premier SIP for a 25-year-old male, standard life, premium payment term: 10 years, policy term: 20 years with 100% investment in Tata AIA Multi Cap fund in Future Secure Plan option. 4% and 8% are assumed rates of return. 18.54% is the 5-year return of Tata AIA Multi Cap fund as of February’26. Maturity amount: ₹16,10,156 at 4% returns, ₹29,18,995 at 8% returns and ₹1,31,00,326 at 18.54% returns. 18.54% is the 5-year CAGR of Tata AIA Multi Cap fund as of feb’26, which is projected for 20 years after adjusting for all expenses. Benchmark of this fund is S&P BSE 200.

Some benefits are guaranteed, and some benefits are variable with returns based on the future performance of your insurer carrying on life insurance business. If your policy offers guaranteed benefits, then these will be clearly marked “guaranteed’ in the illustration table on this page. If your policy offers variable benefits, then the illustrations on these pages will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

2Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfilment of conditions stipulated therein. The Tax-Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Tax laws are subject to amendments from time to time

3All funds open for new business which have completed 5 years since inception are rated 4 or 5 Star by Morningstar as of February 2026.

4Data from our Tata AIA fund fact sheet shows the performance of Tata AIA Multi Cap fund & SFIN NO: ULIF 060 15/07/14 MCF 110 as on Feb 2026. Benchmarked with Nifty 50.

6The Insured Amount under Terminal Illness with Term Booster option (in Health Buddy) is payable on earlier of death or diagnosis of Terminal illness of the Life Insured. Please refer Terms and Conditions for more details.

7Market-linked returns are subject to market risks and terms & conditions of the product. The assumed rate of returns or illustrated amount may not be guaranteed and depends on market fluctuations.

Investments are subject to market risks. The Company does not guarantee any assured returns. The investment income and price may go down as well as up depending on several factors influencing the market.

Linked Life Insurance products are different from traditional insurance products and are subject to risk factors.

The premium paid in Linked Life Insurance policies is subject to investment risks associated with capital markets and publicly available index. The NAV of the units may go up or down based on the performance of Fund and factors influencing the capital market/publicly available index and the insured is responsible for his/her decisions. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. On survival to the end of the policy term, the Total Fund Value including Top-Up Premium Fund Value valued at applicable NAV on the date of Maturity will be paid

The fund is managed by Tata AIA Life Insurance Company Ltd. (hereinafter the “Company”). Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & Tata AIA Smart SIP and Smart Sampoorna Raksha Supreme is only the name of the Unit Linked Life Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

The investment income and price may go down as well as up depending on several factors influencing the market. Please know the associated risks and the applicable charges, from your Insurance Agent or the Intermediary or Policy Document issued by the Insurance Company. Please make your own independent decision after consulting your financial or other professional advisor. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any). All investments made by the Company are subject to market risks. The Company does not guarantee any assured returns

Please know the associated risks and the applicable charges, from your Insurance Agent or the Intermediary or Policy Document issued by the Insurance Company. Please make your own independent decision after consulting your financial or another professional advisor

Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. Premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions

Buying a Life Insurance policy is a long-term commitment. An early termination of the policy usually involves high costs, and the Surrender Value payable may be less than the all the Premiums Paid.

Insurance cover is available under the product. For more details on risk factors, terms and conditions please read sales brochure carefully before concluding a sale.

L&C/Advt/2026/Jun/3807