Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Investing requires proper planning and careful allocation of funds. The right strategy can help you increase your savings balance ... Read more into an income-generating corpus. Depending on whether you are looking for monthly cash flow or long-term growth (or a combination thereof), your ₹20 Lakh lump sum investment provides you with maximum flexibility in determining your balance of safety vs return. To understand the risk-reward balance for your investment objectives, you can use both the advantages of fixed-rate products and the compounding benefits of growth-oriented investments like stocks. This article provides additional details about how to invest your ₹20 Lakh for both monthly income and long-term growth. Read less

Your premium calculation is in progress

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Your details could not be saved.

Please try again.

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Premier SIP Calculator

Here’s your customised plan

Get Maturity Benefit

As per assumed rate of return

₹34.57 Lakh

As per actual past performance

₹70.50 Lakh

Total premium: ₹11.99 Lakh

Additional Benefits

Life Cover (including Terminal Illness Cover)

Accidental Death Cover

Accidental Total & Permanent Disability

Discount

Applicable if the policy is purchased digitally.

This discount is auto-applied and can't be removed

A certified Tata AIA expert will call you from a 1600‑series number to help customise your plan.

Buy Now

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP - Non-participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V01) and

Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually. Product option: Future Secure.

Selecting an appropriate investment avenue for ₹20 Lakh depends on multiple factors rather than a single return expectation. Financial goals play an important role, as short-term needs differ significantly from long-term commitments such as retirement or a child’s future. Risk tolerance also influences selection, since younger investors may be more comfortable with market fluctuations than conservative investors. Additionally, inflation impact should be considered, as returns must help maintain the purchasing value over time.

After understanding how to invest ₹20 Lakh rupees for monthly income, let's go through 10 investment options to invest ₹ ₹20 Lakh.

Monthly income plans may suit individuals seeking a predictable cash flow from their investment. Pension plans may provide income either immediately or from a chosen future date, depending on the annuity option selected. Endowment plans offer life cover and maturity benefits, which can later be structured into a regular income stream. Fixed deposits allow investors to choose monthly or periodic payouts. Unit-linked insurance plans can also generate a monthly income by withdrawing the accumulated funds in instalments.

These policies integrate life coverage with investment growth through market participation. Your ₹20 Lakh premium is split between contributions for life cover and investing in equity, debt, or hybrid funds. The insurance component safeguards your dependants financially in case of untimely death during the policy term. Simultaneously, the investment portion grows through exposure to money market instruments.

For instance, investing ₹20 Lakh as a single premium with a 20-year commitment and assuming 7.5% annual growth may accumulate to over ₹80 Lakh. At maturity, you may receive it as lumpsum or monthly instalments to establish a regular income stream supporting your financial needs.

Two distinct pension formats exist: traditional annuity-linked insurance and retirement ULIPs, both providing life cover for family security. The difference lies in returns and risk exposure. Traditional annuities eliminate uncertainty, delivering fixed monthly payments post-retirement with your ₹20 Lakh investment remaining unchanged, excluding bonuses. Retirement ULIPs offer potential gains depending on fund performance but carry market risk. Both facilitate a monthly income during retirement years.

For example, a 42-year-old investing ₹20 Lakh in an annuity plan with a pension after 18 years may receive approximately ₹2.1 Lakh annually. This equals to around ₹17,500 monthly from age 60.

These endowment-based products provide death benefits with maturity payouts and may be suitable for conservative investors. Committing ₹20 Lakh to such plans can deliver a regular income spanning up to three decades. Insurers commonly add loyalty bonuses when investments continue beyond 10 years. This feature is a predetermined benefit unaffected by market fluctuations, resulting in a low-risk option. The protection framework helps ensure the family receives financial support upon your death during the policy period. If you survive till maturity, you get a fixed income in monthly instalments.

Depositing ₹20 Lakh yields interest between 5-6%, with senior citizens typically receiving slightly higher rates. Capital grows continuously across the selected tenure as interest accumulates. Upon completion, you can withdraw the total corpus or get a fixed amount periodically to generate a monthly income. For example, ₹20 Lakh at 6.25% over 10 years produces approximately 17.8 Lakh in interest and ₹36.7 Lakh corpus at maturity. These time deposits span 6 months to 10 years with interest rates locked at opening, ensuring predictable outcomes. Additionally, you can select monthly interest payouts to convert this investment into a consistent monthly income.

Systematic withdrawal plans enable mutual fund investors to redeem units systematically and receive scheduled payments. It may suit those investing ₹20 Lakh while requiring flexibility in payout timing and amounts. This involves selling specified units on predetermined dates with automatic fund transfers at chosen intervals, monthly, quarterly, or customised schedules matching cash requirements.

Real estate investment trusts acquire and operate commercial properties for income generation. They lease properties to tenants and distribute collected rent among shareholders as dividends. Deploying ₹20 Lakh in REITs mainly serves two purposes: capital appreciation through property value increases and income generation via dividend distributions. This offers real estate exposure without direct ownership, providing liquidity and professional management.

Equity investments produce income through dividends, with returns depending on stock market performance. Dividend distributions typically occur quarterly or annually, though certain companies pay monthly. Allocating ₹20 Lakh to dividend-paying equities creates potential income streams, though amounts vary with profitability and market conditions. This may suit investors comfortable with price volatility while seeking capital growth and periodic income.

This government-backed scheme targets conservative investors seeking low-risk savings with regular income. Operating on a 5-year tenure, it provides safety and predictability for investing ₹20 Lakh without market exposure. Government guarantee eliminates default risk, making it suitable for investors prioritising capital preservation while requiring a monthly income for ongoing expenses.

Professional fund managers invest in fixed-income securities, including corporate bonds, treasury bills, government securities, and commercial papers. Investors can select short-term or long-term funds, aligning with risk tolerance and financial objectives. Investing ₹20 Lakh provides access to diversified fixed-income portfolios managed by experienced professionals who optimise returns while controlling credit and interest rate risks.

The following are the key factors to consider before investing ₹20 Lakh.

Investment period: Long-term investments involve aggressive investment methods with higher risk tolerance. Short-term investment options require conservative investment methods. Align savings schemes with timelines set for each financial goal to balance returns and risk effectively.

Investment period: Long-term investments involve aggressive investment methods with higher risk tolerance. Short-term investment options require conservative investment methods. Align savings schemes with timelines set for each financial goal to balance returns and risk effectively.

To successfully invest ₹20 Lakh, one requires balancing financial goals, risk tolerance, and investment horizon. Diversification of investments in different asset classes can help enhance returns with controlled risk. Based on income generation, wealth creation, and wealth preservation strategies, suitable investment tools can be identified. Additionally, a periodic portfolio check should be done to keep investments aligned with your financial needs at different times in life.

1.

Earnings can fluctuate based on investment asset selection, investment term, return rate, and level of risk. Consider required returns, liquidity requirements, and associated risks before making decisions.

2.

FDs are safe, but the interest earned may not be higher than the rate of inflation. A risk of default by the institution is present, but it is covered by DICGC (Deposit Insurance and Credit Guarantee Corporation) insurance up to ₹5 Lakh for each depositor.

3.

Returns from ULIPs with annual premiums exceeding ₹2.5 Lakh are taxable2. Pension may be exempt under section 10(10A)(iii). Fixed deposits are liable for TDS on interest income. For mutual funds, REITs, and stocks, capital gains tax is applicable.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Premier SIP is designed for combination of Benefits of two individual and separate products named (1) Tata AIA Life Insurance Tata AIA Smart SIP - Non-participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V02) and (2) Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Product option: Future Secure These products are also available for sale individually without the combination offered/suggested.

Param Raksha Life Pro+ is designed for combination of Benefits of two individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). These products are also available for sale individually without the combination offered/suggested.

1Illustration shows a monthly premium of ₹15,000 for Tata AIA Premier SIP for a 30-year-old male, standard life, premium payment term: 10 years, policy term: 20 years with 100% investment in Tata AIA Multi Cap Fund in Future Secure plan option. 4% and 8% are assumed rates of return. 19.87% is the 5-year return of Nifty 500 Index as of October'25. Maturity amount: ₹23,75,740 at 4% returns, ₹43,20,914 at 8% returns and ₹2,33,98,560 at 19.87% returns. The fund value calculation is done by projecting the past returns of Nifty 500 Index after adjusting for all expenses in Tata AIA Premier SIP The above values have been calculated assuming 19.87% p.a. gross investment returns, which is the past 5-year return of Nifty 500 Index as of October'25.

2No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws.

3All funds open for new business which have completed 5 years since inception are rated 4 star or 5 star by Morningstar as of August 2025.

©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

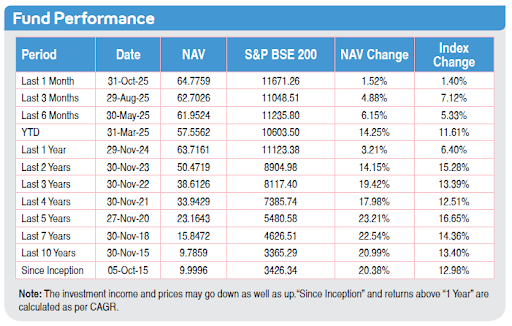

4Data from our Tata AIA fund fact sheet shows the performance of Tata AIA Multi Cap fund & SFIN NO: ULIF 060 15/07/14 MCF110 as on November 2025. Benchmarked with Nifty 50

If your policy offers variable benefits, then the illustrations on this page will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance

Linked Life Insurance products are different from traditional insurance products and are subject to risk factors.

The premium paid in Linked Life Insurance policies is subject to investment risks associated with capital markets and publicly available index. The NAV of the units may go up or down based on the performance of Fund and factors influencing the capital market/publicly available index and the insured is responsible for his/her decisions

Tata AIA Life Insurance Company Limited is only the name of the Life Insurance Company & Tata AIA Premier SIP is only the name of the Linked Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the insurance company

Past performance is not indicative of future performance

The risk factors of the bonuses projected under the product are not guaranteed

These products are subject to the overall performance of the insurer in terms of investments, management of expenses, mortality and lapses.

For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. Insurance cover is available under this product.

L&C/Advt/2026/Jan/0220

New user? Our experts are happy to help.

Thank you for sharing your details.

Our representative will contact you soon.