Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

A 5 year retirement plan is designed to build financial security for individuals nearing retirement. It ensures a stable income over a shorter... Read more investment horizon. It may suit those who prefer predictable returns with controlled risk. With fixed contribution periods, defined benefits, and flexible payout options, such plans help transform accumulated savings into a reliable post-retirement income stream. Read less

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Technical issue detected

please continue without OTP verification

A five year retirement plan is a structured financial arrangement designed to create a regular income stream after a short accumulation period. Unlike traditional retirement solutions that span several decades, this plan focuses on accelerated savings over five years. Contributions are made within a defined duration, after which income payouts begin based on selected terms. This structure may suit those approaching retirement.

A 5 year retirement plan works by allowing individuals to contribute systematically for five years. After the contribution phase ends, payouts begin either immediately or after a chosen deferment period. The structure provides clarity on premium duration, payout frequency, and income timelines. If the policyholder dies during the policy term, then the nominee gets the sum assured.

Non-Participating, Unit Linked, Individual Life Insurance Pension Plan UIN: 110L182V08)

Non-Linked Non-Participating Individual Life Insurance Plan (UIN:110L182V13)

The following are the reasons why one should choose a 5 year plan to retirement.

Here are some suitable retirement options to consider:

A 5 year retirement plan offers various benefits, some of which are as follows:

The following are the types of individuals who can consider a 5 year retirement plan.

Individuals approaching retirement age: Those between fifty-five and sixty can use this plan to bridge income gaps and ensure they enter their retirement life smoothly.

People planning defined near-term goals: The fixed structure supports funding planned life events, medical needs, or lifestyle adjustments after retirement.

Late planners seeking financial direction: Individuals who begin retirement planning later benefit from structured savings and faster financial alignment.

Consider the following before electing a 5 year retirement plan.

A retirement plan for 5 year duration offers clarity, discipline, and income certainty for individuals nearing retirement. It supports structured savings, manageable risk exposure, and defined payout timelines. By focusing on short-term preparedness, individuals gain better control over their financial transition into retirement. Careful evaluation of goals, affordability, and risk tolerance ensures alignment with personal retirement expectations.

1.

The suitability depends on age, income needs, risk preference, and retirement income expectations.

2.

The amount to be saved every month depends on desired retirement income, current age, expected inflation rate, and projected returns on investments.

3.

Estimate future expenses, adjust for inflation, assess retirement duration, and project returns to calculate an appropriate retirement corpus.

4.

The returns may be guaranteed or variable based on the structure of the plan, the investment allocation, and the payout structure chosen at the time of inception.

5.

The early withdrawal of funds may be permitted with certain conditions, reduced benefits, or charges, based on the terms and conditions of the plan.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Tata AIA Smart Pension Secure (UIN: 110L182V08) - Non-Participating, Unit Linked, Individual Life Insurance Pension Plan

The complete name of Tata AIA Fortune Guarantee Pension is Tata AIA Life Insurance Fortune Guarantee Pension (UIN:110N161V13) - A Non-Linked, Non-Participating, Annuity Plan.

1All funds open for new business which have completed 5 years since inception are rated 4 star or 5 star by Morningstar as of August 2025.

©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

2Partial withdrawals only available 3 times during the entire policy term and only for reasons specified in IRDA Regulations as amended from time to time

3The word Guaranteed and Guarantee means the annuity payout is fixed at inception of the policy and will be payable for whole of life or till death of the Annuitant(s).

4Income Tax benefits would be available as per the prevailing income tax laws under old tax regime, subject to fulfilment of conditions stipulated therein. Income Tax laws are subject to change from time to time. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

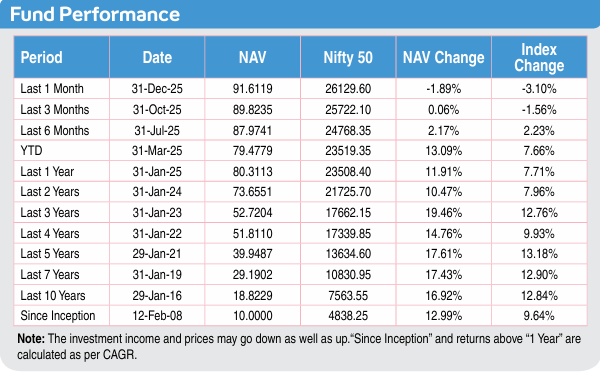

5Illustration shows Annual premium of ₹10,000 for Tata AIA Smart Pension Secure for a 40-year-old male, standard life, premium payment term: 5 years, policy term: 40 years. 4% and 8% are assumed rates of return. 17.61% is the 5-year return of Future Equity Pension Fund as of January'26. Maturity amount: ₹5,82,879 at 4% returns, ₹26,22,892 at 8% returns and ₹7,15,19,133 at 17.61% returns. The fund value calculation is done by projecting the past returns o Future Equity Pension Fund f after adjusting for all expenses in Tata AIA Smart Pension Secure Plan. The above values have been calculated, assuming 17.61% p.a. CAGR, which is the past 5-year return of Future Equity Pension Fund as of January'26.

Some benefits are guaranteed, and some benefits are variable with returns based on the future performance of your insurer carrying on life insurance business. If your policy offers guaranteed benefits, then these will be clearly marked “guaranteed’ in the illustration table on this page. If your policy offers variable benefits, then the illustrations on these pages will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Tax laws are subject to amendments from time to time. If any imposition (tax or otherwise) is levied by any statutory or administrative body under the Policy, Tata AIA Life Insurance Company Limited reserves the right to claim the same from the Policyholder.

For ULIP products

Linked Life Insurance products are different from traditional insurance products and are subject to risk factors.

The premium paid in Linked Life Insurance policies is subject to investment risks associated with capital markets and publicly available index. The NAV of the units may go up or down based on the performance of Fund and factors influencing the capital market/publicly available index and the insured is responsible for his/her decisions.

Tata AIA Life Insurance Company Limited is only the name of the Life Insurance Company & Tata AIA Smart Pension Secure is only the name of the Linked Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the insurance company.

The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns.

Past performance is not indicative of future performance.

If your policy offers variable benefits, then the illustrations on this page will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. Insurance cover is available under this product.

L&C/Advt/2026/Mar/2405