Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Retirement planning is a process that helps individuals plan their finances for their post-working life. During their working life, saving and investing money... Read more regularly can help accumulate a retirement corpus.

It is important for individuals to understand the types of retirement plans so that they can plan their finances well. Each retirement plan is designed in a unique way. Understanding the types of retirement plans in India can help individuals select the most suitable plan for their needs.Read Less

India provides different types of pension plans to cater to retirement savings needs. These plans vary based on structure, returns, and level of risk involved. Some of the plans are stable, while others are geared toward growth.

Guaranteed income plans are designed to provide fixed payouts after retirement. You build a corpus during your working years and receive a predictable income later.

These plans are often preferred by individuals who value stability in retirement income.

Key features include:

Guaranteed income retirement plans are among the more stable types of pension plans available in the market. Their primary purpose is to provide financial security after retirement.

These plans focus more on income protection rather than high returns.

Important features include:

Investment-linked retirement plans work slightly differently. These plans combine insurance protection with market-based investments.

The goal here is long-term wealth creation. Over time, market participation may help increase the retirement corpus.

Key aspects include:

Apart from insurance-based plans, India also offers several government-supported retirement schemes. These schemes are regulated and backed by the government, which adds a layer of stability.

Many times, individuals use these schemes as a core part of their retirement strategy.

Some commonly used options include:

Non-Participating, Unit Linked, Individual Life Insurance Pension Plan UIN: 110L182V08

Non-Linked Non-Participating, Individual Life Insurance Plan (UIN:110L182V13)

The evaluation of the right pension plan is of utmost importance, and for this, there are a few key factors to be considered before making any decision regarding the pension plan. Key factors to be considered include:

The amount invested in retirement plans may vary depending on the type of plan selected. Each plan has its own contribution structure and expected return pattern.

For example:

Retirement planning is an important part of financial security. Individuals need to save enough during their working years. The savings are required during retirement. Knowledge of the types of plans is necessary for the right decision in financial matters. The types of retirement plans in India are mainly guaranteed income plans, investment-linked plans, and government schemes. All the plans are beneficial in their own way. The right selection of the plans can result in a good corpus during retirement. It can also ensure a good income post-retirement.

1.

The better retirement option depends on individual financial goals and risk tolerance. Some investors prefer guaranteed income plans for stable payouts. Others prefer market-linked plans for higher growth potential.

2.

Government-backed schemes such as the Employees’ Provident Fund and the National Pension System are among the most commonly used retirement plans in India.

3.

The two major types of retirement plans are guaranteed income retirement plans and investment-linked retirement plans. The key difference lies in the structure of returns and the level of investment risk.

4.

Yes, individuals can invest in more than one pension plan. Many investors combine government schemes, insurance pension plans, and market-linked investments to build a diversified retirement portfolio.

5.

The ideal retirement corpus depends on lifestyle, expenses, and life expectancy. Financial planners often recommend building savings that can support living expenses for at least 20 to 30 years after retirement.

The linked insurance products do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Tata AIA Smart Pension Secure (UIN: 110L182V08) - Non-Participating, Unit Linked, Individual Life Insurance Pension Plan

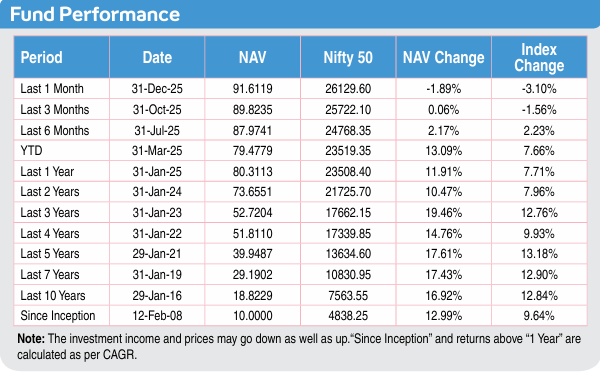

1Illustration shows annual premium of ₹50,000 for Tata AIA Smart Pension Secure for a 40-year-old male, standard life, premium payment term: 5 years, policy term: 40 years with 100% investment in Tata AIA Future Equity Pension fund. 4% and 8% are assumed rates of return. 17.61% is the 5-year return of Tata AIA Future Equity Pension fund as of January'26. Maturity amount: ₹5,82,879 at 4% returns, ₹26,22,892 at 8% returns and ₹7,15,19,133 at 17.61% returns. The fund value calculation is done by projecting the past returns of Tata AIA Future Equity Pension Fund for 40 years after adjusting for all expenses in Tata AIA Smart Pension Secure Plan. The above values have been calculated assuming 17.61% p.a. gross investment returns, which is the past 5-year return of Future Equity Pension Fund as of January'26. Benchmark of this fund is Nifty 50

25-year computed NAV for Future Equity Pension Fund as of January 2026. Other funds are also available. Benchmark of this fund is Nifty 50.

3Partial withdrawals only available 3 times during the entire policy term and only for reasons specified in IRDA Regulations as amended from time to time

4No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfilment of conditions stipulated therein. The Tax-Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

Some benefits are guaranteed, and some benefits are variable with returns based on the future performance of your insurer carrying on life insurance business. If your policy offers guaranteed benefits, then these will be clearly marked “guaranteed’ in the illustration table on this page. If your policy offers variable benefits, then the illustrations on these pages will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

5All funds open for new business which have completed 5 years since inception are rated 4 star or 5 star by Morningstar as of August 2025.

©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

6The word Guaranteed and Guarantee means the annuity payout is fixed at inception of the policy and will be payable for whole of life or till death of the Annuitant(s).

Unit Linked Life Insurance products are different from the traditional insurance products and are subject to the risk factors. Please know the associated risks and the applicable charges, from your Insurance Agent or Intermediary or Policy Document issued by the Insurance Company.

The fund is managed by Tata AIA Life Insurance Company Ltd. For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. The precise terms and condition of this plan are specified in the Policy Contract.

Past performance is not indicative of future performance. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any).

Investments are subject to market risks. The Company does not guarantee any assured returns. The investment income and price may go down as well as up depending on several factors influencing the market.

Please make your own independent decision after consulting your financial or other professional advisor.

Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & the Unit linked insurance product with Tata AIA /Tata AIA Life Insurance as its prefix is only the name of the Unit Linked Life Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

The performance of the managed portfolios and funds is not guaranteed, and the value may increase or decrease in accordance with the future experience of the managed portfolios and funds.

Premium paid in the Unit Linked Life Insurance Policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the Insured is responsible for his/her decisions.

Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the Insurance Company.

L&C/Advt/2026/Apr/2504