Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Surrendering a ULIP means closing the policy before maturity and withdrawing the accumulated fund value. The tax treatment depends ... Read more on the policy issue date, annual premium, sum assured, and timing of surrender. Understanding this ULIP surrender taxation helps investors make informed exit decisions and avoid adverse tax implications. Read less

Premier SIP Calculator

Here’s your customised plan

Get Maturity Benefit

As per assumed rate of return

₹34.57 Lakh

As per actual past performance

₹70.50 Lakh

Total premium: ₹11.99 Lakh

Additional Benefits

Life Cover (including Terminal Illness Cover)

Accidental Death Cover

Accidental Total & Permanent Disability

Discount

Applicable if the policy is purchased digitally.

This discount is auto-applied and can't be removed

Buy Now

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP - Non-participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V01) and

Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually. Product option: Future Secure.

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Success

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Failure

Your details could not be saved.

Please try again.

A ULIP is a hybrid financial product. It combines life insurance with market-linked investment. A part of the premium provides life cover. The remaining amount is invested in equity, debt, or balanced funds. The returns vary with market performance. Due to this structure, ULIPs have distinct taxation rules at maturity and surrender.

ULIP surrender refers to the voluntary termination of the policy before its maturity. Upon surrender, the insurer pays the fund value after applicable deductions. Many policyholders surrender due to urgent financial needs or when they find better investment alternatives. ULIPs carry a mandatory lock-in period of five years. Surrendering during this period may reduce benefits and attract tax.

Surrendering a ULIP can lead to tax. The tax depends on when you exit, when the policy was issued, and how much premium you pay. These rules are laid down in Section 10(10D) of the Income Tax Act. This section decides if the payout is tax-free or not.

A ULIP surrender amount is tax5-free only if it meets Section 10(10D) rules. For policies issued after 1 April 2012, the premium must be within 10% of the sum assured. For older policies (before 1 April 2012), the limit is 20%. For ULIPs issued on or after 1 February 2021, there is also a ₹2.5 lakh yearly premium cap across all ULIPs. If these rules are not followed, the surrender value becomes taxable.

If the payout becomes taxable, only the gains (surrender amount minus premiums paid) are taxed. This is taxed as capital gains under Section 112A at 12.5% on gains above ₹1.25 lakh in one year.

If you surrender before five years, the payout is usually taxable. Past 80C deductions may be reversed, and TDS may apply. The money also moves to a Discontinued Policy Fund till the 5-year lock-in end.

After five years, surrender is allowed freely. But it is not always tax5-free. The payout must still meet Section 10(10D) conditions. If not, the amount is taxed as capital gains. Partial withdrawals after five years are allowed too. They are tax5-free only if they meet 10(10D) rules.

For ULIPs issued before 1 February 2021, the ₹2.5 lakh cap does not apply. So, if they meet the sum-assured premium rules, the payout can stay tax-free. For ULIPs issued on or after 1 February 2021, the ₹2.5 lakh premium cap applies. If the total premium paid across ULIPs crosses this limit, tax exemption is lost and gains are taxed.

A ULIP can be surrendered at different stages of the policy term, but each stage has different implications. Below is an overview to understand how ULIP surrender taxation works.

ULIPs come with a mandatory 5-year lock-in period.

During this period, policyholders cannot freely withdraw funds without consequences.

Surrendering before 5 years may lead to penalties and deductions.

The fund value is moved to a Discontinued Policy Fund until the lock-in ends.

The surrender value may be lower due to applicable charges.

At the end of 5 years of lock-in, policyholders can exit without any penalties.

The insurance company will then pay the surrender value, excluding the charges incurred.

This provides the flexibility to discontinue the policy when the plan is not aligned with the investment objectives.

Before deciding to surrender, consider:

Financial needs and future goals

Impact on long-term wealth creation

Taxability of ULIP on surrender

Charges and deductions

ULIP surrender involves clear tax5 consequences. Surrendering before five years usually attracts tax and reverses earlier deductions. Exiting the plan after five years may act as a tax-saving strategy only when taxpayers meet certain criteria under Section 10(10D). For newer ULIP policies, premiums above 2.5 lakhs will attract capital gains tax. The contract terms and taxability of ULIP on surrender must be reviewed before surrendering a policy to serve personal interests better.

1.

It is the amount paid to the policyholder on early exit after deducting applicable charges.

2.

The insurer pays the fund value based on market performance. Surrender taxability of ULIP depends on surrender timing and Section 10(10D) compliance.

3.

Yes, but only if the policy meets Section 10(10D) conditions. Otherwise, the surrender value becomes taxable.

4.

If Section 10(10D) conditions are not met, the net gains (surrender value minus premiums paid) are taxed as capital gains.

5.

Redemption is tax5-exempt only if Section 10(10D) rules are satisfied. If premium limits are breached, the redemption amount is taxed as capital gains.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Param Raksha Life Pro+ is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). Both Smart Sampoorna Raksha Supreme and Tata AIA Health Buddy are also available for sale individually.

Health Buddy is part of the wellness offerings of TATA AIA Health Buddy. It is the customer’s sole discretion to avail the services. All medical-related services will be directly provided by the Service Providers and not by Tata AIA Life Insurance. These services shall be subject to the availability of the Service Provider. Tata AIA Life Insurance shall not be liable for any liability arising due to customer opting to avail this feature from the Service Providers. For more details on the benefits covered, please refer to the website, contact our Insurance Advisor/Intermediary, or visit our nearest Branch Office.

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP, a non-participating, unit-linked, individual life insurance savings plan (UIN: 110L174V02), and Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually.

Tata AIA Smart SIP - Non-Participating, Unit Linked Individual Life Insurance Savings Plan (UIN:110L174V02)

Tata AIA Smart Sampoorna Raksha Supreme - Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02).

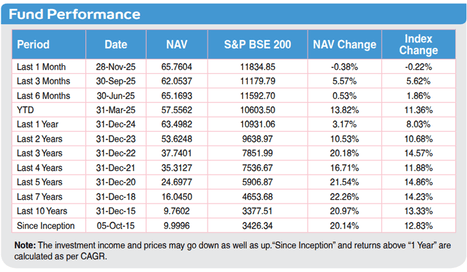

1Illustration shows monthly premium of ₹15,000 for Tata AIA Premier SIP for a 25-year-old male, standard life, premium payment term: 10 years, policy term: 20 years with 100% investment in Tata AIA Multi Cap fund in Future Secure Plan option. 4% and 8% are assumed rates of return. 21.54% is the 5-year return of Tata AIA Multi Cap fund as of December’25. Maturity amount: ₹22,57,608 at 4% returns, ₹40,92,738 at 8% returns and ₹2,77,34,574 at 21.54% returns. The fund value calculation is done by projecting the past returns of Tata AIA Multi Cap Fund for 20 years after adjusting for all expenses in Tata AIA Premier SIP Plan. The above values have been calculated assuming 21.54% p.a. CAGR, which is the past 5-year return of Tata AIA Multi Cap Fund as of December'25. Benchmark of this fund is S&P BSE 200.

Some benefits are guaranteed, and some benefits are variable with returns based on the future performance of your insurer carrying on life insurance business. If your policy offers guaranteed benefits, then these will be clearly marked “guaranteed’ in the illustration table on this page. If your policy offers variable benefits, then the illustrations on these pages will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

2All funds open for new business which have completed 5 years since inception are rated 4 or 5 Star by Morningstar as of August 2025.

3©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

4The Insured Amount under Terminal Illness with Term Booster option (in Health Buddy) is payable on earlier of death or diagnosis of Terminal illness of the Life Insured. Please refer Terms and Conditions for more details.

5Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfilment of conditions stipulated therein. The Tax-Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you.

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Tax laws are subject to amendments from time to time

65-year computed NAV for Multi Cap Fund as of December 2025. Other funds are also available. Benchmark of this fund is S&P BSE 200.

Linked Life Insurance products are different from traditional insurance products and are subject to risk factors.

The premium paid in Linked Life Insurance policies is subject to investment risks associated with capital markets and publicly available index. The NAV of the units may go up or down based on the performance of Fund and factors influencing the capital market/publicly available index and the insured is responsible for his/her decisions.

The fund is managed by Tata AIA Life Insurance Company Ltd. (hereinafter the “Company”). Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & NAME OF ULIP PROD is only the name of the Unit Linked Life Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns

Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the insurance company. Please make your own independent decision after consulting your financial or another professional advisor

Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. Premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions

Market-linked returns are subject to market risks and terms & conditions of the product. The assumed rate of returns or illustrated amount may not be guaranteed and depends on market fluctuations.

Past performance is not indicative of future performance. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any)

If your policy offers variable benefits, then the illustrations on this page will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. Insurance cover is available under this product.

L&C/Advt/2026/Mar/2359