Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

NRIs consider ULIPs (Unit Linked Insurance Plans) to be a unique investment opportunity. NRIs have the opportunity to invest in ULIPs in India in... Read more accordance with the Foreign Exchange Management Act (FEMA). Individual policyholders may use this plan as an investment vehicle to achieve their long-term financial goals. NRIs will be able to participate in the growing financial market and achieve their financial objectives through various ULIP schemes available. Read on to know more about ULIPs for NRIs. Read Less

Premier SIP Calculator

Here’s your customised plan

Get Maturity Benefit

As per assumed rate of return

₹34.57 Lakh

As per actual past performance

₹70.50 Lakh

Total premium: ₹11.99 Lakh

Additional Benefits

Life Cover (including Terminal Illness Cover)

Accidental Death Cover

Accidental Total & Permanent Disability

Discount

Applicable if the policy is purchased digitally.

This discount is auto-applied and can't be removed

Buy Now

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP - Non-participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V01) and

Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually. Product option: Future Secure.

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Success

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Failure

Your details could not be saved.

Please try again.

ULIP is a multi-functional insurance product. In this plan, both life insurance and investment plans are combined. Premiums for ULIP plans need to be paid regularly. A part of the premium goes towards providing life insurance coverage. Remaining premiums are then invested in equities and debts as per user preference.

ULIP invests money taken from policyholders into funds they choose. The total invested amount is divided into 'units', each with a certain face value. The 'units' are then allocated to investors based on their investment. Each unit has an NAV (Net Asset Value), which shows how much each asset is worth. ULIP calculators can help you estimate potential returns based on factors like premium amount, fund choice, and investment duration.

Unit-linked plans are managed by professional fund managers, who invest a significant portion of the premium after closely monitoring market fluctuations. Depending on the results of the analysis, necessary changes are made again.

After the policy matures, you will receive the total fund value at that time. In the event of the policyholder’s death, the nominee receives the higher of the sum assured or 105% of the premium amount paid to date or the fund value of the policy.

Here are some of the best plans offered by Tata AIA Life Insurance you can explore:

ULIP for NRIs combine investment opportunities with life insurance protection, helping individuals participate in India’s market growth while planning long-term financial goals.

NRIs looking to invest in ULIPs can benefit from these features

NRIs can invest in a ULIP plan online based on their financial goals and risk appetite. The following are the steps to invest in ULIP for NRI.

While investing in ULIP plans for NRIs, carefully evaluate regulatory, financial, and investment-related factors before selecting a ULIP plan to ensure it aligns with their long-term objectives.

NRIs should ensure that investments comply with FEMA and RBI guidelines applicable to overseas investors. Proper compliance helps avoid legal complications and supports smooth investment management from abroad.

Defining financial goals before selecting a ULIP helps in choosing suitable fund options and policy structures. Investment objectives may include retirement planning, wealth creation, or future family-related financial responsibilities.

Exchange rate fluctuations can influence the overall investment value for NRIs. Monitoring currency movement helps in understanding potential changes in returns and supports better financial planning decisions.

Reviewing historical fund performance and risk profile is important before investing in a ULIP. This helps NRIs select suitable funds that match their financial expectations and risk tolerance.

ULIPs may include charges such as fund management, mortality, and premium allocation charges. Understanding these costs helps NRIs evaluate the overall impact on long-term investment returns.

Every NRI should keep the following documents ready when purchasing a ULIP for NRI. The required documents include:

Selecting the right NRI ULIP plans requires careful comparison of financial goals, policy features, flexibility, and long-term investment suitability.

ULIPs for NRIs offer the following tax benefits:

ULIP premiums paid by NRIs and Indian citizens are tax exempt2. NRIs are eligible for a deduction of ₹1.5 Lakh under Section 80C of the Income Tax Act. If the ULIP premium is up to ₹2,50,000 and equal to or less than 10% of the sum assured, NRIs are eligible for maturity benefit exemption under Section 10(10D) of the Income Tax Act, 1961

As per section 10(10D) of the Income Tax Act, NRIs can avail of exemptions from taxes on death benefits. When NRIs reach maturity, they qualify for tax2 benefits, subject to the following provisions:

ULIP plans provide NRIs with life insurance protection as well as long-term investment opportunities. With features such as fund switching, top-ups, and partial withdrawals, ULIPs allow flexibility to adapt to changing market conditions. Aside from growth benefits, ULIPs offer valuable tax2 benefits under Section 80C and 10(10D). However, NRIs should carefully examine policy charges, lock-in periods, taxation rules, and DTAA provisions before investing

1.

Yes, NRI can invest in ULIP, as permitted under the Foreign Exchange Management Act (FEMA) and the IRDAI regulations.

2.

By complying with FEMA regulations and using NRE/NRO bank accounts, Non-Resident Indians (NRIs) can invest in Indian mutual funds across equity, debt, and hybrid schemes.

3.

NRIs' new rules primarily concern updates in income tax laws and residency requirements, particularly for individuals in tax-free jurisdictions and high-income individuals.

4.

It depends on a Non-Resident Indian (NRI)'s risk appetite, investment goals (short-term vs. long-term), and repatriation requirements.

5.

Since ULIPs are categorised by investment focus, purpose, and death benefit structure, a fixed number is not available. There are two main structural categories: Type 1 (higher life cover, lower fund value payout) and Type 2 (higher combined sum assured and fund value payout). The other types of ULIPs include those for retirement, education, wealth creation, etc.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP, a non-participating, unit-linked, individual life insurance savings plan (UIN: 110L174V02), and Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually.

Param Raksha Life Pro+ is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). Both Smart Sampoorna Raksha Supreme and Tata AIA Health Buddy are also available for sale individually.

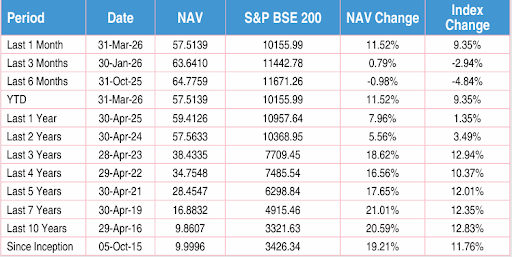

1Illustration shows monthly premium of ₹15,000 for Tata AIA Premier SIP for a 25-year-old male, standard life, premium payment term: 10 years, policy term: 20 years with 100% investment in Tata AIA Multi Cap fund in Future Secure Plan option. 4% and 8% are assumed rates of return. 17.65% is the 5-year return of Tata AIA Multi Cap fund as of April’26. Maturity amount: ₹24,15,144 at 4% returns, ₹43,78,331 at 8% returns and ₹ 1,73,67,190 at 17.65% returns. The fund value calculation is done by projecting the past returns of Tata AIA Multi Cap Fund for 25 years after adjusting for all expenses in Tata AIA Premier SIP Plan. The above values have been calculated assuming 17.65% p.a. CAGR, which is the past 5-year return of Tata AIA Multi Cap Fund as of April'26. Benchmark of this fund is S&P BSE 200.

2Income Tax benefits would be available as per the prevailing income tax laws, subject to fulfillment of conditions stipulated therein. Income Tax laws are subject to change from time to time. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implication mentioned anywhere in this document. Please consult your own tax consultant to know the tax benefits available to you.

3All funds open for new business which have completed 5 years since inception are rated 4 star or 5 star by Morningstar as of August 2025.

45-year computed NAV for Multi Cap Fund as of April 2026. Other funds are also available. Benchmark of this fund is S&P BSE 200.

5Data from our Tata AIA fund fact sheet shows the performance of Tata AIA Multi Cap fund & SFIN NO: ULIF 060 15/07/14 MCF110 as on April 2026. Benchmarked with Nifty 50

©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

Some Benefits are guaranteed, and some Benefits are variable (non-guaranteed) with returns based on the future performance of the opted funds and fulfilment of other applicable Policy conditions. If your Policy offers guaranteed returns, then these will be clearly marked as \"guaranteed\" in the illustration table on this page. If your policy offers non-guaranteed returns, then illustration will show two different rates of assumed future investment returns. The above illustration has been determined using assumed future investment returns of 8% and 4% respectively. The rates used have been set by the Life Insurance Council. These assumed rates of return are not guaranteed and there are no upper and lower limits of what you might get back at Maturity, due to the fact that the value of your Policy is dependent on a number of factors including future investment performance.

After a lock-in period of 5 years, you can withdraw funds during times of emergency. It depends on the ULIP plan you choose how often and how much you can withdraw.If your policy offers variable benefits, then the illustrations on this page will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

Linked Life Insurance products are different from traditional insurance products and are subject to risk factors.

Tax benefits of up to ₹46,800 u/s 80C is calculated at highest tax slab rate of 31.20% (including cess excluding surcharge) on life insurance premium paid of ₹1,50,000 as per old tax regime. Tax benefits under the policy are subject to conditions laid under Section 80C, 80D,10(10D), 115BAC and other applicable provisions of the Income Tax Act,1961. The Tax Free income is subject to conditions specified under section 10(10D) and other applicable provisions of the Income Tax Act,1961. Tax laws are subject to amendments made thereto from time to time. Please consult your tax advisor for details, before acting on above.

Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. Premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions

Tata AIA Life Insurance Company Limited is only the name of the Life Insurance Company & Tata AIA Smart SIP, Tata AIA Smart Sampoorna Raksha Supreme is only the name of the Linked Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

Please know the associated risks and the applicable charges, from your Insurance Agent or the Intermediary or Policy Document issued by the Insurance Company. Please make your own independent decision after consulting your financial or another professional advisor.

The information, provided herein, may not be treated as a solicitation request in any manner. Any decision to buy online insurance by NRIs is completely his/her choice. The insurer is permitted to solicit insurance in India and settles claim in INR only.

Past performance is not indicative of future performance

The risk factors of the bonuses projected under the product are not guaranteed

These products are subject to the overall performance of the insurer in terms of investments, management of expenses, mortality and lapses.

For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. The precise terms and condition of this plan are specified in the Policy Contract.

Life insurance cover is available under the solution. For details on products, associated risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale.

L&C/Advt/2026/Jun/3518