Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

Health insurance is a financial product that helps pay for medical and healthcare expenses. This covers hospitalisation expenses, including... Read more surgeries and treatments, and other related expenses. Health insurance plays the role of a safety net. It eases up the economic burden usually associated with unanticipated illness or mishap. It enables individuals to concentrate on their recovery rather than on their bills. As medical costs increase rapidly in India, it is necessary to be familiar with the various kinds of health insurance and how they work. With this knowledge, one can plan their finances in the long run. Read less

There are several types of health plans available in India. Each plan serves a specific purpose and fits different lifestyles, ages, and family needs.

Health insurance constitutes an agreement between the consumer and the insurer. You pay a premium at predetermined intervals. In exchange, the insurer promises to reimburse specific medical expenses incurred by you or your dependants.

A key component of financial security is health insurance. In India, medical expenses are high and keep going up each year. Even a single hospital stay can negatively impact savings or put families in debt if they do not have health insurance. A suitable health plan helps reduce this financial burden and brings peace of mind.

Several common benefits are available under different types of health plans.

Do not choose your plan solely on popularity or advertisement. Some important factors you need to check are:.

Choose sum insured that meets your expected medical costs based on your age and lifestyle.

Ensure the premium is affordable, but do not minimise coverage.

Find out how long you must wait for pre-existing conditions or particular treatments.

Network hospitals refer to a larger network that provides better access to cashless hospitalisation.

Check for add-ons/riders3 such as maternity cover, critical illness rider or daily hospital cash as required.

To find the best health insurance for you, you need to:

Compare different plans from different insurance companies and look at the amount of coverage you will get, how much you will pay each month (premium), what is covered/not covered by the plan, and whether you have any riders on the policy (add-ons).

Consider whether or not the insurance company you are thinking about will allow you to renew the plan at a reduced rate for the rest of your life.

Use online comparison systems to help you compare plans, or ask an insurance advisor to help you understand what the options are and how to make a decision about them.

Making wise financial decisions will be made easier if you are aware of the various forms of health insurance and how they relate to your particular financial circumstances. It is crucial to remember that every kind of health insurance product—individual, family, senior citizen, etc.—has special advantages of its own and can be useful in the case of an unexpected medical emergency. Your long-term financial security can also be guaranteed by choosing an insurance plan that meets your health needs.

1.

Individual, family floater, senior citizen, critical illness, personal accident, maternity, top-up, and group plans.

2.

Individual health insurance, family floater, senior citizen plans, and critical illness insurance.

3.

Notify the insurer, submit required documents and bills, and follow the claim steps.

Claims can be cashless or reimbursement, based on the hospital and policy rules.

4.

Yes. Premiums are eligible for tax* deductions under Indian laws, subject to conditions.

5.

There is no fixed limit. Some insurers offer coverage up to ₹1 crore or more based on needs and affordability.

The linked insurance product do not offer any liquidity during the first five years of the contract. The policy holder will not be able to surrender/withdraw the monies invested in linked insurance products completely or partially till the end of the fifth year.

Tata AIA Pro-Fit comprises of Tata AIA Health Pro, A Non-Participating, Unit-linked, Individual Health Insurance Plan (UIN: 110L180V01), Tata AIA Health Secure, A Non- Participating, Unit Linked, Individual Health rider (UIN: 110A050V01) & Tata AIA Health Buddy Non-Participating, Non-Linked Individual Health Product (UIN: 110N183V01) Tata AIA Smart Health Pro and Tata AIA Health Buddy are also available for sale individually.

Tata AIA Health Buddy Plan – Non-Participating, Non-Linked Individual Health Product (UIN: 110N183V01)

Tata AIA Health SIP (UIN:110L184V01) - Non-participating, Unit Linked, Individual Health Insurance Plan

Tata AIA Shubh Health Plus comprises of Tata AIA Health SIP - A Non-Participating, Unit-linked, Individual Health Insurance Plan (UIN: :110L184V01), Tata AIA Health Buddy, A Non-linked, Non-participating, Individual Health Product (UIN: 110N183V01 or any other later version). Tata AIA Health SIP and Tata AIA Health Buddy are also available individually for sale.

These products are also available for sale individually without the combination offered/ suggested. This benefit illustration is the arithmetic combination and chronological listing of combined benefits of individual products. The customer is advised to refer the detailed sales brochure of respective individual products mentioned herein before concluding sale.

2Get daily cash benefit of up to ₹20,000 on hospitalization & Up to ₹40,000 on ICU admission

3Riders are not mandatory and are available for nominal extra cost. For more details on benefits, premiums, and exclusions under the Rider, please contact Tata AIA Life's Insurance Advisor/Intermediary/ branch.

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Tax laws are subject to amendments from time to time. If any imposition (tax or otherwise) is levied by any statutory or administrative body under the Policy, Tata AIA Life Insurance Company Limited reserves the right to claim the same from the Policyholder.

Tata AIA Life Insurance Company Limited is only the name of the Insurance Company & Tata AIA Health Pro & Tata AIA Health SIP is only the name of the Unit Linked health Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

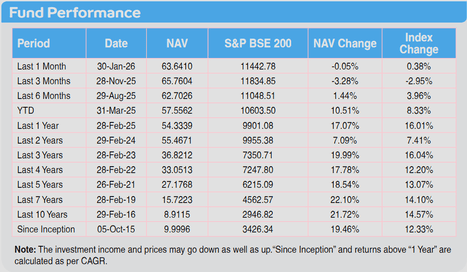

The fund is managed by Tata AIA Life Insurance Company Ltd.

For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale. The precise terms and condition of this plan are specified in the Policy Contract.

Past performance is not indicative of future performance. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any).

All investments made by the Company are subj ect to market risks. The Company does not guarantee any assured returns. The investment income and price may go down as well as up depending on several factors influencing the market.

Please make your own independent decision after consulting your financial or other professional advisor.

Unit Linked Insurance products are different from the traditional insurance products and are subject to the risk factors. Please know the associated risks and the applicable charges, from your Insurance Agent or Intermediary or Policy Document issued by the Insurance Company.

Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. The underlying Fund's NAV will be affected by interest rates and the performance of the underlying stocks.

The performance of the managed portfolios and funds is not guaranteed, and the value may increase or decrease in accordance with the future experience of the managed portfolios and funds.

Premium paid in the Unit Linked Insurance Policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the Insured is responsible for his/her decisions.

Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the Insurance Company.

Insurance cover is available under the product.

The products are underwritten by Tata AIA Life Insurance Company Ltd.

The plans are not a guaranteed issuance plan, and it will be subject to Company’s underwriting and acceptance.

For more details on risk factors, terms and conditions please read sales brochure carefully before concluding a sale.

All Premiums are subject to applicable taxes, cesses & levies which will entirely be borne by the Policyholder and will always be paid by the Policyholder along with the payment of Premium. If any imposition (tax or otherwise) is levied by any statutory or administrative body under the Policy, Tata AIA Life Insurance Company Limited reserves the right to claim the same from the Policyholder. Alternatively, Tata AIA Life Insurance Company Limited has the right to deduct the amount from the benefits payable by Us under the Policy.

Auto debit discount is applicable for Payments made through any electronic mode through an auto debit mandate for 1st-year instalment.

Risk cover commences along with policy commencement for all lives, including minor lives.

Buying a Health Insurance Policy is a long-term commitment. An early termination of the Policy usually involves high costs, and the Surrender Value payable may be less than the all the Premiums Paid.

In case of non-standard lives and on submission of non-standard age proof, extra premiums will be charged as per our underwriting guidelines.

Discount on policy will be subject to sales literature and policy contract.

L&C/Advt/2026/Apr/2505