Call us

Call us

FOR EXISTING POLICY

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Call us:

FOR NEW POLICY

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY

Want to buy a new policy online?

FOR NEW POLICY (NRIs)

Note: Consent is provided to Tata AIA Life Insurance Company Limited to contact you by calling/giving missed call to the above numbers.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

No relevant search results found.

A Unit Linked Insurance Plan (ULIP) is a type of life insurance plan that offers dual benefits: life cover and the option... Read more to invest in the financial market for wealth. When you pay the premium, one part goes towards insurance, and the rest is invested to build wealth over time. ULIPs have a five-year lock-in period and offer tax benefits6 under Section 80C and Section 10(10D), as per applicable laws. Secure your family while creating wealth for your financial future with Tata AIA Life Insurance Wealth Solutions with 18.54% returns as of Feb’ 26 (Benchmark: 13.07%)12.

Example: A 25-year-old individual investing in ULIP can steadily build a sizeable corpus over 15-20 years while ensuring continuous life cover for his family’s financial security. This long term approach helps him secure his own financial future without facing potential financial constraints. Read Less

Ulip Calculator

Here’s your customised plan

Get Maturity Benefit

As per assumed rate of return

₹34.57 Lakh

As per actual past performance

₹70.50 Lakh

Total premium: ₹11.99 Lakh

Additional Benefits

Life Cover (including Terminal Illness Cover)

Accidental Death Cover

Accidental Total & Permanent Disability

Discount

Applicable if the policy is purchased digitally.

This discount is auto-applied and can't be removed

Buy Now

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP - Non-participating, Unit-linked, Individual Life Insurance Savings Plan (UIN: 110L174V01) and

Tata AIA Health Buddy - Non-participating, Non-Linked, Individual Health Product (UIN:110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually. Product option: Future Secure.

Your premium calculation is in progress

Kindly enter the OTP sent to

Please enter valid OTP

01:60

Didn't receive OTP?

Success

Your details have been successfully submitted. A representative from Tata AIA Life Insurance will call you soon.

Failure

Your details could not be saved.

Please try again.

A ULIP (Unit Linked Insurance Plan) is a financial product that provides life insurance protection along with investment opportunities. A ULIP plan provides your family with life insurance, while the balance is invested in market-linked8 funds like equity, debt, or a mix of both. The dual benefit of this policy allows you to protect your loved ones and grow your wealth over time to meet long-term goals, such as financing your child's education or retirement planning. In addition, ULIPs give you more control over your financial future by allowing you to choose or switch funds according to your risk appetite.

In a ULIP plan, a portion of your premium provides life cover, while the remaining amount is invested in market-linked7 funds. Here’s how it works:

Professional fund managers manage the investment portion of your ULIP. The fund managers make investment decisions based on various factors, such as market conditions and the fund's objective. To manage your chosen fund, the life insurance company charges you a fee known as fund management fees.

There is a 5-year lock-in period for ULIPs. You cannot surrender or partially withdraw from your policy during the first five years. This aims to promote long-term investment.

Under Section 80C of the Income Tax Act, 1961, ULIP premiums qualify for tax deductions6 (up to ₹1.5 Lakh). Section 10(10D) allows the maturity amount to be tax-free under certain conditions.

To understand the role of insurer and policyholder, let's consider an example:

Suppose Nakul, a 25-year-old professional, invests in a ULIP for 20 years to build a retirement corpus.

Scenario 1: In case of an unfortunate demise

If Nakul passes away during the policy term, his family receives a death benefit equal to the higher of the sum assured or the fund value. This ensures his family's financial stability, irrespective of how the investment portfolio has performed.

Scenario 2: On maturity

If Nakul completes the full policy term, he receives the accumulated fund value. This maturity amount can then support his retirement plans and help him maintain his lifestyle post-retirement.

Choosing the best ULIP plan involves reviewing different features, costs, and fund options carefully. Since ULIPs vary across insurers, comparing them helps in understanding how each plan is structured.

ULIP plans differ in terms of charges, fund options, flexibility, and policy features. Reviewing multiple plans side by side can help in identifying how they vary across these aspects and how they align with different financial preferences.

ULIPs offer different types of funds whose performance is linked to the market. Looking at past fund performance over different time periods can give a general idea of consistency and volatility, although returns are not guaranteed.

Some ULIPs offer more flexibility than others. This may include options to switch between funds, adjust premium payments, or choose policy tenure. A plan with wider options allows more room for changes over time.

ULIPs include various charges such as premium allocation charges, fund management fees, policy administration charges, and mortality charges. These costs can impact the overall value of the investment, so it is important to review them in detail.

Many insurers provide online ULIP calculators. These tools can be used to estimate potential returns based on premium, tenure, and fund choice. The figures are indicative and depend on market performance.

The solvency ratio reflects the financial strength of an insurance company. A ratio of 1.5 or higher is generally used as a reference point to indicate the insurer’s ability to meet its obligations.

The claim settlement ratio shows how many claims an insurer has settled compared to the total claims received in a financial year. This helps in understanding the insurer’s claim settlement record.

ULIPs come with a mandatory 5-year lock-in period. During this time, withdrawals are restricted, which makes it important to consider the investment horizon before selecting a plan.

Online comparison platforms and insurer websites provide details on premiums, features, and fund options. Reviewing these sources can help in understanding differences across plans.

Here’s how different investors can consider ULIPs based on their investor profiles.

| Investor Profile | Risk Appetite | Fund Type | Typical Financial Goal | Explanation |

|---|---|---|---|---|

Young Professional |

High |

Equity funds (stock market–linked) |

Long-term wealth creation, children’s education |

Time horizon is long, so market ups and downs can be absorbed |

Mid-Career Investor |

Moderate |

Balanced / hybrid funds (equity + debt) |

Wealth building, home deposit |

Mix of growth and stability helps avoid large fluctuations |

Pre-Retiree |

Low / Conservative |

Debt funds (lower-risk) |

Capital protection, retirement planning |

Focus is on stability and avoiding loss of savings |

Goal-Oriented Investor |

High initially, then reduces |

Lifecycle / dynamic funds (shift to debt over time) |

Long-term goals (10–15+ years) |

Risk reduces gradually as the goal approaches |

| Types of Funds Options | Details |

|---|---|

| Equity-Based ULIP Funds | High-risk investments in company stocks offering potential long-term returns. |

| Hybrid or Balanced Funds | Balanced mix of equity and debt for moderate-risk investors. |

| Debt-Based ULIP Funds | Low-risk investments in bonds and securities with modest returns. |

| Cash Funds | Money market investments offering stability with low risk and returns |

| Types of Funds Options | Details |

|---|---|

| ULIP plans for wealth creation | Long-term market-linked7 investments to achieve significant financial goals. |

| ULIP plans for children's education | Education funding with partial withdrawals from the ULIP post lock-in period. |

| ULIP plans for health benefits | Emergency medical fund with optional health rider8 coverage. |

| ULIP plans for retirement | Long-term corpus building for a comfortable post-retirement lifestyle. |

| Types of Funds Options | Details |

|---|---|

| Single premium | One-time lump sum investment for long-term wealth growth. |

| Regular premium | Monthly or annual payments for gradual corpus accumulation through steady income. |

| Types of Funds Options | Details |

|---|---|

| Level cover | Constant life coverage throughout the policy term for stable protection. |

| Increasing life cover | Progressive coverage increases to match growing responsibilities and financial needs. |

The following are some of the types of investors who may consider ULIPs.

After understanding what ULIP means, let’s find out why one should invest in it.

Many investors evaluate ULIPs alongside mutual funds and term insurance. The key difference lies in how these products combine protection, taxation, and investment discipline.

| Parameter | ULIP (Unit Linked Insurance Plan) | Mutual Funds | Fixed Deposits (FDs) | PPF (Public Provident Fund) |

|---|---|---|---|---|

Primary Purpose |

Relevant where a combined insurance and investment structure is preferred in one plan |

Works in scenarios focused on market-linked wealth creation |

Fits situations prioritising capital protection and stable returns |

Suits long-term savings with a focus on capital safety and tax benefits |

Structure |

Bundled product combining insurance and investment |

Standalone investment product |

Simple deposit-based product |

Government-backed savings scheme |

Lock-in Period |

5-year lock-in period |

No lock-in (except ELSS: 3 years) |

Based on chosen tenure |

15-year lock-in with partial withdrawal options |

Liquidity |

Limited access initially; withdrawals allowed after lock-in |

High liquidity with easy redemption (except ELSS) |

Early withdrawal allowed with penalty |

Limited liquidity; partial withdrawals allowed after a few years |

Tax Treatment |

Eligible under Section 80C; maturity may be tax-free under Section 10(10D), subject to conditions |

ELSS qualifies under 80C; other funds taxed as per capital gains rules |

Tax-saving FD qualifies under 80C; interest is taxable |

EEE status (investment, interest, and maturity are tax-free under current rules) |

Charges / Costs |

Includes multiple charges such as allocation, administration, fund management, and mortality charges |

Mainly expense ratio and possible exit load |

Minimal charges; penalty may apply on early withdrawal |

No major charges |

Transparency |

Moderate due to bundled structure |

High transparency with NAV and portfolio details |

Clear and easy to understand |

Simple and clearly defined structure |

Flexibility |

Switching allowed within available fund options |

High flexibility to switch, redeem, or rebalance |

Limited flexibility once tenure is fixed |

Limited flexibility due to long lock-in |

Insurance Component |

Life cover included |

No insurance component |

No insurance component |

No insurance component |

Investment Control |

Limited to available fund options within the plan |

Wide choice across fund types and strategies |

No active investment decision required |

No investment choice; fixed structure |

Tenure Orientation |

Generally aligned with long-term planning |

Suitable across short-, medium-, and long-term horizons |

Fixed tenure as selected |

Designed for long-term savings (15 years) |

To simplify how investors should evaluate a ULIP, Tata AIA uses a structured approach called the “ULIP Fit Framework”. This framework is designed to help align the product with real financial needs rather than just returns.

Start by identifying the goal. ULIPs are more suitable for long-term goals such as retirement, children’s education, or wealth creation over 10 to 20 years.

ULIPs work best when held for longer durations. Staying invested beyond 10 years allows compounding and cost efficiency to play out effectively.

Choose between equity, debt, or hybrid funds based on your comfort with market fluctuations and expected returns.

Here are the key benefits a ULIP plan offers

ULIPs Plans are known for the dual advantage of investment and insurance they offer under a single policy. The life insurance cover will secure your family in your absence, and the investment option will help you create wealth for your future financial goals.

With a ULIP policy, you can choose between equity, hybrid, and debt fund options based on your high, medium, or low risk profile. For example, young earners can choose a high-risk equity fund, whereas individuals close to retirement can choose a low-risk conservative debt fund.

You can keep track of the performance of the ULIP funds based on the market movement and switch between them to enhance the potential gains.

ULIP investment plans have a mandatory lock-in period of 5 years. After the lock-in period, you can make partial withdrawals from your ULIP policy to meet any immediate financial needs.

ULIP fund management ensures that returns increase, helping you achieve long-term financial goals.

Here's how you can manage your ULIP investments:

ULIPs have equity, debt, and balanced funds. Choose based on risk appetite and investment horizon.

Track the Net Asset Value (NAV) and switch funds if required. Market conditions affect ULIP returns, so periodic reviews are essential. You can also compare the current returns with average ULIP returns in last 10 years.

ULIPs provide free switching options between equity and debt funds. Use this feature as per market conditions and financial objectives.

ULIPs may provide higher returns when invested for 10-15 years, as the benefits of compounding and reduced charges over time take effect.

Adjust fund allocation to protect gains and ensure they align with your financial goals. A properly planned ULIP strategy helps in wealth creation and risk management, maximising fund returns.

Returns as of Apr'26. Fund ratings by Morningstar as of Apr'26.

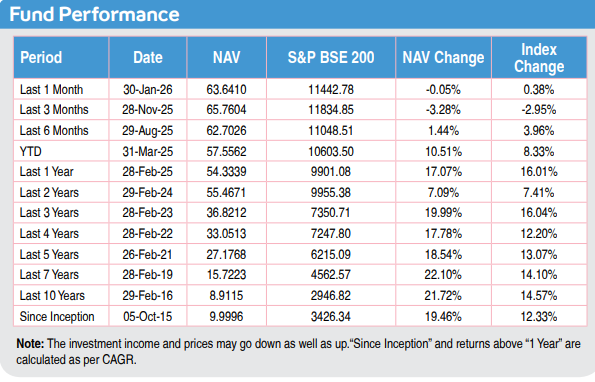

Tata AIA ULIP plans offer a flexible way to build long-term wealth through unit-linked savings and life protection. These ... Read more market-linked7 solutions allow you to invest in equity funds, debt funds, or hybrid funds based on your goals and risk appetite. Tata AIA’s equity-oriented ULIP funds have delivered competitive performance, with the India Consumption Fund showing a 5-year annualised return of 18.54% (Benchmark: 13.07%) and the Top 200 Fund recording 19.13% (Benchmark: 13.07%) as of Feb’26.

With ULIP features such as fund switching, partial withdrawals, premium allocation, and transparent ULIP charges, you can customise your financial strategy with complete flexibility. ULIP fund options allow you to align your investment with your preferred mix of growth and stability. Plans like Tata AIA Premier SIP and Tata AIA Param Raksha Life Pro+ help you grow wealth systematically while ensuring long-term financial security. Read Less

Here’s what you should do to optimise the returns once you choose the top rated ULIP plans.

Consider investing in a ULIP scheme from an early age. By choosing a longer policy period, you will reduce the risk of short-term volatility. Additionally, you can pay a reasonable premium for the required coverage.

Invest in long-term funds based on your risk profile. Utilise the switching option to maximise your returns based on the current market conditions.

Make sure you review your ULIP policy on a regular basis to ensure it continues to meet your requirements and aligns with the market conditions.

ULIPs offer a variety of fund options. Based on your risk appetite, you can invest in equity, debt, or balanced funds. You can also switch between ULIP funds at no cost as per your needs. In this way, you can maximise your returns by taking advantage of market conditions. If the markets are volatile, you can invest in low-risk debt funds, and if they are favourable, you can invest in equity funds.

Managing ULIP funds can be based on your investment preferences. At Tata AIA, you can choose the investment approach based on the following options to manage your ULIP funds.

It refers to manual selection, which means you can choose the fund options based on their performance and requirements, all by yourself!

If your objective is to minimise losses, we provide fund options that offer intermediate growth and ensure safety.

If you want to enhance the potential gains, we offer fund options for high growth with risk.

We also offer options to balance risk and return for your investment goals.

We offer Enhanced SMART (Systematic Money Allocation & Regular Transfer) for a structured investment into the volatile market based on your choice of an equity-oriented fund and a debt-oriented fund.

| Plan Name | Entry Age | Minimum Annual Investment |

|---|---|---|

| Tata AIA Premier SIP | 18-50 years | ₹12,000/year or ₹1,000/month |

| Tata AIA Smart SIP | 18-65 years | ₹12,000/year or ₹1,000/month |

| Tata AIA Smart Fortune Plus | 30 days-65 Years | ₹24,000/year or ₹2,000/month |

| Tata AIA Smart Sampoorna Raksha Supreme | 18-65 years | ₹20,000/year or ₹1667/month |

| Tata AIA i Systematic Insurance Plan | 0-60 years | ₹24,000/year or ₹2,000/month |

| Tata AIA Smart Sampoorna Raksha Pro | 18-65 Years | ₹24,000/year or ₹2,000/month |

ULIPs include a few charges associated with managing the policy that you should know.

A ULIP calculator is an online tool that helps you know the maturity amount, or the ULIP returns that you can receive from your Unit Linked Insurance Plans, and determine the applicable premium. Once you provide a few details about your investment and other requirements based on the ULIP features, you can determine the premium and the expected returns.

With the help of the ULIP return calculator, you can make a reasonable comparison and analysis instead of simply going by the ULIP charges, which is only one factor for selecting a ULIP. Read More: What is a ULIP Calculator? - Features & Benefits

When evaluating ULIPs, returns are typically measured in two ways:

The following table highlights how the power of compounding works in different scenarios.

| Monthly Contribution | Investment Period | Estimated Returns at 4%14 | Estimated Returns at 8%14 |

|---|---|---|---|

| ₹20,000 | 20 Years | ₹32,46,284 | ₹58,78,157 |

| ₹15,000 | 20 Years | ₹24,15,144 | ₹43,78,331 |

| ₹10,000 | 20 Years | ₹16,10,156 | ₹29,18,995 |

| ₹5,000 | 20 Years | ₹8,04,989 | ₹14,59,338 |

Illustrations show returns for specified monthly premium for Tata AIA Premier SIP for a 25-year-old male, standard life for the defined investment period, limited pay with 100% investment in Tata AIA Multi Cap Fund in Future Secure Plan option. 4% and 8% are assumed rates of returns. Other funds are also available with this plan.

A ULIP investment provides various tax6 benefits under the Income Tax Act, 1961, making it a tax-effective investment. Recent regulatory updates and taxation rules for ULIPs issued after February 2021 continue to influence investor decisions in 2026, especially for high-premium policies. Understanding these changes is essential before investing.

Amounts are based on a 20-year-old non-smoker male, with a 20-year premium payment term and a 30-year policy term, Future Secure plan option under the limited payment method with 100% invested in Tata AIA MultiCap fund at 8% Rate of Return. Returns @4% 18.7 Lakh for ₹5,000/month, 37.5 Lakh for ₹10,000/month, 56.3 Lakh for ₹15,000/month, 75.5 Lakh for ₹20,000/month respectively.

| As of 31st Mar | FY23 | FY24 | FY25 | FY26 |

|---|---|---|---|---|

Total AUM (in Cr.) |

71,006 |

99,207 |

122,922 |

145,589 |

The steps to buy the ULIP plan online are as follows:

Delaying your Investment can cost you Big

Start at age 25

Start at age 35

There are different types of term insurance plans you can choose based on your needs. Some of them are as follows:

The myths about investing in ULIPs are as follows.

Popular Searches Related to ULIP

Popular Searches

Last updated on 21 Jul 2026

Param Raksha Life Pro+ is designed for combination of benefits of following individual and separate products named (1) Tata AIA Smart Sampoorna Raksha Supreme Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02) and (2) Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). Both Smart Sampoorna Raksha Supreme and Tata AIA Health Buddy are also available for sale individually.

Tata AIA Premier SIP is a combination of the Tata AIA Smart SIP, a non-participating, unit-linked, individual life insurance savings plan (UIN: 110L174V02), and Tata AIA Health Buddy, Non-Participating, Non-Linked, Individual Health Product (UIN: 110N183V01). Both Tata AIA Smart SIP and Tata AIA Health Buddy are also available for sale individually.

Tata AIA Shubh Invest Protect comprises of Tata AIA Sampoorna Raksha Promise- A Non-Linked, Non-Participating, pure risk, Individual Life Insurance Product (UIN:110N176V11) and Tata AIA Smart SIP - Non-Participating, Unit Linked Individual Life Insurance Savings Plan (UIN:110L174V02). Tata AIA Sampoorna Raksha Promise and Tata AIA Smart SIP are also available individually for sale.

Tata AIA Sampoorna Raksha Promise - Non-Linked, Non-Participating, pure risk, Individual Life Insurance Product (UIN:110N176V12)

Tata AIA Smart SIP - Non-Participating, Unit Linked Individual Life Insurance Savings Plan (UIN:110L174V02)

Tata AIA Smart Fortune Plus - Non-Participating, Unit Linked Individual Life Insurance Savings Plan (UIN: 110L177V01)

Tata AIA Smart Sampoorna Raksha Supreme - Unit Linked, Non-Participating Individual Life Insurance Plan (UIN: 110L179V02).

Tata AIA Smart Sampoorna Raksha Pro - Non- Participating, Unit Linked Individual Life Insurance Savings Plan (UIN: 110L172V03).

Tata AIA i Systematic Insurance Plan - Non-Participating Unit Linked Individual Life Insurance Savings Plan (UIN:110L164V10)

1IIllustration shows monthly premium of ₹15,000 for Tata AIA Premier SIP for a 25-year-old male, standard life, premium payment term: 10 years, policy term: 20 years with 100% investment in Tata AIA Multi Cap fund in Future Secure Plan option. 4% and 8% are assumed rates of return. 17.65% is the 5-year return of Tata AIA Multi Cap fund as of Apr’26. Maturity amount: ₹24,15,144 at 4% returns, ₹43,78,331 at 8% returns and ₹1,73,67,190 at 17.65% returns. The fund value calculation is done by projecting the past returns of Tata AIA Multi Cap Fund for 25 years after adjusting for all expenses in Tata AIA Premier SIP Plan. The above values have been calculated assuming 17.65% p.a. CAGR, which is the past 5-year return of Tata AIA Multi Cap Fund as of Apr'26. Benchmark of this fund is S&P BSE 200.

2All funds open for new business which have been completed 5 years since inception are rated 4 or 5 Star by Morningstar as of August 2025.

3©2025 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. The information contained here: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar India Private Limited (“Morningstar”); (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources and (5) shall not be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar) nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the information.

4The Insured Amount under Terminal Illness with Term Booster option (in Health Buddy) is payable on earlier of death or diagnosis of Terminal illness of the Life Insured. Please refer Terms and Conditions for more details.

5Waiver of premium is available only in Future Secure and Family Secure option under Tata AIA Smart SIP.

6Income Tax benefits would be available as per the prevailing income tax laws under old tax regime, subject to fulfilment of conditions stipulated therein. Income Tax laws are subject to change from time to time. Tata AIA Life Insurance Company Ltd. does not assume responsibility on tax implications mentioned anywhere on this site. Please consult your own tax consultant to know the tax benefits available to you

No Goods and Service Tax shall be applicable on Individual life insurance products as per prevailing laws. Tax laws are subject to amendments from time to time. If any imposition (tax or otherwise) is levied by any statutory or administrative body under the Policy, Tata AIA Life Insurance Company Limited reserves the right to claim the same from the Policyholder.

7Market-linked returns are subject to market risks and terms & conditions of the product. The assumed rate of returns or illustrated amount may not be guaranteed and depends on market fluctuations.

8Rider is not mandatory and is available for a nominal extra cost. For more details on benefits, premiums, and exclusions under the Rider, please contact Tata AIA Life's Insurance Advisor/ branch.

9As on 31st October 2025, the company has a total Assets Under Management (AUM) of 1,45,589 Crores..

10The Individual Death Claim Settlement Ratio of Tata AIA is 99.45%, as per the latest annual audited figures for FY 2025-26

1198,01,699 families protected till 18th May 2026.

13Some benefits are guaranteed, and some benefits are variable with returns based on the future performance of your insurer carrying on life insurance business. If your policy offers guaranteed benefits, then these will be clearly marked “guaranteed’ in the illustration table on this page. If your policy offers variable benefits, then the illustrations on these pages will show two different rates of assumed future investment returns. Currently these are assumed rate of returns as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

Linked Life Insurance products are different from traditional insurance products and are subject to risk factors.

Various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns. The premium paid in Linked Life Insurance policies is subject to investment risks associated with capital markets and publicly available index. The NAV of the units may go up or down based on the performance of Fund and factors influencing the capital market/publicly available index and the insured is responsible for his/her decisions. On survival to the end of the policy term, the Total Fund Value including Top-Up Premium Fund Value valued at applicable NAV on the date of Maturity will be paid

Investments are subject to market risks. The Company does not guarantee any assured returns. The investment income and price may go down as well as up depending on several factors influencing the market

Tata AIA Life Insurance Company Limited is only the name of the Life Insurance Company & Tata AIA Smart SIP, Tata AIA Smart Fortune Plus, Tata AIA Smart Sampoorna Raksha Supreme, Tata AIA Life insurance Wealth Pro, Tata AIA Life Insurance Fortune Pro, Tata AIA Life insurance Fortune maxima, Tata AIA Life insurance Wealth Maxima, Tata AIA Systematic Insurance Plan and Tata AIA Smart Sampoorna Raksha Pro is only the name of the Linked Insurance contract and does not in any way indicate the quality of the contract, its future prospects or returns.

Please know the associated risks and the applicable charges, from your insurance agent or the Intermediary or policy document issued by the insurance company. Please make your own independent decision after consulting your financial or another professional advisor

Past performance is not indicative of future performance. Returns are calculated on an absolute basis for a period of less than (or equal to) a year, with reinvestment of dividends (if any)

If your policy offers variable benefits, then the illustrations on this page will show two different rates of assumed future investment returns. Currently the gross investment returns are stipulated as 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed, and these are not the upper or lower limits of what you might get back, as the value of your policy is dependent on a number of factors including actual future investment performance.

Life insurance cover is available under the solution. For more details on risk factors, terms and conditions please read Sales Brochure carefully before concluding a sale.

L&C/Advt/2026/Jun/3900

Reviewed by

Reviewed by

.jpg)